India, set to become the world’s fourth-largest economy this year, has been experiencing robust economic growth, driving a significant expansion in its middle and upper-middle class. This transformation is fueling a surge in consumer spending, with the country poised to nearly double its consumption by 2030.1 From e-commerce and premium goods to digital services and travel, India’s rising aspirations and youthful, tech-savvy population present unparalleled opportunities. As global markets look east, India is emerging as the epicenter of the next wave of consumer-driven economic growth. In this paper, we explore India’s current consumer landscape and highlight the promising investment themes in this rapidly evolving market.

India’s consumption landscape is experiencing incredible momentum driven by powerful demographic tailwinds. As we’d penned in our white paper on India, unlike traditional export-dependent economies, India has built a growth engine powered by consumption from its vast and youthful population. Household consumption contributes to over 60% of GDP, and this trend continues to accelerate as wage growth rises in both urban and rural sectors.2 Personal income tax revenue has grown at a 16% compound annual growth rate (CAGR), increasing from INR 2.65 trillion in FY15 to INR 10.45 trillion in FY24.3 During this period, the number of taxpayers has also doubled.4

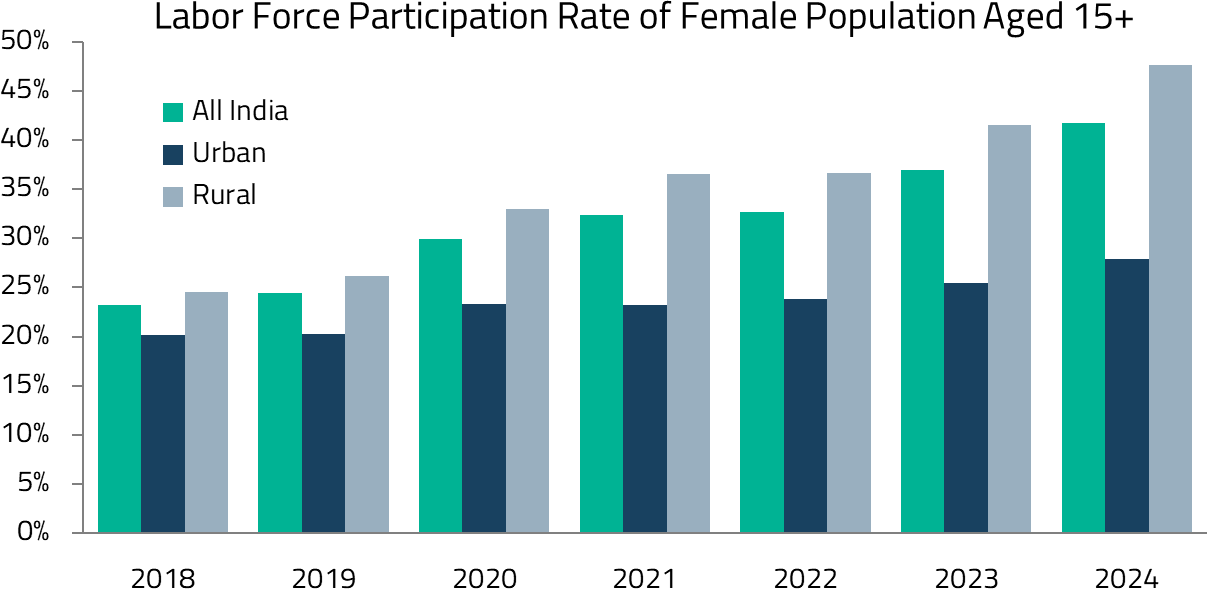

The dramatic rise in female labor force participation, from 23% in 2018 to 42% in 2024, represents a significant acceleration in household wealth creation.5 Furthermore, the ongoing structural shift from agricultural to service and construction sectors is catalyzing the expansion of India’s middle and upper-middle class, reinforcing the country’s consumption growth trajectory as per capita GDP continues to reach new highs. In the near term, structural reforms such as tax cuts and the anticipated implementation of the Eighth Pay Commission should also further bolster consumption growth.

While the macroeconomic outlook appears promising, the on-ground reality presents a more nuanced picture. India is home to the world’s largest Gen-Z and millennial population, with over 730 million individuals who are more literate, tech-savvy, and globally connected than previous generations.6 This demographic shift is accelerating the adoption of global trends and reshaping consumer behavior. Social media has emerged as a powerful force, influencing consumer awareness and aspirations across categories, from fashion and electronics to food and wellness.

Simultaneously, the rapid rise of e-commerce platforms has democratized access to branded and premium products, particularly in smaller towns and rural areas. This improved access, combined with shifting consumer preferences, is intensifying competition across industries as brands vie for market share in this dynamic environment.

We would argue that the heightened competitive intensity is not limited to a few segments but is evident across categories (though the degree would vary). Previously well-moated categories such as paints, groceries, and quick service restaurants (QSR) are now facing disruption, with new entrants gaining market share from incumbents. This shift has led to muted earnings growth and a reassessment of these sectors.

Consequently, while the opportunities are immense, businesses must navigate these complexities to fully capitalize on India’s evolving consumer landscape. For investors, identifying the right segments with palatable competitive intensity becomes all the more critical.

