Asia’s consumption growth story is evolving, driven by fundamental demographic and economic shifts. The rapid expansion of the middle class, particularly across India and ASEAN nations, is unleashing unprecedented discretionary spending power. This demographic transformation coincides with strategic supply chain diversification away from China. As manufacturing investment flows into these markets, rising wages are accelerating a virtuous cycle of consumption. Meanwhile, this regional evolution is prompting China to accelerate its own pivot toward domestic consumption-driven growth, marking a strategic shift from its traditional export and investment model. On top of these macro trends, we’ve also seen a shift in consumption behavior across Asia, which we explore in this paper.

Despite these varied dynamics, the broader Asian landscape continues to offer a wealth of idiosyncratic investment opportunities, driven by each market’s distinct consumer evolution and economic prospects. For long-term investors, the key to capturing these opportunities lies in identifying market leaders with strong unit economics, clear paths to market share gains, and robust balance sheets. In this paper, we delve into the unique consumption opportunities present across key Asian markets.

Consumption in the Back Seat for Far Too Long

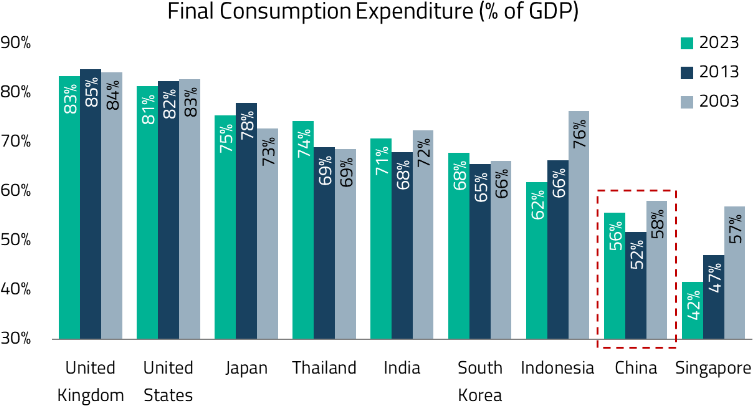

Historically driven by substantial government-led infrastructure investments, the Chinese economy is now navigating a period of recalibration. Excessive construction has resulted in underutilized infrastructure and property assets, creating challenges in managing accumulated debt. This structural slowdown is evident in the deceleration of credit growth, with key indicators such as Total Social Financing (TSF) and bank asset growth (excluding government bonds) reaching new lows. Meanwhile, total consumption accounts for only around 56% of China’s GDP, significantly lower than the 70-80% seen in developed economies and many emerging markets.1

In response to these economic headwinds, the Chinese government is pivoting towards boosting domestic consumption as a primary driver of GDP growth. Recognizing that relying on future borrowing is unsustainable, policymakers are implementing measures to stimulate consumer spending. Key strategies include addressing local government debt to ensure the repayment capabilities of constructors and SMEs, encouraging banks to increase lending for corporate capital expenditures and hiring, and subsequently raising wages to incentivize consumer spending.

From September 2024 onwards, signs of economic easing have emerged, particularly in household consumption. Policy measures such as trade-in stimuli, reductions in the Reserve Requirement Ratio (RRR), 7-day repurchase agreements (REPO), Medium-Term Lending Facility (MLF) rates, and Loan Prime Rates (LPR) are expected to lower borrowing costs and provide subsidies that enhance consumer purchasing power.

This pivot becomes all the more necessary within the current geopolitical climate of tariffs. While US-China relations remain tense, there is a complex interdependency between the two nations, which means decoupling overnight won’t happen. Still, we expect the US to reduce its sourcing from China by ~30-40% over the next few years. In response, China will need to look to expand its consumption share of GDP as a way to mitigate external shocks and sustain long-term growth.

On consumption, retail sales in China have maintained a steady growth rate of approximately 5% year-over-year (y/y), supported by stable growth in disposable income.2 However, beneath this consistent retail performance lies a varied growth profile across different product categories. Domestic brands are increasingly capturing market share in sectors such as sportswear and cosmetics, challenging the dominance of established international players. This shift underscores a broader trend of consumer preference towards locally understood and competitively priced products. The resilience of Chinese brands is further demonstrated by their adaptability and strategic expansions, both domestically and internationally.

