Asian consumer and internet equities have been among the most overlooked corners of the market in 2026. The AI infrastructure trade and the industrial re-armament cycle have absorbed the bulk of regional investor attention year-to-date, and consumer names have paid the price: valuations have drifted well below levels that reflect the underlying earnings trajectory, compounded by the impact of the Middle East conflict on sentiment and on energy-import-heavy economies like India.

We think this is a mistake, and one that is likely to correct sharply. The structural stories underpinning our conviction across Korea, India, China, and ASEAN have not deteriorated. They have simply been ignored. The businesses we hold are compounding earnings at 15 to 25% per year, with balance sheets in good shape and competitive positions that, in most cases, are stronger than they were 12 months ago. When attention rotates back to fundamentals, as it inevitably does when momentum trades lose steam, we think the gap between price and value will close quickly. For readers who want the full structural backdrop to these markets, our June 2025 Asia Consumption white paper provides an overview of the landscape.

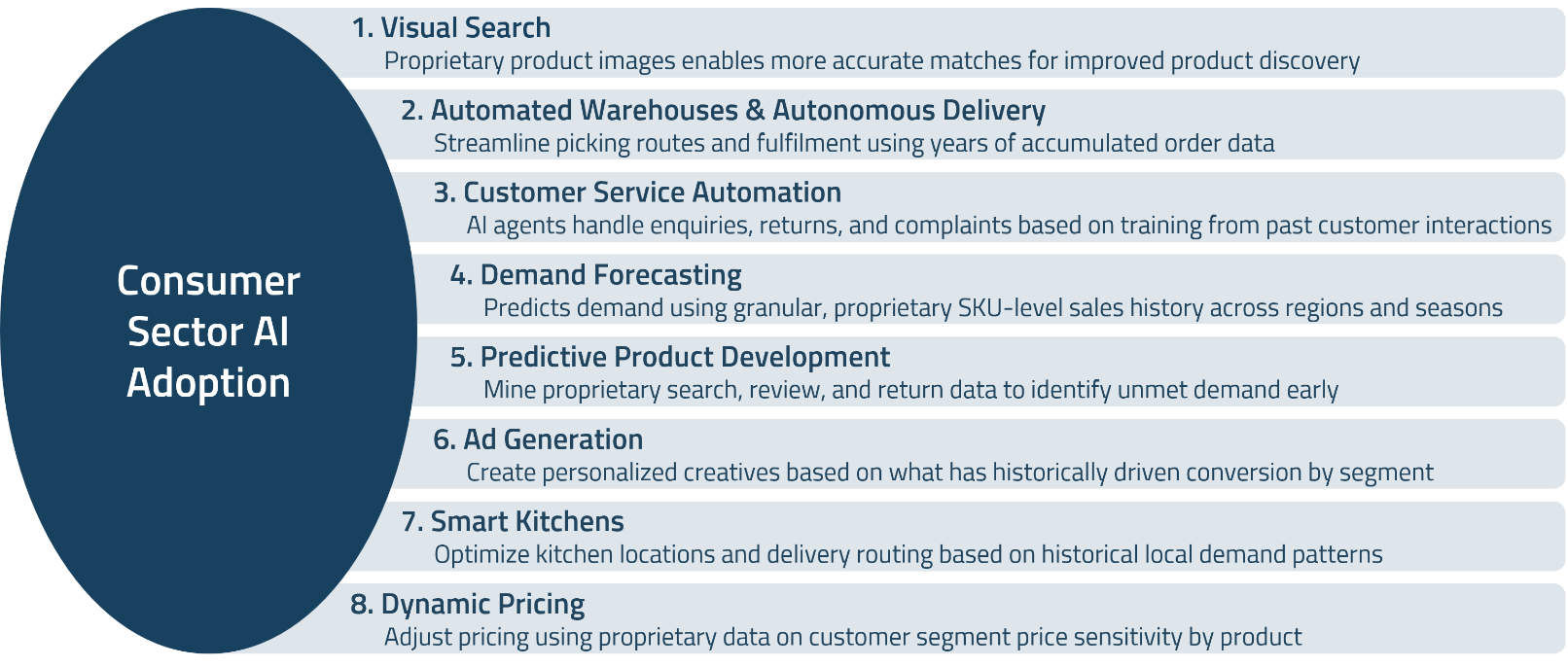

This note sets out our updated thinking across each market. Before doing so, we address directly the question that has generated the most investor anxiety in recent months: whether agentic AI represents a structural threat to consumer internet platforms. Our view is that it does not, and that the debate has been materially misconstrued. We set out our reasoning below, because it is relevant to how we think about every name in this piece.

No topic has generated more investor anxiety, or in our view, more confused thinking, than agentic AI and its potential to disrupt consumer internet platforms. The fear is intuitive: if AI agents can execute purchases autonomously, why would consumers still need to visit Taobao, Shopee, or MakeMyTrip?

Our answer, in short, is because the platforms own what the agents need. Agentic AI is a new interface layer, not a replacement for the supply chain, logistics network, inventory relationships, and consumer trust that the leading platforms have spent years building. To understand why incumbents win, it helps to understand what actually makes agentic AI work.

What Agentic AI Actually Requires

Unlike traditional chatbots that guide users but require manual follow-through, agentic AI executes multi-step workflows end-to-end. The enabling infrastructure, protocols like MCP (Model Context Protocol) and Google’s Universal Commerce Protocol, provides a bridge between AI models and live commerce systems. But that bridge is only as useful as the destination at the other end. An AI agent can place a food order, but it needs a platform with real-time inventory, pricing, and delivery capability to fulfil it. The platforms have that. The AI model providers do not.