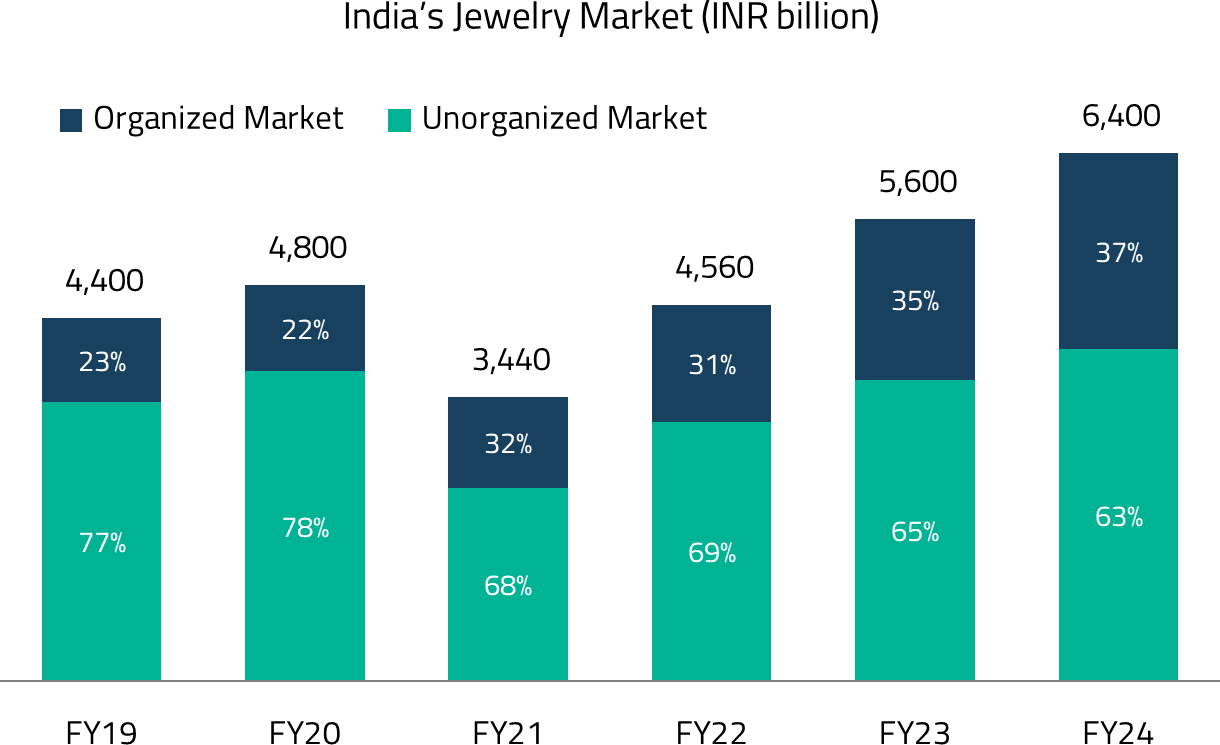

Organized jewelry retailers are witnessing strong demand, fueled by a robust wedding season that accounts for 60% of total jewelry consumption.7 Demand, which began picking up in FY24, has remained strong through FY25, with most retailers reporting double-digit same-store sales growth.8 Consumers are increasingly willing to pay a premium for trust, superior product quality, and an enhanced shopping experience, further solidifying the position of organized players like Tanishq and Kalyan in this thriving market.

What’s driving this demand is India’s vibrant wedding culture. If weddings were categorized as an industry, India’s would be worth approximately USD 130 billion, second only to food and groceries.9 Indians are known for hosting lavish weddings that serve as a display of social status and lifestyle. With around 10 million weddings held annually, celebrations often span several days or even weeks, as seen in recent high-profile events like the Ambani wedding. This dynamic wedding culture actually fuels growth across multiple industries, such as apparel, footwear, luggage, and jewelry. While competitive pressures are increasing in categories like luggage and apparel, we remain bullish on the jewelry segment.

A potential shift we continue to monitor is the rising adoption of lab-grown diamonds (LGDs). The declining costs of LGDs are making them increasingly affordable, now priced at roughly one-tenth the cost of natural diamonds.10 This significant price difference, especially for larger stones, is driving a shift among consumers from natural to lab-grown diamonds.

While LGD adoption could pressure profitability for some retailers like Tanishq, which rely heavily on high-margin solitaires, the overall impact on natural diamonds remains limited due to India’s predominant consumption of smaller stones. Overall, organized jewelry retailers should continue to thrive by leveraging trust, modern designs, and premium experiences, highlighting their ability to adapt to this evolving market landscape.