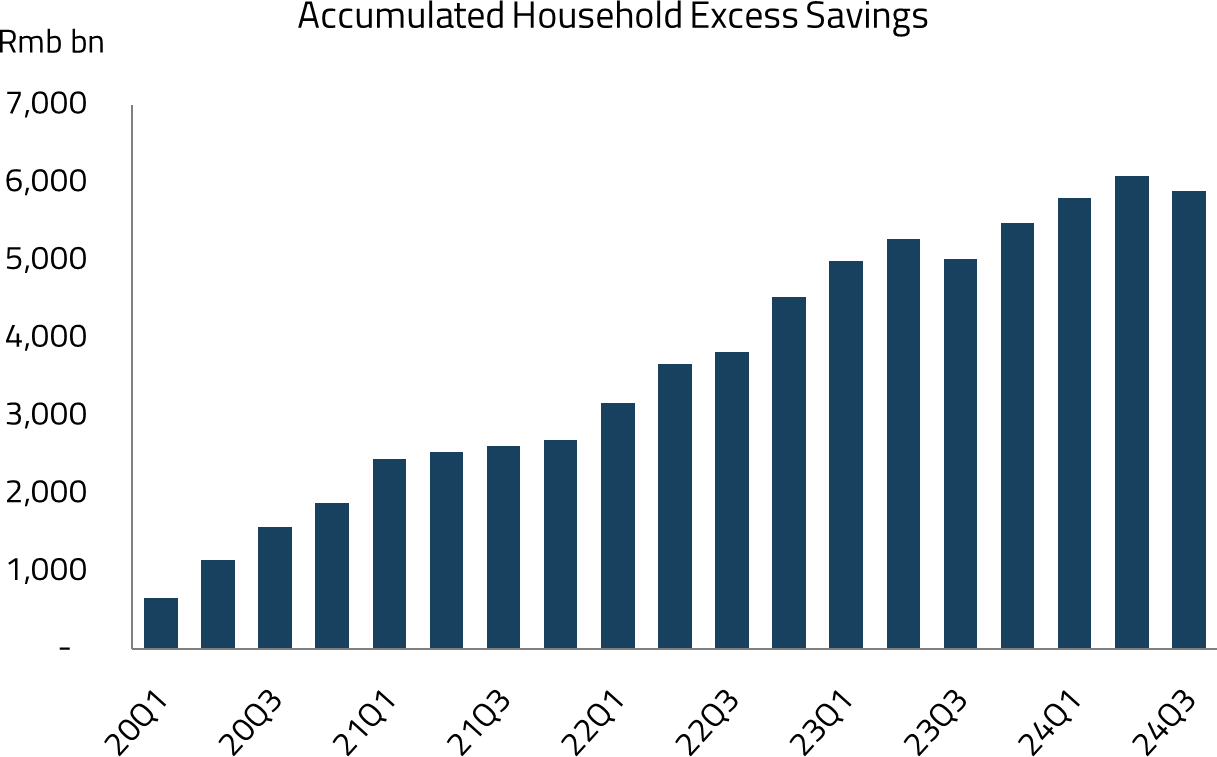

Additionally, China’s consumer base has benefited from a period of reduced property purchases, leading to significant savings accumulation among households. This financial cushion enhances the potential for sustained consumer spending, even amidst economic uncertainties. The government’s focus on enhancing domestic consumption is further supported by initiatives aimed at stabilizing the market through various policy levers, ensuring a robust and resilient economic environment.

In China, we are witnessing domestic leaders gaining significant market share by leveraging their understanding of local consumer preferences while eyeing international expansion opportunities. This trend underscores the resilience and adaptability of Chinese brands in a competitive landscape. We believe the best companies thrive under difficult conditions, and their lackluster valuations provide attractive entry points.

We categorize the best opportunities into two groups: 1) domestic leaders that can consolidate market share in fragmented industries, and 2) companies with stable domestic growth and significant international expansion opportunities.

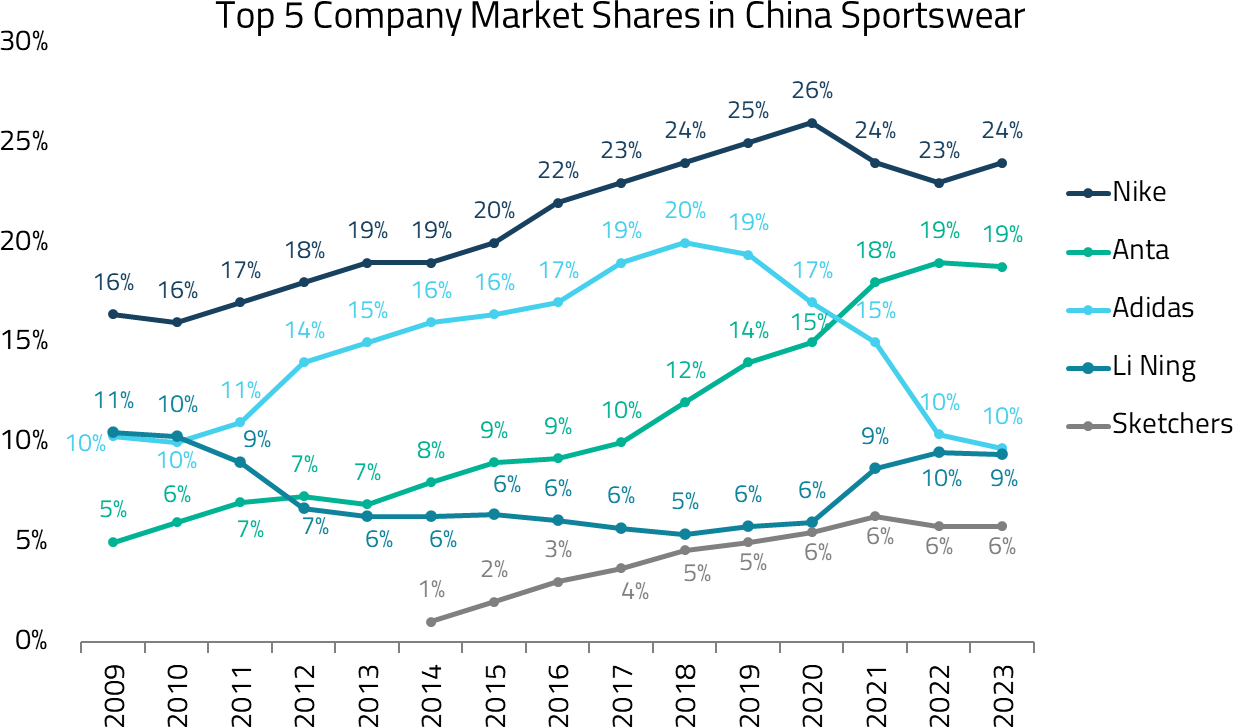

In the first category, Anta Sports exemplifies a domestic leader consolidating market share. Once dominated by foreign brands like Nike and Adidas, China’s sportswear industry has seen domestic brands emerge as new favorites over the past decade. By offering quality products at competitive prices, Anta has captured 19% market share in China, approaching Nike’s 24%.3 The company leverages cash flow from its core brand to acquire premium labels like Fila and Descente, building a strong multi-brand portfolio.