The early evidence supports our view. ChatGPT’s consumer commerce ambitions have repeatedly stalled. The Walmart agentic tie-up was quietly unwound. Travel and commerce portals inside ChatGPT have failed to gain meaningful traction. Consumer behavior is hard to shift: users still prefer to browse and transact on familiar platforms, using AI primarily for research and discovery rather than autonomous purchasing.

The Platforms That Win: Four Structural Moats

With this frame in mind, we now turn to individual markets and names.

Korean beauty has quietly become one of the most powerful structural growth stories in consumer goods globally. Driven by the cultural reach of Korean pop music, drama, and social media, demand for Korean skincare and color cosmetics has expanded well beyond Asia into Europe, the US, and Latin America. What began as a niche trend has matured into a mainstream shift in consumer preferences, with Korean products increasingly seen not as budget alternatives to Western prestige brands but as genuinely superior formulations at a fraction of the price.

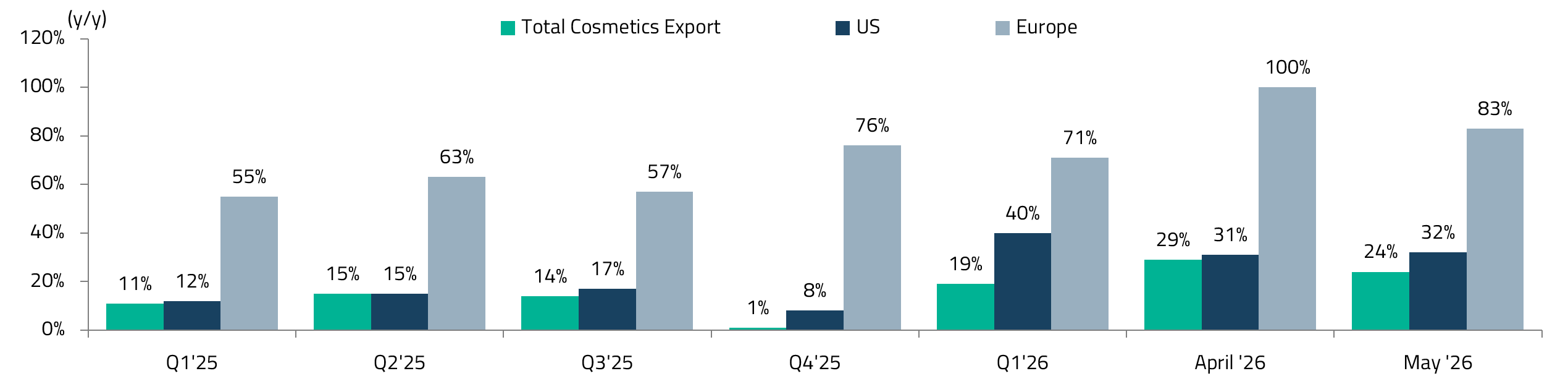

The data reflects this. Total Korean cosmetics exports grew 19% year-over-year (y/y) in the first quarter of 2026 and accelerated to 24% y/y in May.1 Europe has been the standout, with growth of 71% in the first quarter and 83% in May, while the US has re-accelerated sharply, posting 40% and 32% growth over the same periods.2

The structural shift driving this growth is the rise of indie brands. These smaller, digitally native labels have built global followings by delivering comparable quality to legacy multinationals at a fraction of the price. The table below illustrates the value proposition concisely.

| Category | Legacy luxury brand | K-beauty alternative | Key performance advantage |

|---|---|---|---|

| BB/CC Cream | IT Cosmetics CC+ Cream ($47) | Missha M Perfect Cover BB Cream ($10-$15) | Smoother coverage and better hydration at nearly 75% lower cost. |

| Anti-Aging Ampoule | Estée Lauder Advanced Night Repair ($125) | Missha Time Revolution Night Repair ($25-$30) | Similar fermented ingredients (“Extreme Biome”) for barrier repair at a far more accessible price point. |

| Pore Toner | Glow Recipe Watermelon Glow Toner ($35) | Axis-Y Daily Purifying Treatment Toner ($18) | Comparable BHA/PHA and tea-tree extracts to clear pores, with a more focused, gentle formula. |

| Liquid Blush | Rare Beauty Soft Pinch Liquid Blush ($23) | A’Pieu Juicy Pang Water Blusher ($8-$10) | Lighter, more blendable “watery” finish ideal for the dewy “glass skin” look. |

| Lip Gloss | Dior Addict Lip Maximizer ($40) | Rom&nd Glasting Water Gloss ($10-$12) | High-shine, non-sticky finish with a similar dewy sheen at nearly a quarter of the price. |

| K-indie brand | K-indie brand | K-premium brand | Global premium brand | |

|---|---|---|---|---|

| Brand | Beauty of Joseon | KAHI | Sulwhasoo | Dior |

| Product |  Relief Sun |

Airy Fit Sun Stick |

Sangbaek Sun Cream |

Diorsnow UV Shield Tone Up |

| SPF | 50+ | 50+ | 50+ | 50+ |

| PA | ++++ | ++++ | ++++ | +++ |

| Innovative tech / ingredient | Rice & probiotic ingredients | Polymer High Temperature Tech (withstands high temperature) | Patented water boosting (waterproof) | Melasolv (Amorepacific’s in-house whitening ingredient) |