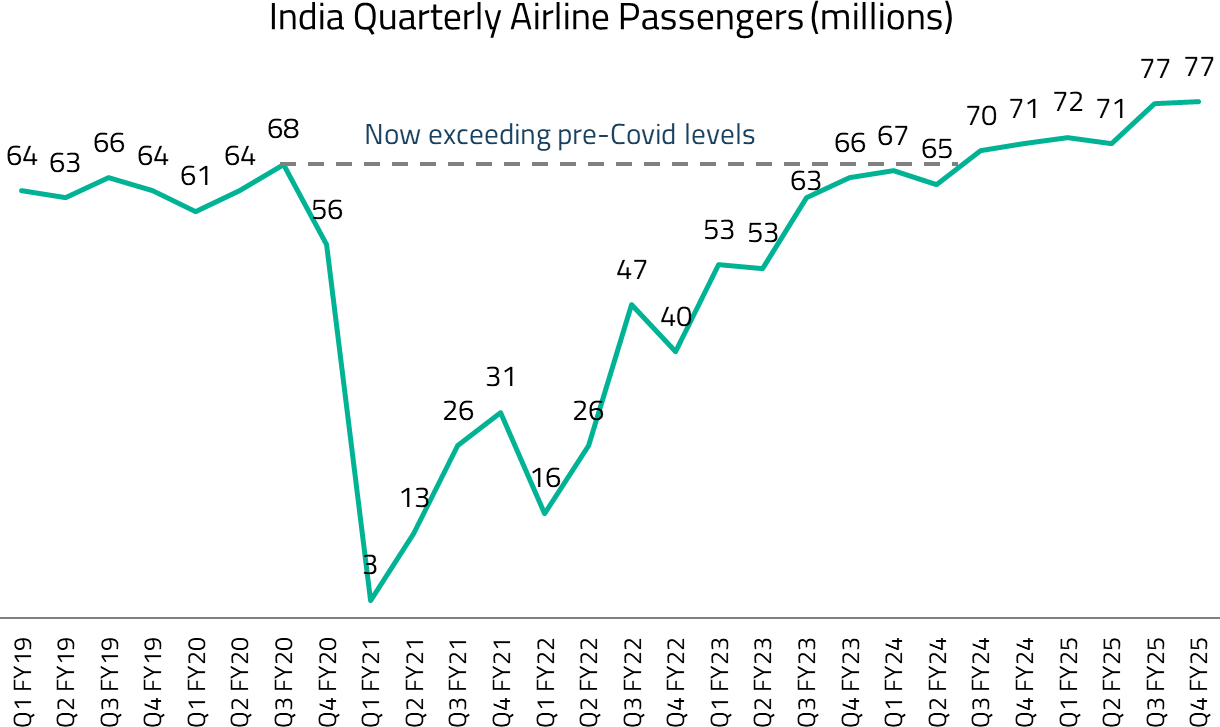

Another promising growth theme in India is travel. While travel demand has normalized from the euphoric highs of 2022-23’s “revenge travel” period, interest in travel remains strong. India’s youthful and aspirational population continues to seek out new destinations, and the widespread influence of social media further fuels this desire for unique experiences. As travel frequencies continue to grow with the rising aspirations and affordability, sectors such as hotels, aviation, and online travel agency (OTA) platforms are well-positioned to benefit from this enduring, secular trend.

The number of operational airports in India has surged from 74 in 2014 to 157 in 2024, reflecting the rapid expansion of the country’s aviation infrastructure.11 With the government targeting 350 to 400 operational airports by 2047, the long-term growth potential of the aviation sector is immense.12 Airlines are already gearing up to meet the rising demand, as evidenced by the large orderbook of Indian aviation players.

InterGlobe Aviation, which operates IndiGo, stands out as an attractive opportunity in this rapidly growing market. As India’s largest passenger airline by market share, IndiGo is renowned for its low-cost carrier model and operational efficiency. It boasts one of the youngest aircraft fleets globally and, in recent years, has been focused on expanding its international routes. Despite its budget positioning, IndiGo maintains a reputation for good service quality, making it well-positioned to capitalize on the sector’s long-term growth trends.

With the pickup in airline passengers, the OTA market has also seen robust growth. These platforms provide a seamless user experience, offering a broad range of choices, particularly in hotel inventory, which is a key differentiator. They also address critical customer pain points, such as instant refunds and predictive tools for ticket confirmation probabilities, enhancing overall convenience and satisfaction.

Market leader, MakeMyTrip, demonstrates the sector’s potential, with adjusted operating profit more than doubling over the last two years to USD 178 million in FY25.13 Renowned for its user-friendly platform and mobile app, the company has also expanded its presence to other countries in South Asia and the Middle East. To strengthen its market position, MakeMyTrip has made key acquisitions, including Goibibo and redBus, cementing its leadership in the region’s online travel ecosystem.