In the second category, Pinduoduo (PDD) illustrates successful international expansion built on domestic strength. Starting as an insignificant player in 2015 when Alibaba and JD dominated Chinese e-commerce, PDD has grown to capture 20% market share with comparable take-rates.4 Its international platform, Temu, launched in 2022, has already achieved Amazon-comparable global monthly active users (MAU) and approximately USD 50 billion in gross merchandise value (GMV) for 2024.5 Despite tariffs, we believe Temu’s growth potential could exceed PDD’s domestic operations, given its unique advantage in connecting international consumers directly with cost-efficient Chinese manufacturers.

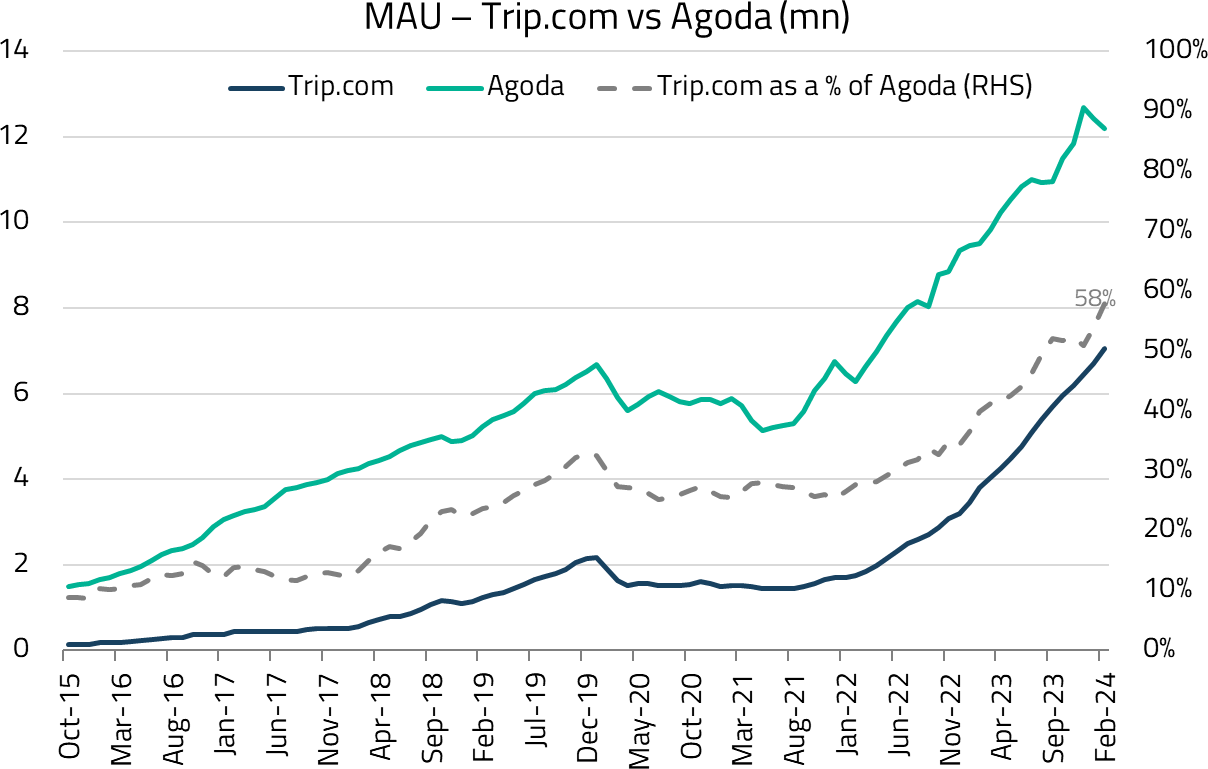

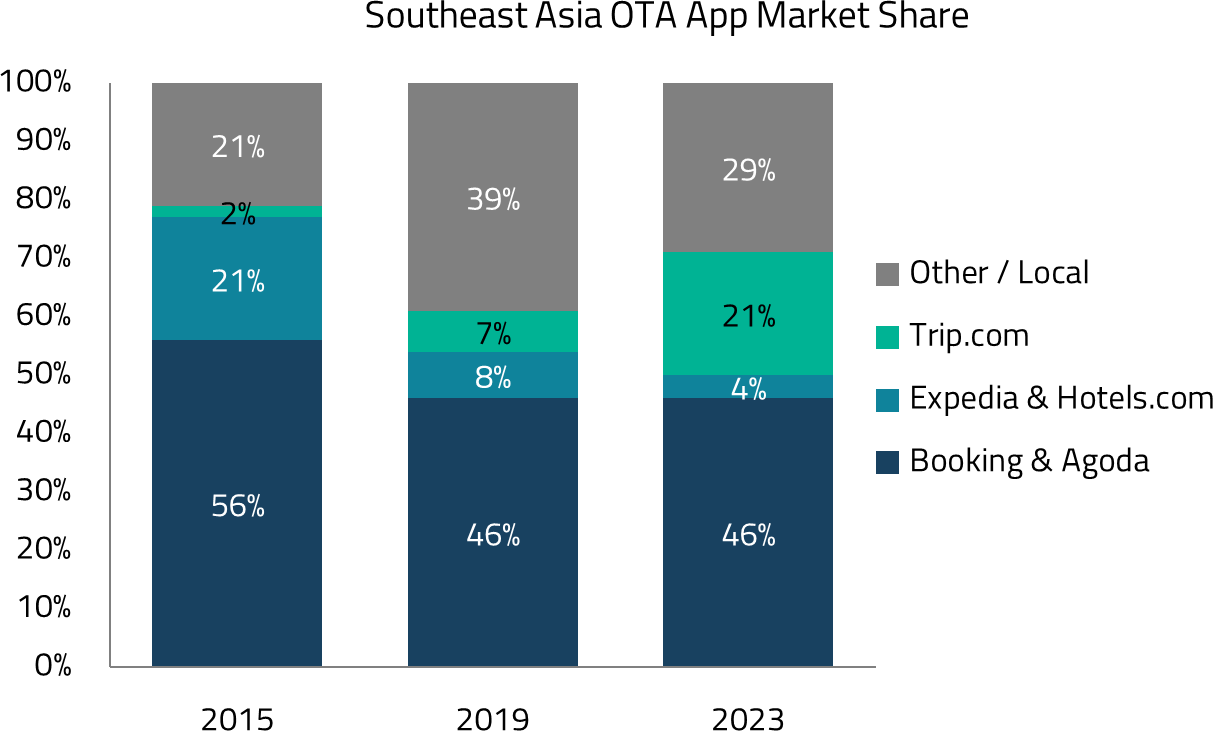

Trip.com Group (TCOM) is another domestic leader with an international expansion story that is seeing tremendous growth. Originating as Ctrip in China, TCOM has effectively leveraged its dominant market share to grow its outbound business, catering to Chinese tourists traveling abroad. TCOM is strategically positioned to improve profitability through multiple levers: 1) by increasing take-rates from current below-market levels, and 2) by optimizing marketing expenses as it achieves greater scale. This measured approach to international growth demonstrates the company’s potential to enhance group-wide margins while expanding its global footprint.