| Packaging | Cream product in tube | Solid type in stick form | Cream product in tube | Cream product in tube |

| Volume | 50ml | 14g | 50ml | 30ml |

| Price | ₩19,000 (~$13) | ₩15,000 (~$10) | ₩90,000 (~$61) | ₩98,000 (~$67) |

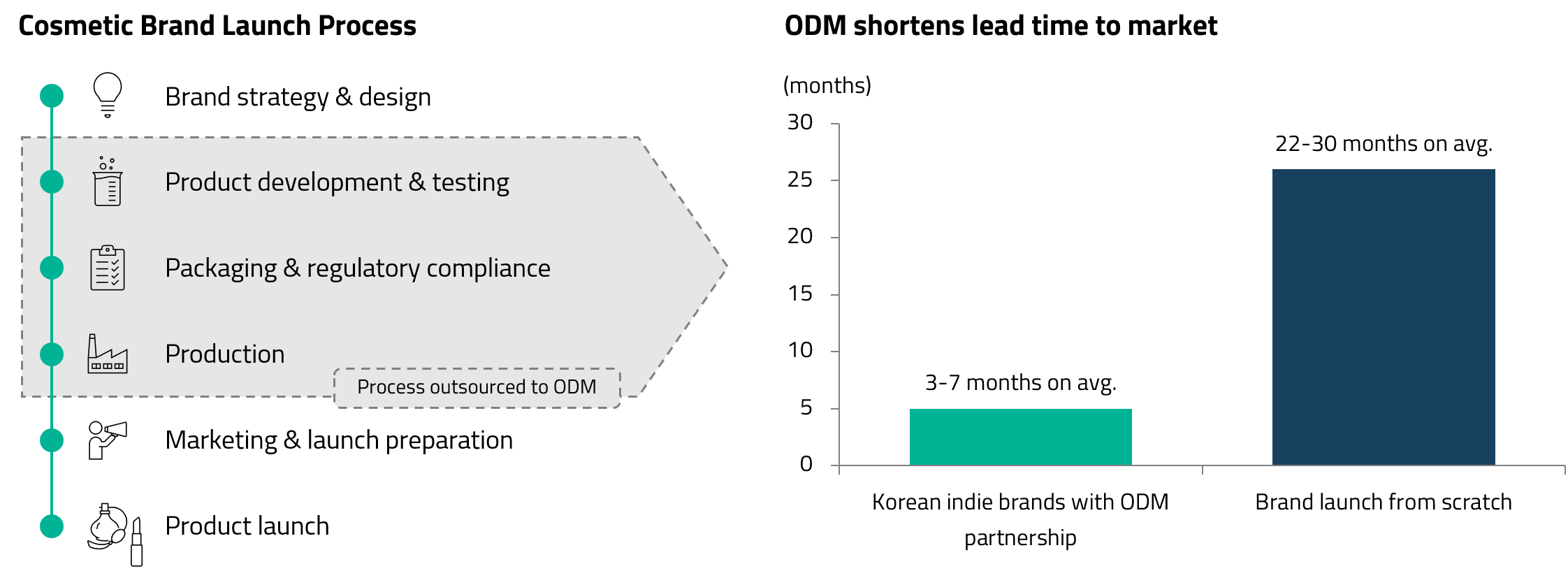

As indie brands take share from legacy multinationals, the principal beneficiary is not necessarily a consumer brand itself but the manufacturer behind many of them. Cosmecca Korea is one of the country’s leading ODM (original design manufacturer) cosmetics producers, meaning it formulates and manufactures products to order for brand clients rather than selling under its own name. This business model is particularly well-suited to the current moment: as indie brands proliferate and product cycles shorten, the ability to iterate quickly and cost-effectively becomes a genuine competitive advantage. Additionally, Cosmecca’s manufacturing footprint spans both Korea and the US, providing meaningful insulation against tariff-related disruptions that have affected other exporters.

Cosmecca’s edge is twofold: 1) its ODM model allows indie brand clients to bring new products to market rapidly, keeping pace with fast-changing consumer tastes, and 2) it delivers formulations on par with legacy multinationals at a fraction of the cost, which is precisely the dynamic that allows the brands it supplies to keep taking share.

We believe Cosmecca can compound earnings at approximately 15% per annum over the medium term, driven by continued export volume growth and improving operating leverage as the business scales. At 11x 2027 estimated earnings, the stock trades at a meaningful discount to that growth rate, and is one of the clearest cases of price-to-growth mispricing in our portfolio.3

India remains one of the most compelling consumer growth stories in the world, underpinned by a young and rapidly urbanizing population, rising female labor force participation, and per capita GDP reaching new highs. Household consumption accounts for over 60% of GDP, and the structural shift from agricultural to service and construction sectors continues to expand India’s middle and upper-middle class.4

That said, Indian equities have been among the hardest hit in the regional sell-off, compounded by the rupee’s depreciation and the oil price shock’s disproportionate impact on India’s import-heavy energy mix. Consumer sentiment has softened at the margin and near-term earnings revisions in some segments reflect that pressure. However, below the macro noise, the multi-year structural stories we have been building positions in are more intact than ever.

Eternal (Zomato): Quick Commerce Still in Early Innings

One of the most significant behavioral shifts underway in urban India is the rise of quick commerce, referring to on-demand delivery of groceries and everyday essentials in under 15 minutes. Few predicted that this format would achieve the adoption it has to date, but it has proven to be a genuinely durable convenience proposition, particularly among younger urban consumers who prioritize time over marginal cost savings. The category is still nascent: urban penetration is low, product selection is expanding and should eventually catch up to the SKU range available on traditional e-commerce platforms, and consumer behavior is still shifting.