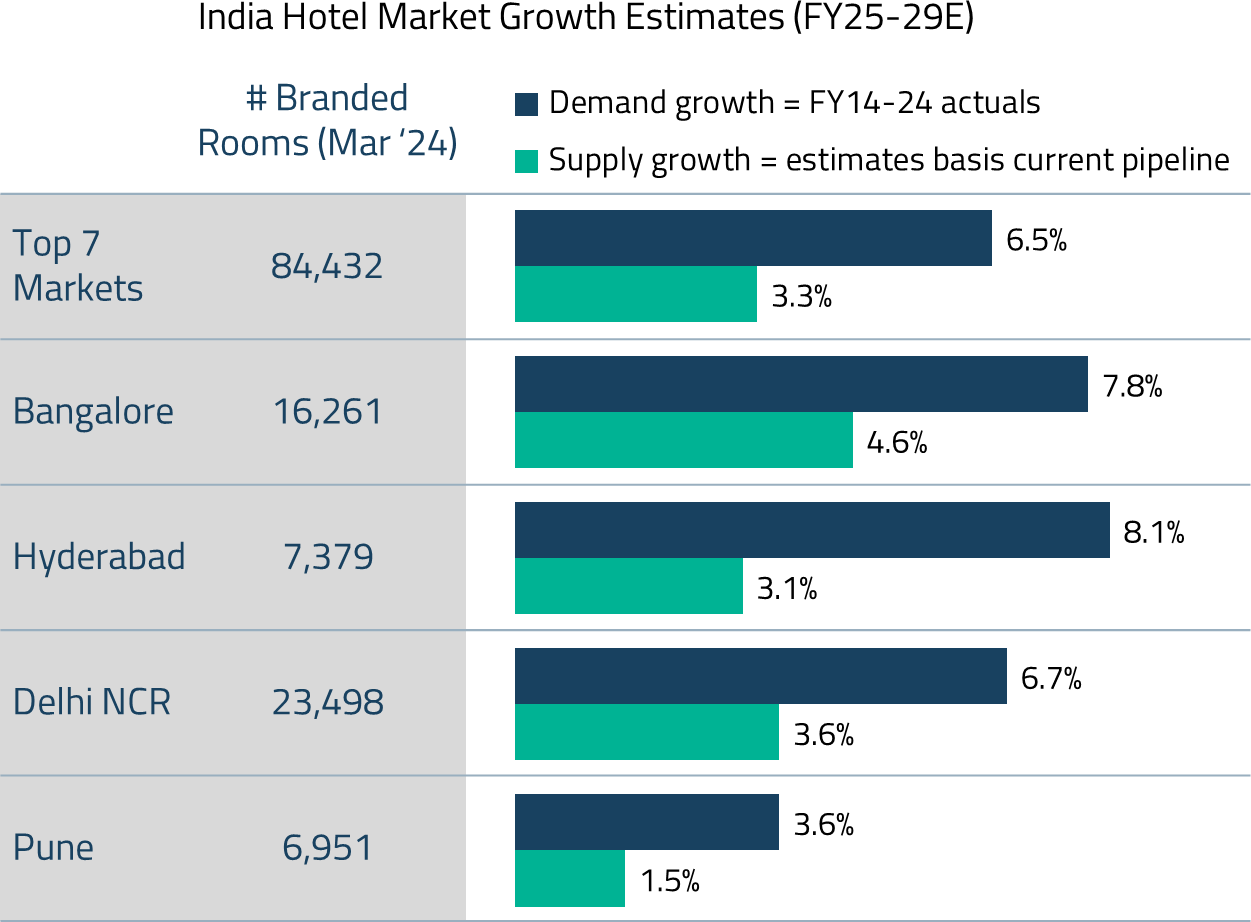

Finally, the hospitality industry in India remains on a firm footing, with demand consistently outpacing the supply of new branded hotel keys. This demand is fueled by a mix of business and leisure travel, staycations, and travel for weddings, conferences, and events. Average Room Rates (ARR) have risen across most markets, driven by robust demand momentum and enhanced pricing power. The dynamics are especially favorable for the luxury and upscale hospitality segments, which face higher barriers to entry due to longer gestation periods and significant capital requirements. This trend is expected to persist, particularly in the top seven cities, where demand remains more predictable and supply growth is notably constrained.