Despite challenging macro conditions, these market leaders exemplify how Chinese companies are successfully expanding both domestically and internationally. By focusing on companies that can consolidate market share, adapt to consumer trends, and explore international expansion, we continue to see sustained growth opportunities within China’s consumer landscape. Moreover, with current valuations not fully reflecting their growth potential and competitive advantages, we see compelling opportunities for long-term investors who can look past near-term market volatility.

Demographic Dividend Meets Economic Momentum

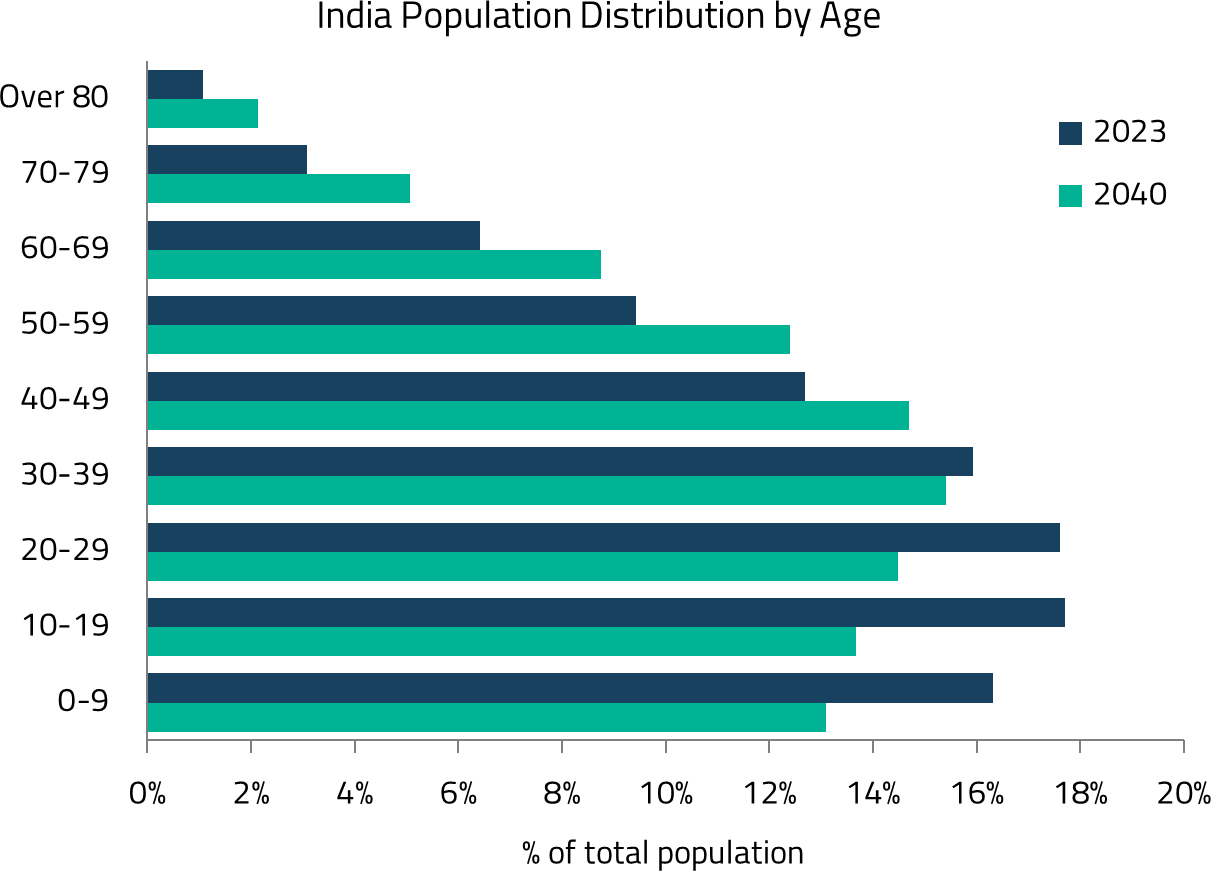

India’s consumption landscape is experiencing incredible momentum driven by powerful demographic tailwinds. As we’d penned in our white paper on India, unlike traditional export-dependent economies, India has built a growth engine powered by consumption from its vast and youthful population. Household consumption contributes to over 60% of GDP, and this trend continues to accelerate as wage growth rises in both urban and rural sectors.6