The quick commerce market in India was approximately INR 300 billion (~USD 4 billion) in 2024 and is projected to reach INR 2 trillion (~USD 22 billion) by 2028.5 The rapid growth is driven by improving delivery density and the rapid growth of dark stores, and the small fulfillment centers located close to consumers that make ultra-fast delivery economically viable.

Eternal, the parent company of Zomato, is the market leader in this space. The company has leveraged its extensive experience and infrastructure from food delivery to efficiently build out its quick commerce operation, Blinkit, giving it a head start on logistics, supply chain relationships, and consumer trust that newer entrants will find difficult to replicate quickly. Competitors, including Zepto, Instamart, and Flipkart, are ramping up, and the category will likely remain competitive. But quick commerce in India remains a blue-ocean market with years of meaningful growth ahead, and we think Eternal is best positioned to capture the largest share of that expansion.

Nykaa: India’s Gateway to the Beauty Revolution

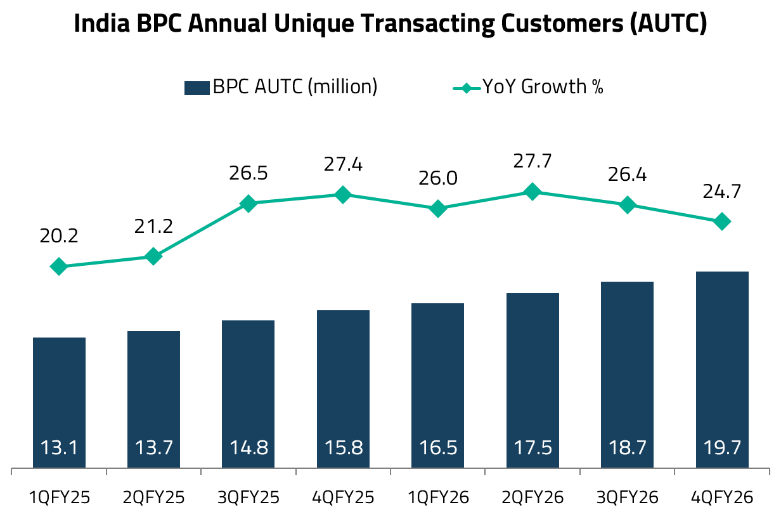

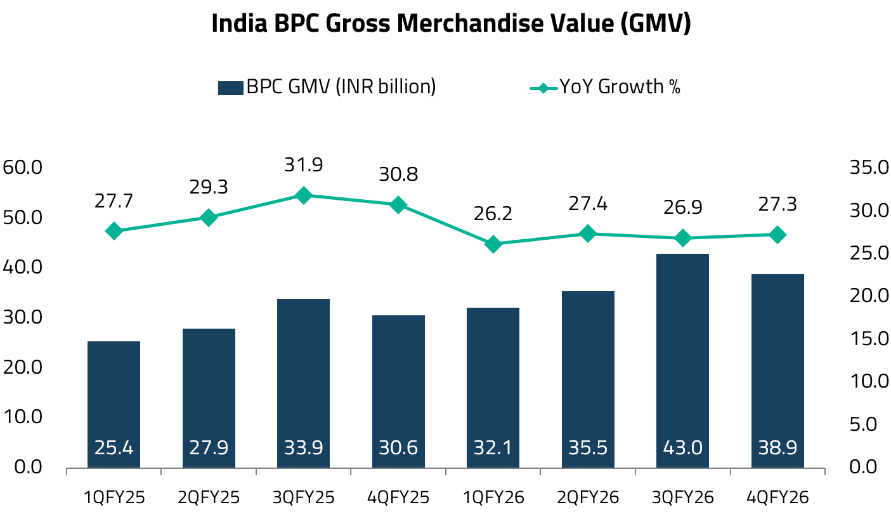

India’s beauty and personal care (BPC) market is one of the fastest-growing globally, with industry estimates pointing to low double-digit CAGR over the coming years.6 The structural drivers are compelling and mutually reinforcing. India’s median age is below 29, with over 65% of the population under 35, creating a large, young, and increasingly image-conscious consumer base whose grooming and skincare habits are still maturing.7 Rising female workforce participation and higher disposable incomes are driving premiumization, while the rapid expansion of the middle class in tier-2 and tier-3 cities is steadily enlarging the addressable market beyond the major urban centers.