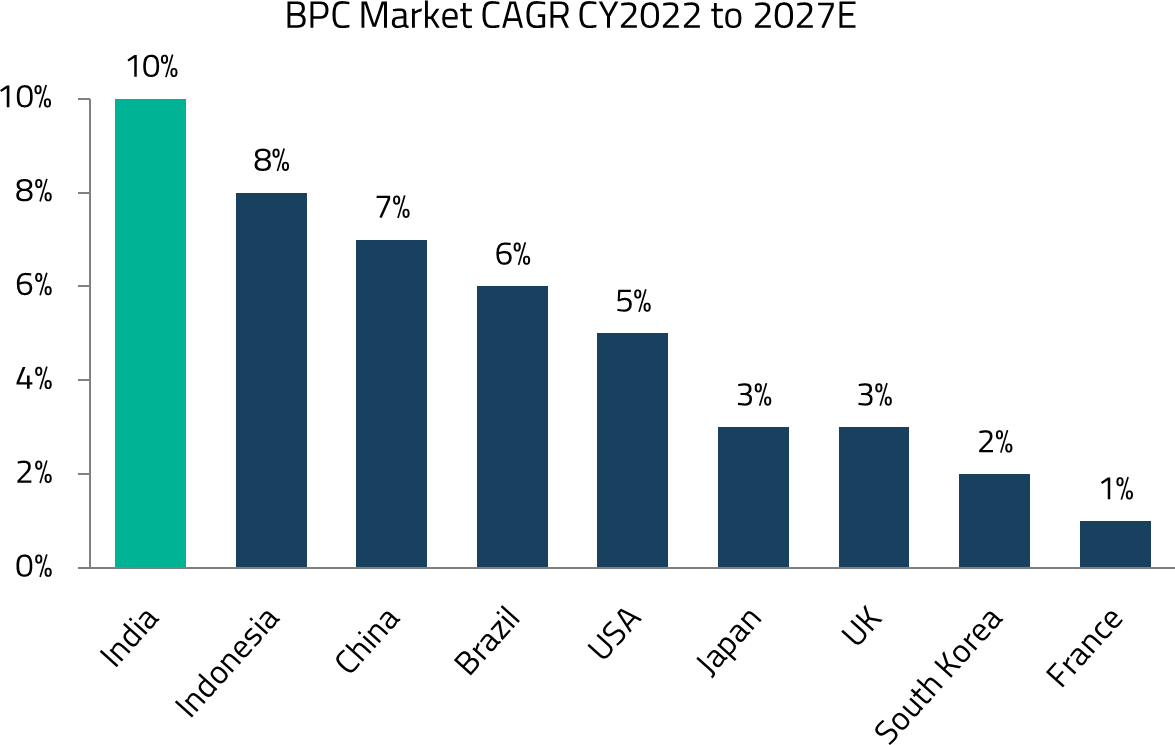

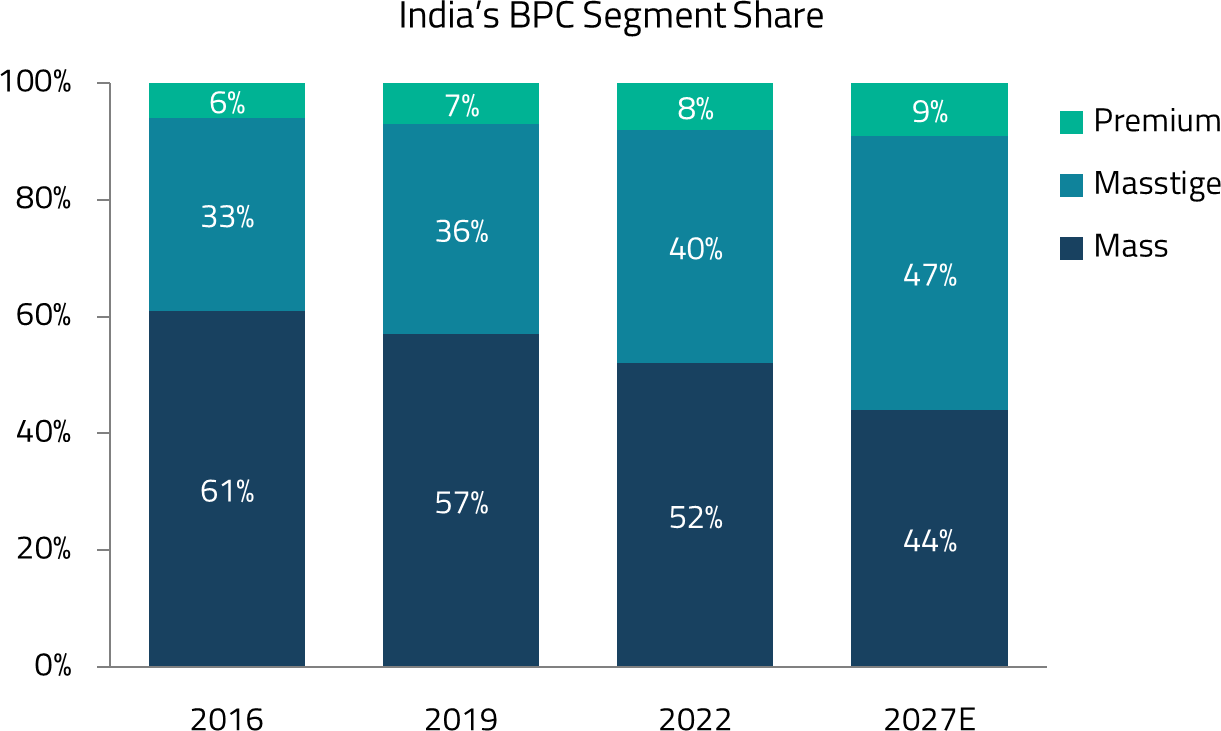

The COVID-19 pandemic provided a significant boost to direct-to-consumer brands at a time when offline retailers were struggling. Among various categories, beauty and personal care (BPC) emerged as one of the most preferred for online sales due to its high average order value (AOV) and attractive gross margins. These high margins are essential for absorbing customer acquisition costs. After establishing a strong online presence, many of these brands are now expanding into offline retail to offer a more comprehensive shopping experience.

The influx of new brands has accelerated market expansion at a rapid pace. Additionally, the rise in female labor force participation has further fueled category growth. We believe BPC is one of the fastest-growing categories, particularly in the mass-premium and luxury segments. While the overall BPC market grows at a low double-digit rate, the online channel is expanding at nearly twice that pace.14 Nykaa, India’s leading omnichannel BPC retailer, is a clear beneficiary of this trend, leveraging its extensive product portfolio, strong brand partnerships, and seamless shopping experience to capitalize on increasing online adoption.

However, with numerous brands vying for the same ~50 million premium customer base, competition has intensified, leading to a significant rise in advertising expenditures.15 To sustain their growth ambitions, many companies now face a difficult trade-off between prioritizing growth or profitability. While the focus during the COVID era was on “growth at all costs”, the landscape has shifted as funding avenues have tightened, prompting companies to adopt a more measured, profitability-driven approach.

Among the few success stories, Honasa, the parent company of brands like Mamaearth and The Derma Co., stands out. Known for its focus on natural, toxin-free, and dermatologist-approved products, Honasa has effectively scaled by leveraging its strong capabilities in identifying emerging consumer trends and executing highly targeted digital marketing strategies. While Honasa has excelled in the digital realm, unlocking its next phase of growth will hinge on mastering offline distribution and establishing a robust omnichannel presence.