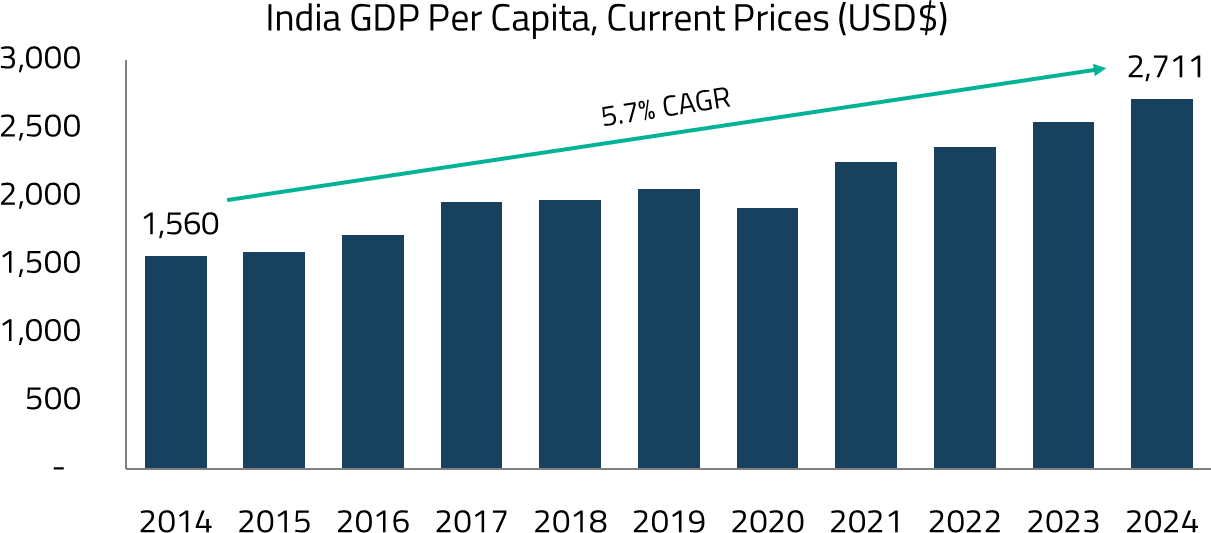

With one of the world’s youngest populations and accelerating urbanization, Indian consumers are rapidly adopting modern retail formats and e-commerce platforms. A significant behavioral shift is underway, exemplified by the explosive growth of quick commerce, which is reshaping traditional shopping patterns. As India’s per capita GDP continues to reach new highs, new discretionary consumption categories will emerge in the coming years.

In the context of geopolitics, India appears to be at the right place, at the right time. India is uniquely positioned in this global economic transition, primarily due to its dual advantage as both a manufacturing destination and a massive consumer market. Unlike previous manufacturing shifts from China and Korea to ASEAN countries, where their smaller markets ultimately led to the current tariffs based on trade deficits, the next wave of manufacturing is moving to India.

India’s large and growing domestic market creates a unique economic equilibrium that supports both export growth and substantial import capacity, providing natural insulation against potential trade pressures. This resilience is underpinned by powerful demographic trends: a growing working-age population that will drive urbanization and income growth over the next two decades.