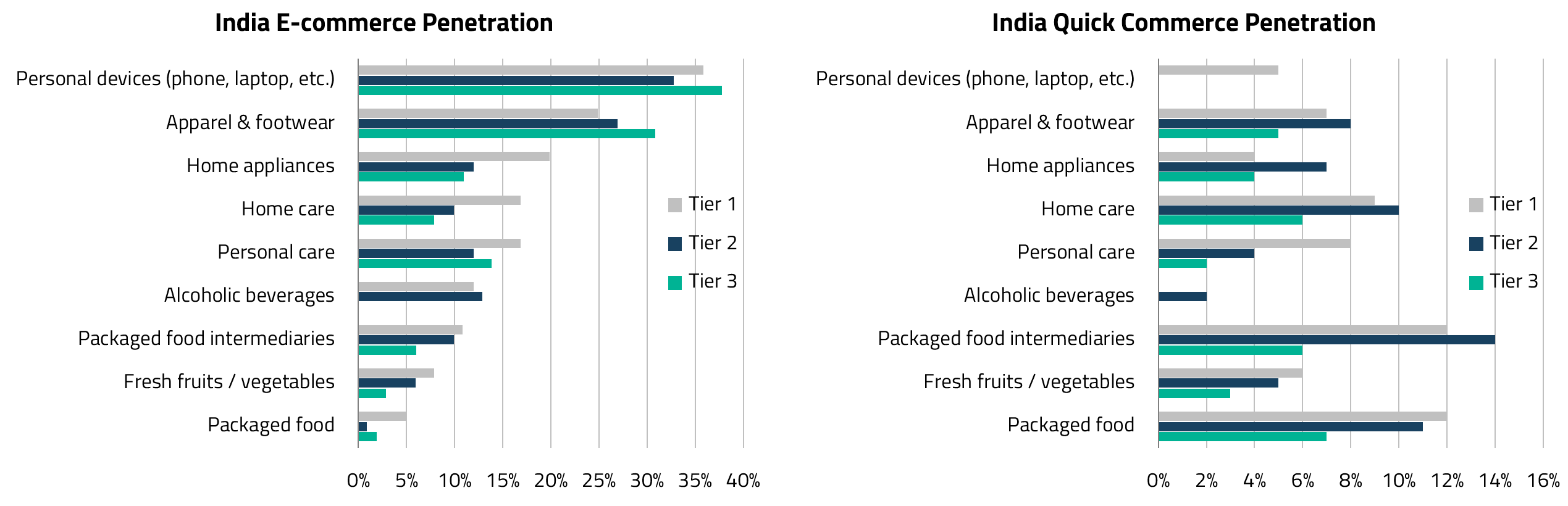

The online channel is the primary engine of this growth, compounding at a significantly faster pace than the overall market as e-commerce platforms solve longstanding distribution gaps, extend nationwide reach, and offer a far deeper range of products across price points and sub-categories than physical retail can match. Online already accounts for approximately 30% of beauty and personal care sales in India and is on track to reach parity with organized offline retail, making it one of the fastest-growing verticals in Indian e-commerce.8

We think Nykaa is structurally best placed to capture this opportunity. Founded as a pure-play beauty destination at a time when the category was fragmented and largely served by general retailers, Nykaa now commands approximately 30% of India’s online beauty and personal care market, making it the largest specialty platform in a channel itself growing at over 25% per year.9 That first-mover advantage matters enormously in a market historically troubled by counterfeit products. Nykaa’s inventory-led model, whereby it sources, stores, and fulfills products directly rather than acting purely as a marketplace, gives it tighter control over authenticity and quality. This has made it the trusted destination of choice for consumers seeking genuine products, and the preferred partner for both international luxury brands and domestic labels seeking credible distribution.

The company’s moat extends beyond assortment into what is best described as a full-funnel content-to-commerce engine. Through tutorials, reviews, and influencer-led education, Nykaa moves consumers from discovery to purchase within its own ecosystem, deepening engagement and structurally reducing customer acquisition costs. Late entrants trying to replicate this must spend aggressively to build equivalent trust and habits, a gap that compounds in Nykaa’s favor over time.

Against this backdrop, Nykaa’s beauty business continues to grow at approximately 25% per year, supported by robust customer additions and rapid premiumization as Indian consumers trade up.10 With category leadership, a defensible content-driven moat, and a market that is still in the early stages of its growth trajectory, Nykaa is uniquely positioned to play India’s multi-year beauty and personal care story.