We have greater confidence in backing online retailers like Nykaa over Honasa. BPC customers often exhibit limited brand loyalty, frequently shifting from one trend to the next. However, Nykaa has successfully positioned itself as a premium shopping destination with a strong and loyal customer base, giving it a significant competitive advantage. The platform’s extensive selection of 6,800 brands not only reinforces its appeal to consumers but also solidifies its market position by attracting higher advertising spending from brands eager to capitalize on Nykaa’s reach and influence.16 This combination of customer loyalty, vast product offerings, and robust advertiser demand creates a powerful competitive moat for the company.

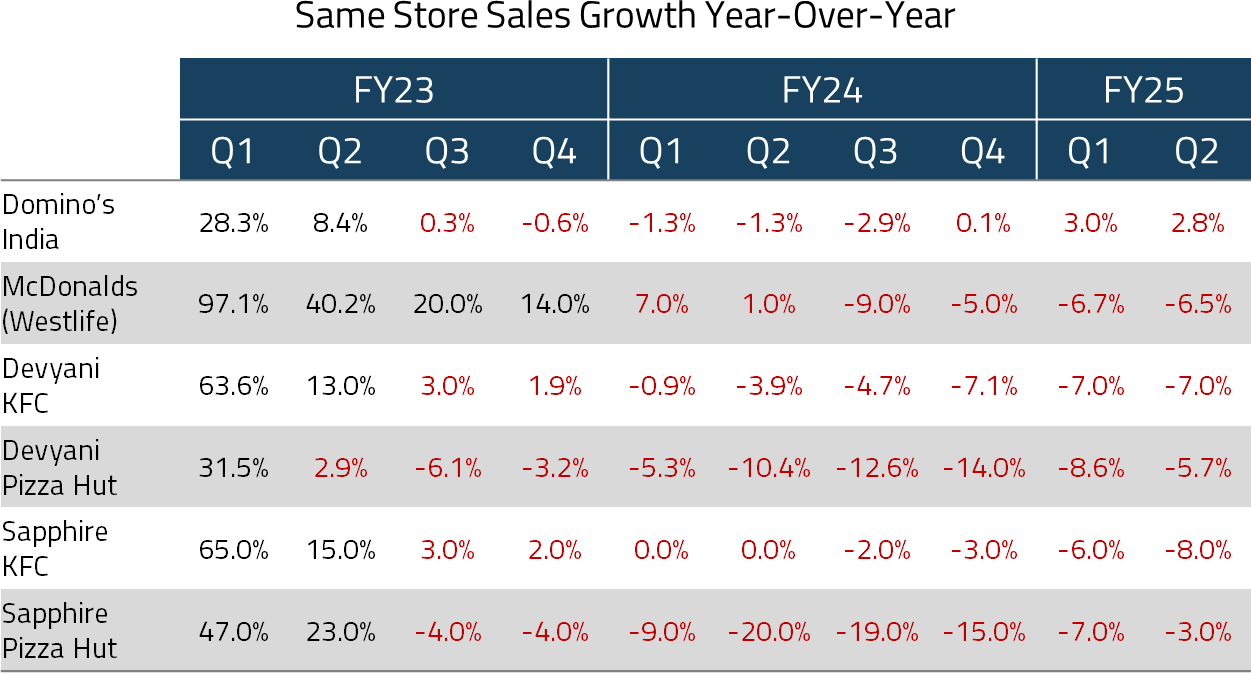

India’s Quick Service Restaurant (QSR) sector has been grappling with challenges as consumers now enjoy a broader range of choices and unparalleled convenience through food delivery platforms. A notable overlap exists between QSRs and food aggregators, with both deriving the majority of their business from the top 10 cities, intensifying competition for consumer attention.