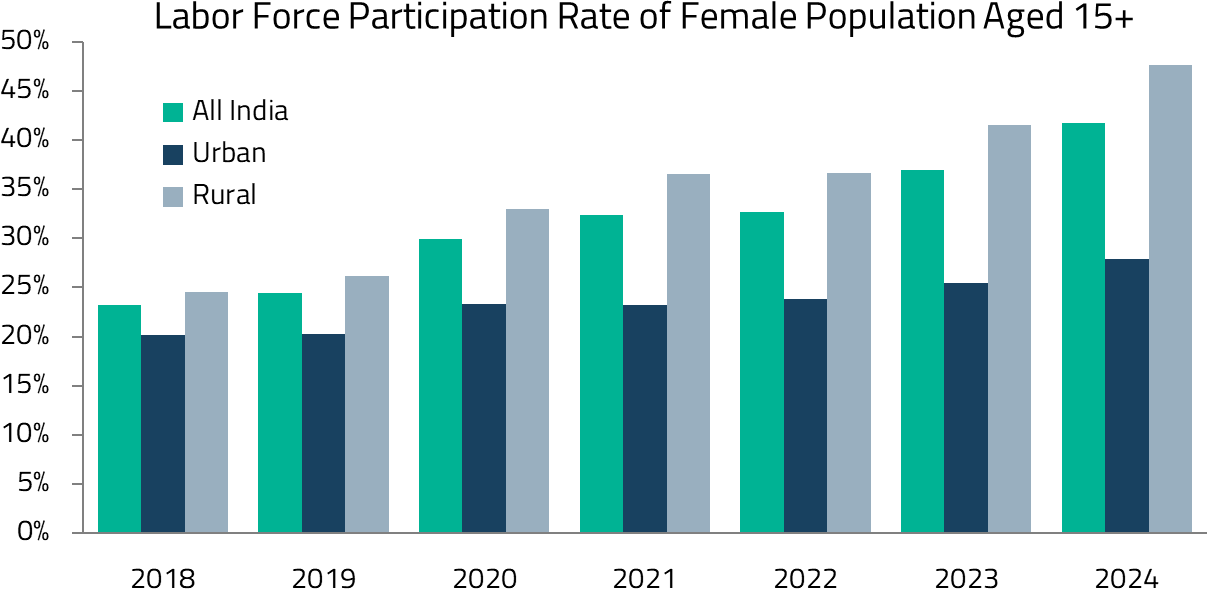

The dramatic rise in female labor force participation, from 23% in 2018 to 42% in 2024, represents a significant acceleration in household wealth creation.7 Furthermore, the ongoing structural shift from agricultural to service and construction sectors is catalyzing the expansion of India’s middle and upper-middle class, reinforcing the country’s consumption growth trajectory.

India’s Emerging Consumption Categories

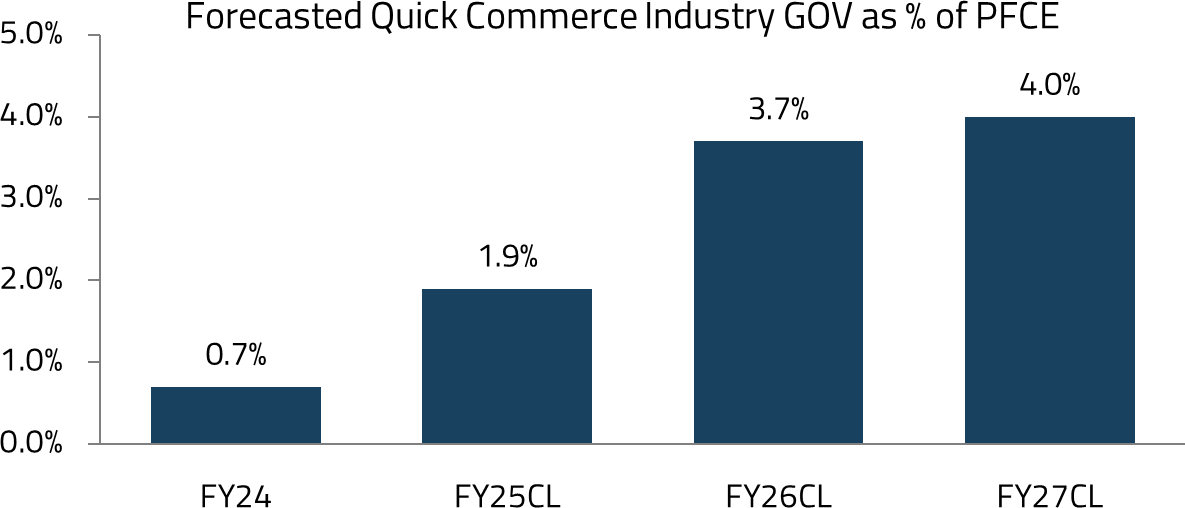

India’s growing middle class is not just saving more—it is spending more. Few expected quick commerce (under 15-minute delivery) to appeal to mass adoption, but it’s undoubtedly becoming the go-to channel for many in the top cities. As Indian consumers prioritize convenience, the quick commerce channel has flourished and is projected to become a USD 34 billion market by 2029 from the current ~5 billion USD in 2024.8

Zomato is leading the way amid the channel transformation as it leverages its know-how from food delivery to efficiently deploy dark stores. Although we expect to see additional competition in the space as companies like Zepto, Instamart, and Flipkart ramp up, quick commerce is a blue ocean market that will likely have meaningful growth for years to come.

Travel and tourism is another category witnessing a surge, driven by increased disposable income and supportive government schemes. India’s online consumer spend is projected to become more than 6x its size from USD 110 billion in 2022 to USD 710 billion in 2030.9 Notably, travel is the second-largest digital spending category after e-commerce.10 The government is playing a key enabling role by improving regional air connectivity, upgrading tourist infrastructure, and promoting lesser-known destinations. Spiritual and heritage tourism, driven by India’s rich cultural tapestry, is also being strategically marketed to international audiences.

Market leader MakeMyTrip demonstrates the sector’s potential, with adjusted operating profit more than doubling over the last two years to USD 178 million in FY25.11 Meanwhile, IndiGo dominates air travel with significant domestic market share as well as globally ranked volume in departures and bookings. Both companies showcase experienced management teams, strong capital positions, and high-margin business models essential for long-term profitability.

As more Indian citizens explore both domestic and international travel, the tourism sector is expected to become a USD 500 billion industry by 2030, contributing meaningfully to employment and GDP growth.12 These trends are not only generating economic activity but are also elevating India’s soft power on the global stage.

For a deeper dive into India’s consumption themes, see our dedicated report – India Consumption: The World’s Next Consumer Powerhouse.

Digital platforms are transforming how consumers access goods and services, democratizing consumption across previously underserved markets. Technology ecosystems throughout ASEAN and Asia broadly enable consumers to leapfrog traditional retail infrastructure limitations that have historically constrained spending.

These platforms provide consumers with access to essential services and commerce, which is particularly valuable in ASEAN markets with fragmented retail landscapes and challenging physical infrastructure. Their ecosystems integrate digital payments, e-commerce, food delivery, and mobility services into unified consumer touchpoints. These digital gateways are also empowering first-time consumers in secondary cities and rural areas to participate in the formal economy, accelerating financial inclusion through integrated payment solutions, and extending critical services like healthcare and education to previously inaccessible regions.