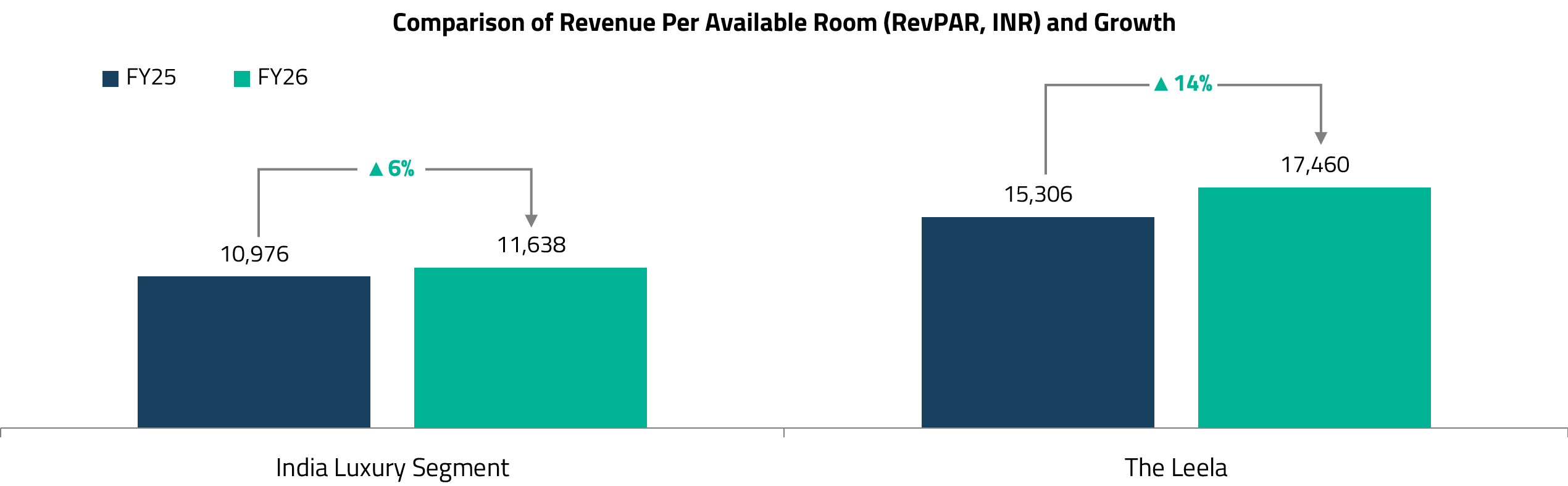

Leela Hotels: Capturing India’s Luxury Travel Moment

India’s premium hospitality sector is entering a period of sustained structural growth, underpinned by a favorable demand-supply dynamic seen in few other markets. On the demand side, the rapid expansion of high-net-worth wealth in India is creating structural growth in luxury travel, while the rising share of Global Capability Centers (GCCs) in commercial leasing is driving a steady increase in high-spending foreign business travelers. On the supply side, new luxury hotel additions remain constrained: projects of this scale require substantial upfront capital and typically deliver returns only over a long back-ended horizon, keeping competitive intensity low and pricing power firmly in the hands of existing operators. Together, these dynamics point to double-digit growth in average room rates (ARR) over the medium term.11

Leela Hotels is the natural beneficiary of this moment. Founded four decades ago and now backed by Brookfield, Leela operates 15 properties with approximately 4,000 keys across India’s most important business and leisure destinations.12 It is the country’s only pure-play luxury hospitality brand at scale, a distinction that matters enormously in a segment where brand credibility takes decades to build and cannot be manufactured quickly by capital alone. That brand strength is reflected in Leela’s ability to command a roughly 50% premium in revenue per available room (RevPAR) versus the broader luxury industry, a measure that captures both occupancy and pricing power in a single metric.13

What makes Leela’s positioning particularly durable is its approach to the guest experience. Rather than offering a standardized luxury product, each Leela property is deeply embedded in its local context, drawing on regional culture, art, cuisine, and heritage to create a differentiated experience that is genuinely difficult to replicate. This is not merely a brand narrative, but it’s also reflected in the numbers. Leela’s net promoter score of 86 compares to an industry average of 74 for the luxury segment, a meaningful gap that speaks to the loyalty and advocacy among its guests.14

As India’s affluent consumer base expands and experiential travel continues to take a larger share of discretionary spending, Leela is positioned as the primary destination for both domestic luxury travelers and the growing wave of inbound business and leisure visitors seeking an authentically Indian premium experience.

China’s consumer internet landscape has undergone a year of significant disruption. Fierce competition among the major platforms, particularly in food delivery, where subsidy wars between JD, Alibaba, and Meituan have weighed on profitability across the board, has prompted legitimate questions from investors about the return profile of this spending. At the same time, China’s broader pivot toward domestic consumption-led growth, a theme we explored in detail in our June 2025 paper, is creating a more supportive backdrop for consumer-facing businesses over the medium term as policy stimulus filters through to household spending power. The near-term competitive noise is real, but it should not obscure the quality of the underlying franchises.

Alibaba: More Than the Sum of Its Parts

Alibaba needs little introduction as a name, but its current investment case is more nuanced than its reputation as China’s dominant e-commerce operator might suggest. The bear case centers on food delivery profitability – Alibaba has been investing heavily in instant commerce (the rapid delivery of everyday items like groceries, meals, and household goods), and the subsidy-driven customer acquisition costs have weighed on near-term earnings. The bull case centers on everything else.

Our view is that as long as Alibaba’s instant commerce operations reach break-even, a threshold that appears increasingly within reach as subsidy intensity normalizes, the traffic and consumer attention captured through that channel can be leveraged to reinforce the core Taobao and Tmall ecosystem at near-zero incremental cost. The strategic logic is straightforward: acquire new customers through high-frequency everyday purchases such as milk tea and lunchboxes, then cross-sell higher-margin discretionary products across the broader platform.

The early evidence suggests this is working. Taobao Shangou, Alibaba’s instant buy-and-deliver service, generated over 100 million orders from new users brought onto the Taobao app during just the first three weeks of the Singles’ Day shopping festival alone.15

Separately, we believe the market is materially undervaluing Alibaba’s cloud business. Cloud computing in China is still in the relatively early stages of enterprise adoption, and Alibaba Cloud is the clear market leader. We expect the business to compound at approximately 40% per year while generating meaningful margin expansion as the initial investment phase matures.16 This trajectory is not yet visible in consensus numbers in a way that reflects its full potential. At approximately 14x 2028 estimated earnings, Alibaba screens as one of the cheapest quality businesses in our universe.17 The food delivery drag is real but transitional. The cloud optionality is underpriced.

PDD Holdings: Domestic Stability, Temu Optionality

PDD Holdings operates two distinct but complementary businesses: Pinduoduo, its domestic Chinese e-commerce platform, and Temu, its fast-growing international marketplace. Understanding both is essential to appreciating why the stock screens as compellingly undervalued at current prices.

PDD built its domestic position by targeting price-sensitive consumers with a social commerce model that rewarded group buying and peer referrals. What began as a challenger to Alibaba and JD has grown into a platform with genuine scale and a deeply entrenched value-for-money brand perception that proves difficult to dislodge even as consumers’ incomes rise. Domestically, PDD is now cycling through an easier comparable period following a year of heavy investment, and GMV growth is running in the low-teens year-over-year, comfortably ahead of the mid-single-digit growth seen across the broader Chinese e-commerce industry.18 PDD is also moving up-market into consumer electronics, undercutting Taobao and JD on higher-value appliances and devices, historically categories where winning consumer trust has been difficult, further entrenching its value positioning across a wider range of purchase occasions.