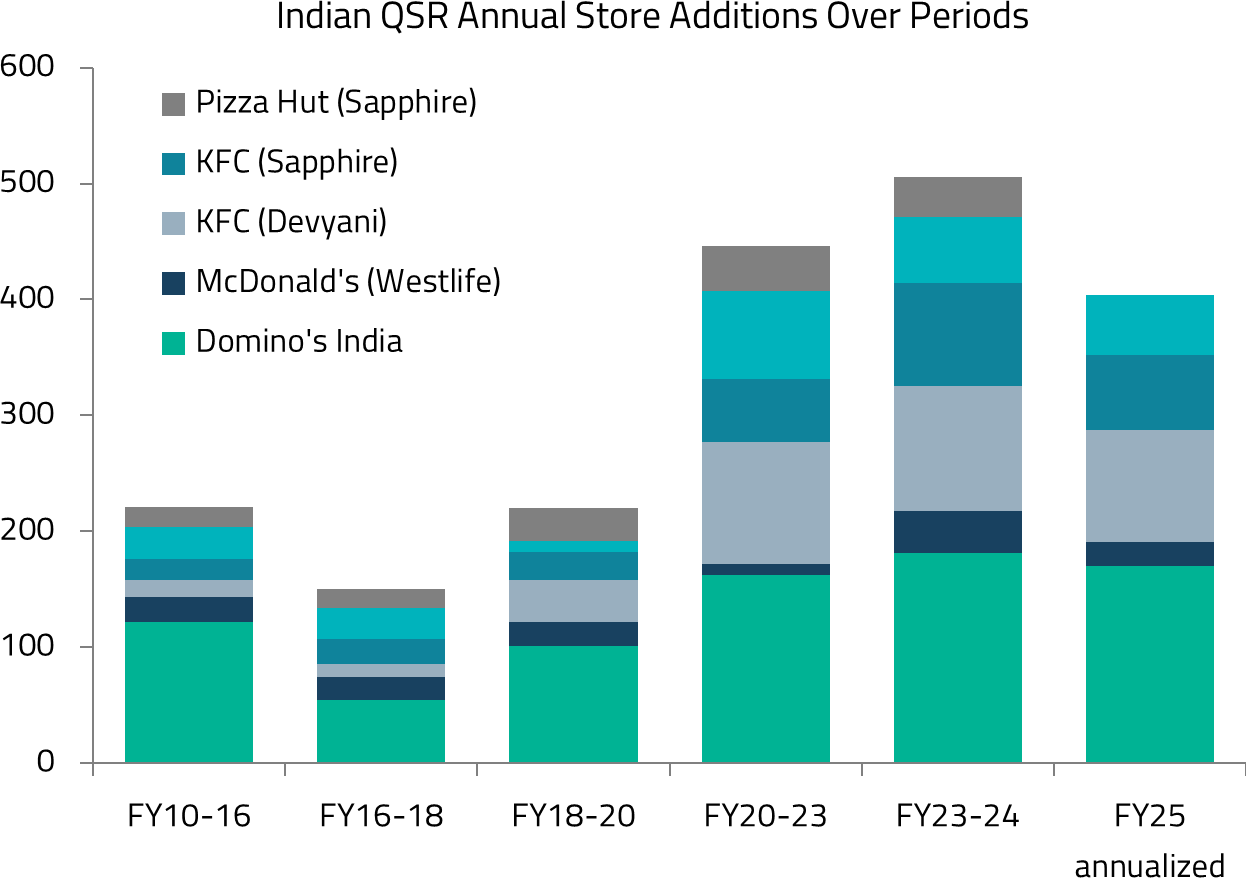

Another key factor contributing to the decline in same-store sales growth (SSG) has been the aggressive store expansion by QSR players post-pandemic. While this expansion was aimed at capturing market share, it has inadvertently led to cannibalization of sales between nearby stores and heightened competitive intensity. As a result, the combination of demand shifting towards food aggregators and rising competition has weakened overall demand and adversely impacted store-level economics for many QSR operators.

Despite these headwinds, one company that stands out is Domino’s, which has managed to deliver double-digit SSG thanks to strategic initiatives aimed at reviving demand.17 The company has focused on brand building, waived delivery fees, introduced product innovations, and maintained stable pricing for two consecutive years. While these investments have temporarily pressured profitability, Domino’s is well-positioned to benefit in the long run due to its high operating leverage.

Domino’s operates with a distinct advantage—a delivery-focused model. Unlike most QSRs, Domino’s has successfully cultivated a loyal customer base that frequently uses its proprietary app for placing orders. Supported by strong technological capabilities and a dense network of delivery-focused stores, Domino’s ensures faster delivery times, which enhances customer satisfaction. This operational model provides the company with a sustainable competitive edge that is difficult for competitors to replicate.