Our approach prioritizes platforms that can leverage network effects to achieve dominant market positions, while fostering deep consumer relationships through a genuine value proposition. Through this approach, we see Sea Ltd and Grab Holdings as the two top opportunities in the region.

Sea Ltd: Southeast Asia’s Leading Digital Ecosystem Platform

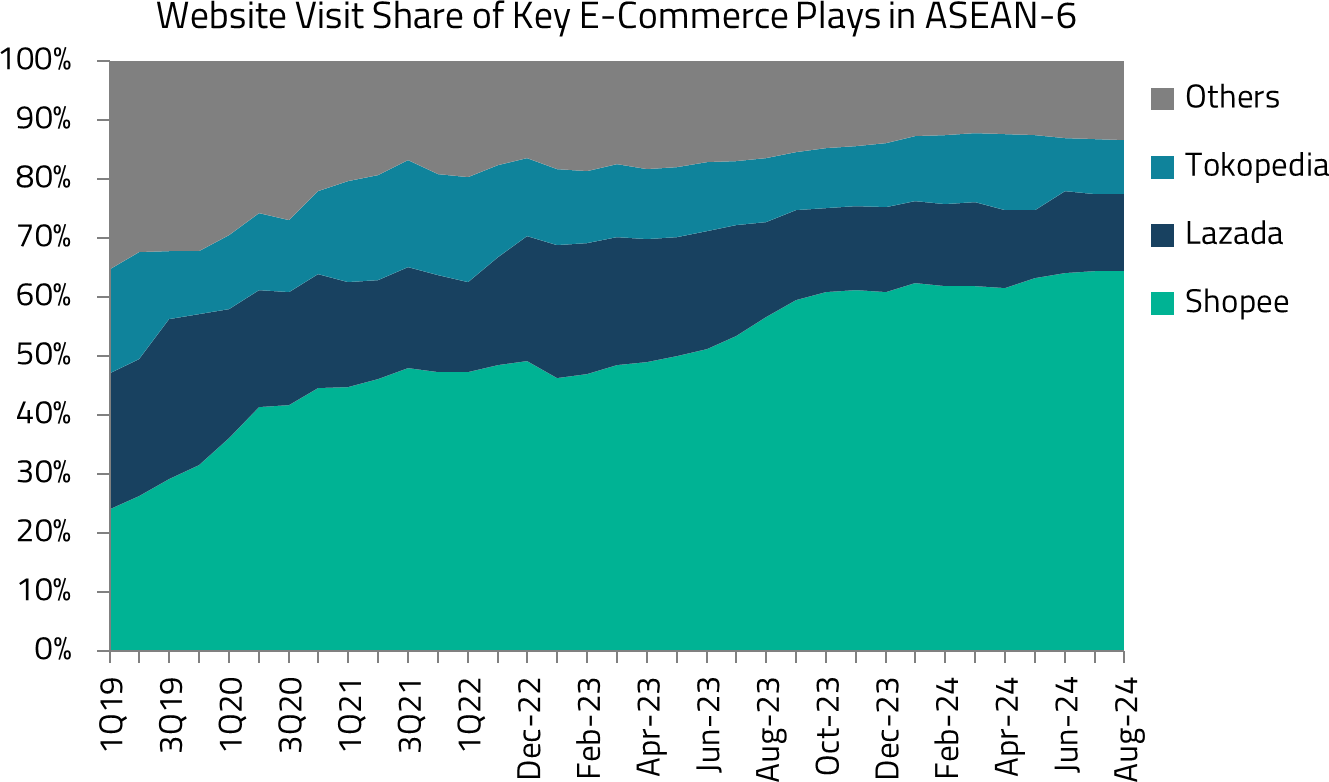

Sea stands as Southeast Asia’s leading digital ecosystem, commanding a dominant position across e-commerce, gaming, and digital financial services. Through its Shopee platform, Sea controls 50-60% of Southeast Asian e-commerce, while successfully expanding into Taiwan and Brazil, demonstrating its ability to replicate its winning formula in diverse markets.13

What makes Sea exceptional is its three-pronged growth engine: digital entertainment through Garena (featuring flagship battle royale game Free Fire), e-commerce via Shopee (offering C2C and B2C marketplaces, Shopee Mall for authorized retailers, and innovative features like livestream shopping), and digital financial services through Monee/ShopeePay (providing digital wallet services, payment processing, buy now pay later or “BNPL”, etc.). The company has also expanded into emerging services like SeaFood delivery and ShopeeExpress logistics.

Shopee’s marketplace is experiencing robust 28% y/y GMV growth, exceeding USD 100 billion in FY24, while steadily improving profitability through raising take rates and advertising revenue.14 The gaming division, anchored by Free Fire’s 100+ million daily active users, provides stable, high-margin cash flows that fund growth initiatives. Meanwhile, the digital financial services arm is rapidly scaling with over 28 million active loan users and loans principal outstanding growing 75% y/y in 1Q 2025.15

Sea employs vertical integration tactics where ShopeePay offers cashback for Shopee purchases, Free Fire players receive rewards for using Shopee, and exclusive in-game items can only be purchased via ShopeePay. The company creates bundled offers during Shopee “Payday Sales” with boosted cashback and free shipping with ShopeePay payments. Its app interface features unified login and Shopee Coins across services, while ecosystem lock-in tactics include Shopee Guarantee escrow requiring platform payment methods and non-transferable ecosystem currency.