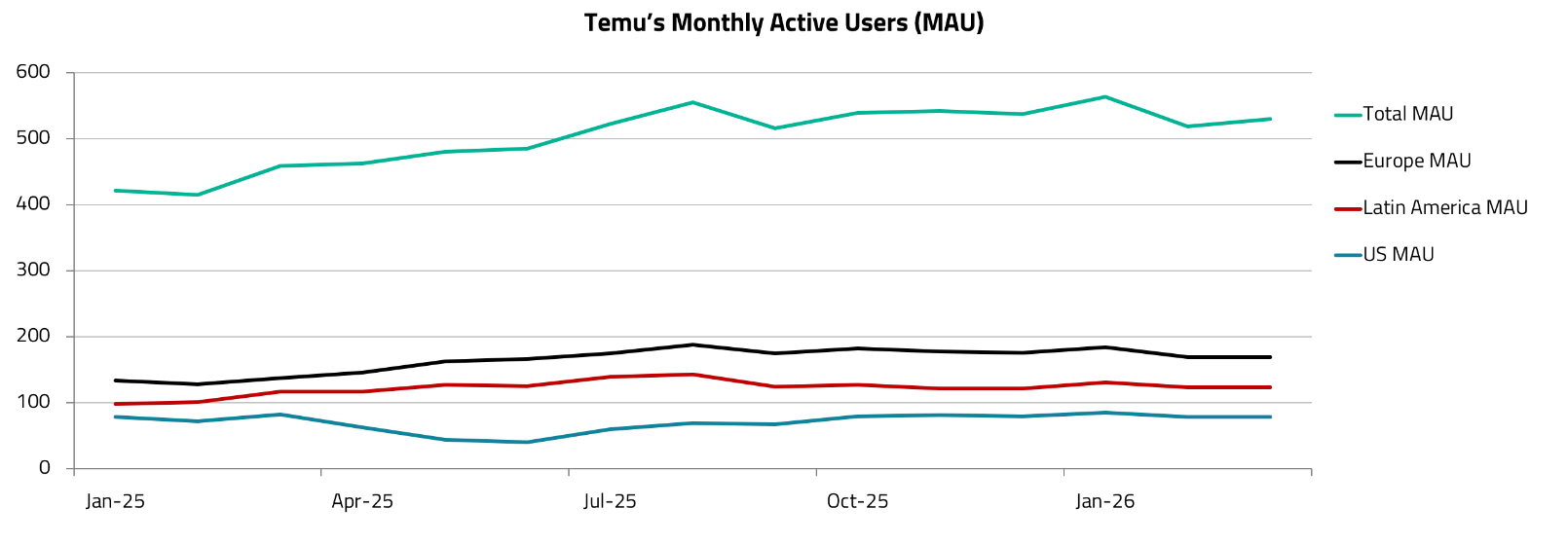

Internationally, Temu has scaled at a pace that few anticipated when it launched in 2022. The platform now registers over 530 million global monthly active users as of Q1 2026, with early signs of profitability emerging in select markets.19 Temu’s model, connecting international consumers directly with cost-efficient Chinese manufacturers, gives it a structural cost advantage that is difficult for Western platforms to replicate. As the business matures, we expect the long-term take-rate to converge toward the 2%+ range seen among established global peers, implying substantial earnings optionality that is not reflected in current numbers.

At 7x 2027 estimated earnings, PDD is the most undervalued name in our China internet exposure.20 The reporting opacity is a legitimate concern that we do not dismiss. But it does not change the fundamental competitive reality: this is a business with a dominant domestic position and a fast-growing international platform, currently priced as if both are impaired.

Southeast Asia’s consumer markets have been broadly caught in the regional sell-off, with energy-importing economies feeling the acute impact of higher crude prices. The macro headwinds are real, but they are masking a set of idiosyncratic structural growth stories that we believe are as compelling as ever. Our approach in ASEAN has always been to look past the regional noise and focus on businesses with idiosyncratic growth drivers that are insulated from the macro headwinds.

MWG Mobile World: Quietly Compounding in Vietnam

Vietnam is one of the most interesting consumer markets in Southeast Asia, combining a young and increasingly affluent population with a retail landscape that remains significantly underpenetrated by modern trade formats. As incomes rise and urbanization accelerates, Vietnamese consumers are shifting away from traditional wet markets and informal retailers toward organized, branded retail experiences. This transition is still in its early stages, which is precisely what makes it interesting from an investment perspective.

Mobile World Group (MWG) is Vietnam’s leading consumer retailer, operating across two distinct but complementary segments. Its DMX electronics division is the country’s dominant consumer electronics retailer, offering smartphones, laptops, and household appliances through a nationwide store network with a service proposition that smaller competitors cannot match. DMX leverages its balance sheet and nationwide coverage to offer superior after-sales support, and has built an in-house buy-now-pay-later programme, MWG Paylater, developed with Cake by VPBank, that offers zero down payment, zero interest on selected products, and credit lines of up to VND 40 million (~USD 1,500) with approval in approximately two minutes via app. In a market where consumer credit infrastructure is still developing, this is a meaningful differentiator.