These interconnected initiatives demonstrate Sea’s ability in leveraging its vast network effects, allowing the company to efficiently cross-sell services across its ecosystem while simultaneously deepening user engagement and raising switching costs.

Grab: From Rides to Regional Superapp

In contrast to Sea, Grab Holdings has built its ecosystem around mobility services (e.g. ride-hailing), food services (including restaurant deliveries and cloud kitchens), deliveries and logistics (GrabExpress parcel delivery and business logistics solutions), financial services (GrabPay digital wallet, payment processing, insurance, digital banking via GXS Bank, and merchant financing), and comprehensive merchant services (GrabAds, business management tools, and data analytics).

Grab’s cross-selling approach similarly features GrabRewards for multiple service usage, discounted rides after food purchases, and the GrabUnlimited subscription covering various services. Grab bundles meal deals with free delivery and offers discounted airport rides with travel insurance. Its super app interface seamlessly integrates services with a unified GrabPay wallet and contextual recommendations, while loyalty tiers and point expiration drive continued engagement.

While Sea and Grab intersect in financial services, they operate in parallel across the ASEAN region by providing unique and complementary content and services. Sea leverages its e-commerce platform and gaming service for digital transactions, while Grab functions as a super app for more local services. This strategic differentiation allows both companies to thrive in the region, with each addressing distinct consumer needs and enhancing the region’s digital ecosystem.

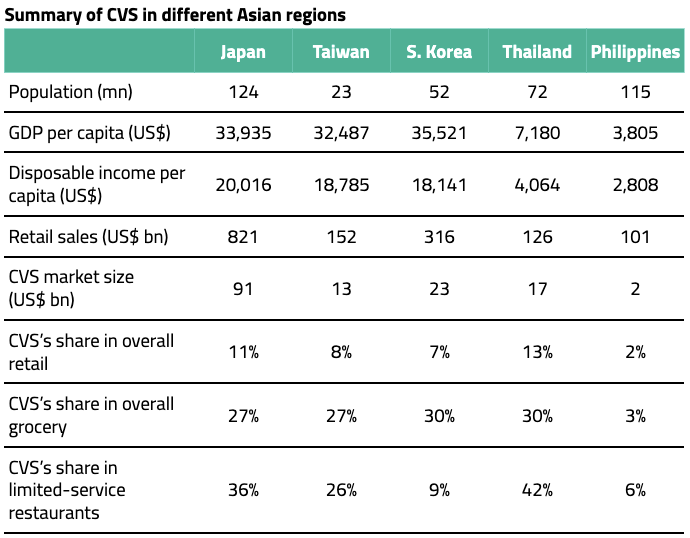

Beyond the digital ecosystems dominated by Sea and Grab, ASEAN markets offer compelling opportunities in traditional retail segments that are undergoing modern transformation. The Philippines presents a particularly interesting case, where despite current low valuations across consumer companies, the modern trade sector shows promise. Philippine Seven (SEVN), operator of 7-Eleven stores, stands out as an interesting investment opportunity. The convenience store channel in the Philippines remains significantly underpenetrated, with each store serving approximately 10,000 people, compared to 2,000-4,000 in more developed markets like Thailand and Taiwan.16 SEVN’s current footprint of 4,200 stores, growing by 500 annually, suggests a substantial runway toward a potential 10,000-store network.17 With store-level payback periods of just 2-3 years generating strong returns on capital employed, we think SEVN shows characteristics of a long-term compounder, following the successful paths of President Chain in Taiwan and CPALL in Thailand.

In Vietnam, several up-and-coming businesses are adopting operating models that mirror the successes seen in other parts of Asia. In the jewelry sector, Phu Nhuan Jewelry (PNJ) is rapidly expanding its store network by adding around 5% each year while maintaining a payback period of 18 to 24 months.18 The gold jewelry market is highly trust-dependent, with customers prioritizing the authenticity of the materials, making branding a key factor when choosing where to shop. PNJ holds a dominant market position and benefits from ongoing market consolidation, as branded jewelry operators account for only about 30% of the total market.19 We believe there is significant growth potential for PNJ to reinvest its capital into expanding its stores and eventually capture over 50% of the market.

Finally, Mobile World Group (MWG) operates in the consumer electronics and groceries segments, with the majority of its future earnings growth coming from the grocery division (BHX). Vietnam’s modern trade grocery penetration was only ~12% in 2022, compared to 30% to 50% in other ASEAN countries, indicating ample room for MWG to expand this segment and achieve a reasonable return on equity (ROE).20 We have observed the mini-mart model succeed in Indonesia with Alfamart, which has effectively replaced traditional wet markets. Similarly, BHX is well-positioned to scale and replicate this success in Vietnam.

The evolution of Asian consumption markets reveals a compelling investment landscape, with each region charting its own path. China is pivoting towards domestic consumption to sustain growth, creating prospects for leading local brands poised for market consolidation and international expansion. Meanwhile, India and ASEAN are emerging as the next consumer hotspots, fueled by demographic dividends and rapid digital transformation. These factors are unlocking significant consumer spending and creating fertile ground for both traditional and innovative business models to thrive.

While these markets are all at different stages of development, they share some common threads: rising middle-class consumption, digital adoption, and the emergence of strong local champions. The winners in this space will be those who can build enduring competitive advantages while scaling alongside Asia’s growing consumer class, presenting exciting long-term investment opportunities across the region.

For sophisticated investors only. For informational purposes only. The information presented in the material is not and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP (“Shikhara”) is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission. This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this material are prepared and maintained by Shikhara and has not been reviewed by the Securities and Exchange Commission of the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.