The more exciting long-term opportunity, however, lies in Bách Hóa Xanh (BHX), MWG’s grocery division. Modern trade grocery penetration in Vietnam stood at only around 12% in 2022, compared to 30% to 50% across more developed ASEAN markets, leaving an enormous runway for organized retailers to take share from traditional wet markets and informal vendors.21 BHX operates as a neighborhood mini-supermarket, offering a clean and organized shopping environment, packaged goods with clear food safety standards, and the convenience of fixed pricing and electronic payment, attributes that resonate strongly with younger, urban Vietnamese consumers. The contrast with traditional wet markets is stark, as the table below illustrates.

| Feature | Bách Hóa Xanh (BHX) | Traditional wet markets |

|---|---|---|

| Format | Clean, organized mini-supermarket layout with standard checkout counters. | Open-air stalls, crowded corridors, and occasionally wet floors. |

| Product origin | Packaged and weighed items with clear traceability, branding, and food-safety standards. | Unpackaged, whole-animal, and raw produce displayed directly by farmers and vendors. |

| Pricing | Slightly higher on average, with occasional deep discounts to compete. | Generally cheaper; heavily favors haggling and direct negotiation. |

| Experience | Modern conveniences like air conditioning, POS payments, and uniform shelf stock. | Immersive, authentic cultural experience where buyers inspect live / recently slaughtered meats. |

Sea Limited: Southeast Asia’s Digital Ecosystem, Now Compounding

Sea Limited is Southeast Asia’s leading digital ecosystem platform, operating across three interlocking businesses: Shopee, the region’s dominant e-commerce marketplace; Garena, a gaming platform with over 660 million quarterly active users; and Monee, a rapidly scaling digital financial services arm.22 We featured Sea in our June 2025 paper, and the competitive position today is considerably stronger than it was a year ago.

Sea’s full year 2025 results reflected broad-based strength across all three segments, with revenue growing 36% to ~USD 23 billion and net income more than tripling to USD 1.6 billion.23 Shopee delivered Q4 GMV growth of 29% year-over-year, with gross orders up 31%, while Monee revenue grew 54% in the same period driven by rapid expansion of its credit business.24 Garena, which has at times been characterized as a declining asset, surprised positively, with 2025 bookings up 37% and higher paying user penetration, providing stable high-margin cash flows that fund growth across the ecosystem without requiring external capital.25

The market’s negative reaction to 2026 guidance struck us as a misreading of the situation. Sea’s target of roughly 25% Shopee GMV growth in 2026, with adjusted EBITDA at least matching 2025, sits at the centre of the debate, with investors questioning management’s ability to balance heavier investment in logistics, membership, and financial services against preserving profitability. Our view is that Sea is reinvesting from a position of strength rather than necessity, following the same playbook that successfully defended market share against PDD and Douyin in 2022 and 2023. The most recent Q1 2026 results support this reading, with Shopee revenue up 44% year-over-year and Monee revenue up 58%, both ahead of expectations.26

The fintech flywheel is the part of the story least appreciated by the market. Monee’s credit underwriting models are fed by real-time transaction data from Shopee, enabling a distinctive approach to financial inclusion that has added tens of millions of first-time borrowers across the region, with non-performing loan ratios remaining stable throughout the expansion. In 2025 alone, Monee gained over 20 million unique first-time borrowers, while Shopee served around 400 million active buyers and 20 million sellers.27 The interconnected nature of the three businesses creates switching costs and network effects that standalone competitors, whether in e-commerce, gaming, or fintech, cannot easily replicate.

Sea’s balance sheet provides an additional layer of conviction. The company holds substantial net cash, funding the current investment cycle while providing meaningful downside protection. For long-term investors willing to look through a period of deliberate reinvestment, Sea remains one of the most compelling quality-at-a-discount opportunities in our portfolio.

The sell-off in Asian consumer and internet equities has created a rare alignment of compelling valuations and intact fundamentals. Across Korea, India, China, and ASEAN, the businesses we have written about in this note are compounding earnings at rates that their current valuations do not come close to reflecting. The macro headwinds – elevated crude prices, currency pressure, and geopolitical uncertainty – are real. But they are conditions, not conclusions, and importantly, they do not alter the structural trajectories of the themes we’ve identified.

On agentic AI, our view is straightforward. We believe that innovative incumbents, those who are actively embedding AI to optimize and enhance their businesses, will win. The platforms with the deepest data, the most extensive logistics infrastructure, and the most trusted consumer relationships will be the ones that AI agents route through, not around. The disruption thesis misunderstands where the moats actually sit, and we are comfortable holding positions in businesses that we believe will be net beneficiaries of the AI transition rather than its casualties.

We have been adding selectively to our highest-conviction names through this period of weakness, maintaining our long-term orientation while remaining attentive to the risk of further escalation in the Middle East. More broadly, the AI infrastructure trade and the momentum that has surrounded it have absorbed an extraordinary share of investor attention and capital this year, leaving little room for anything else. We expect that when that momentum tapers, and when the geopolitical fog clears, the rotation back toward quality consumer and internet businesses in Asia is likely to be sharp.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return, and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Private Placement Memorandum for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The MSCI AC Asia ex Japan Index captures large and mid-cap representation across Developed Markets (DM) countries (excluding Japan) and Emerging Markets (EM) countries in Asia. The index covers approximately 85% of the free float-adjusted market capitalization in each country. The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips, and foreign listings (e.g. ADRs). The index covers about 85% of the Chinese equity universe.

The contents of this material are prepared and maintained by Shikhara and have not been reviewed by the Securities and Exchange Commission of the United States.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.