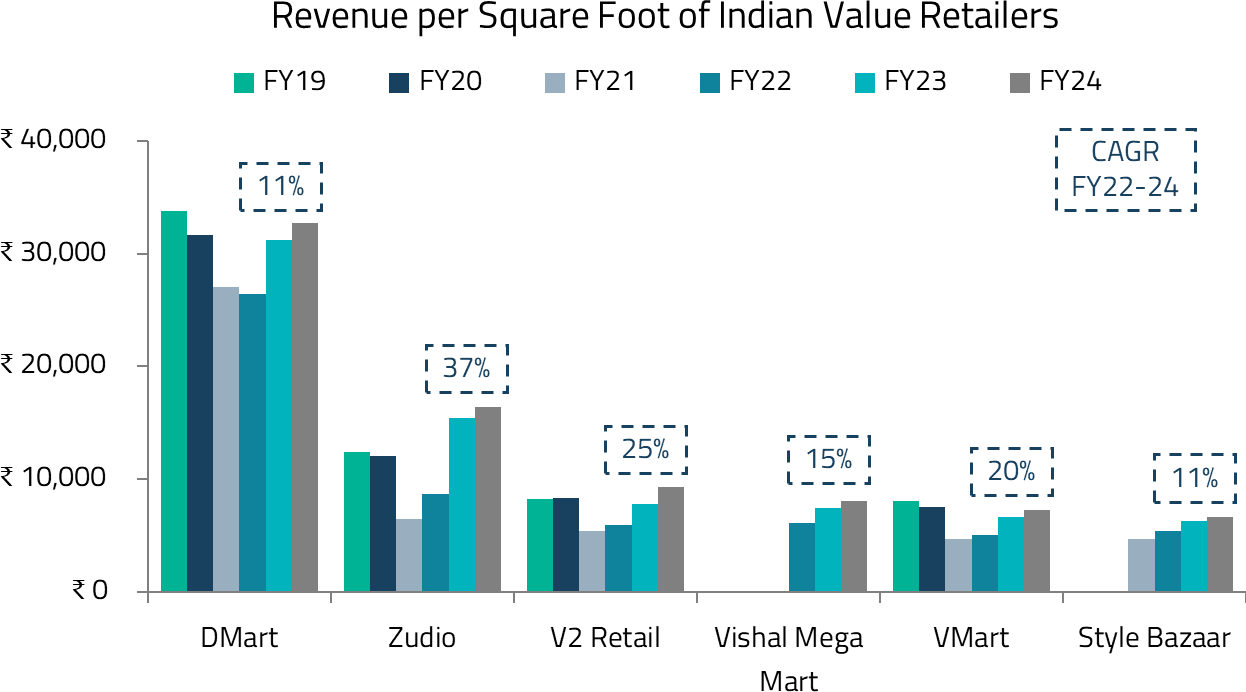

While consumers worldwide seek value (i.e. quality products at affordable prices), this preference is especially pronounced in India, where affordability remains a key constraint for the majority of the population. Market leaders across various categories have successfully catered to this value-conscious segment, including Voltas in air conditioners, MI in smartphones, and Maruti in passenger vehicles.

However, value retailers like V-Mart and V2 Retail struggle to differentiate themselves in this highly competitive segment. Most players rely on similar sourcing partners, resulting in little to no distinction in product offerings. This lack of differentiation, combined with cyclicality driven by rural demand fluctuations and competitive intensity, makes it challenging to build a strong, long-term investment case for these players.

In contrast, Zudio has emerged as a standout performer in recent years. Unlike many other value retailers that predominantly focus on Tier 2 and smaller towns, Zudio has strategically concentrated its expansion efforts in metro and Tier 1 cities. Its unique approach—offering stylish, high-quality products at exceptionally low prices—creates a “kid in a candy shop” shopping experience, resonating strongly with urban consumers.

We believe Zudio’s success lies in its well-honed design and supply chain capabilities, which enable it to deliver superior products while maintaining affordability. These capabilities are difficult to replicate, giving Zudio a sustainable competitive advantage and setting it apart from other value players in the market.

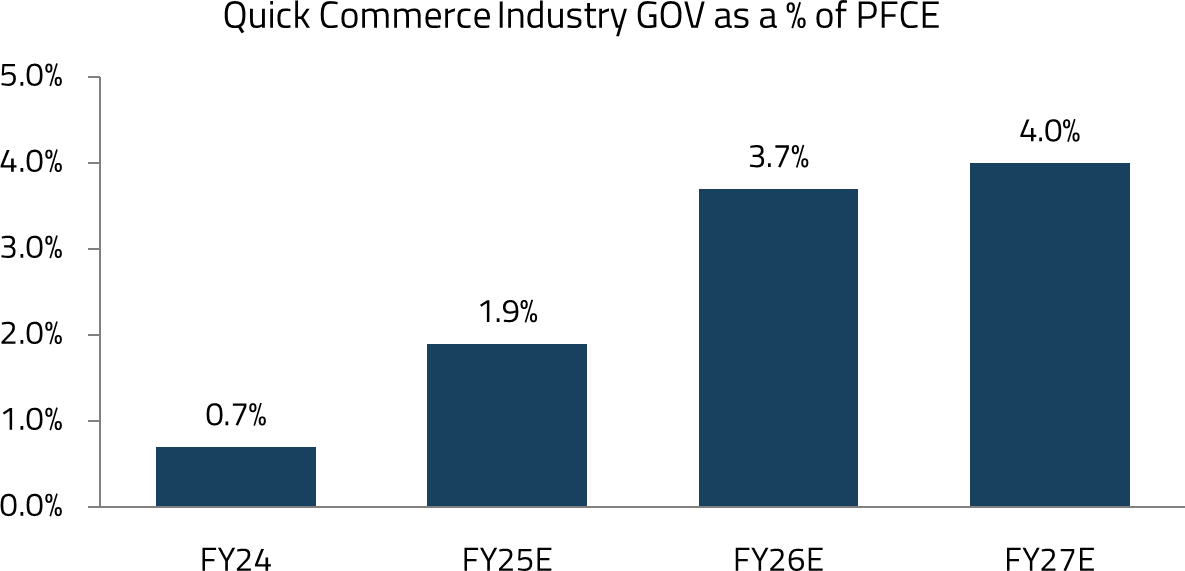

When quick commerce first emerged, it was met with skepticism from investors, who questioned both the necessity of 10-minute deliveries and the viability of the business model. However, over the past year, these concerns have largely been addressed. Once consumers experience the unparalleled convenience of rapid delivery, it quickly becomes an ingrained habit, driving strong customer loyalty and repeat usage.

Surprisingly, products such as bed sheets and mobile phones, previously considered impractical for ultra-fast delivery (under 15 minutes), are now being sold successfully, underscoring the adaptability and potential of this growing sector. In our view, quick commerce represents the ideal retail format, combining the convenience and proximity of traditional “mom-and-pop” stores with the extensive SKU range of e-commerce and modern trade.

The expansion into discretionary categories has not only increased the total addressable market but has also improved store-level economics. These higher-value items drive up the average order value, leading to greater absolute gross profit per transaction. Additionally, the strong demand for fresh groceries provides a further boost to gross margins. While few expected the mass adoption of ultra-fast deliveries, quick commerce is rapidly becoming the go-to shopping channel in major cities.

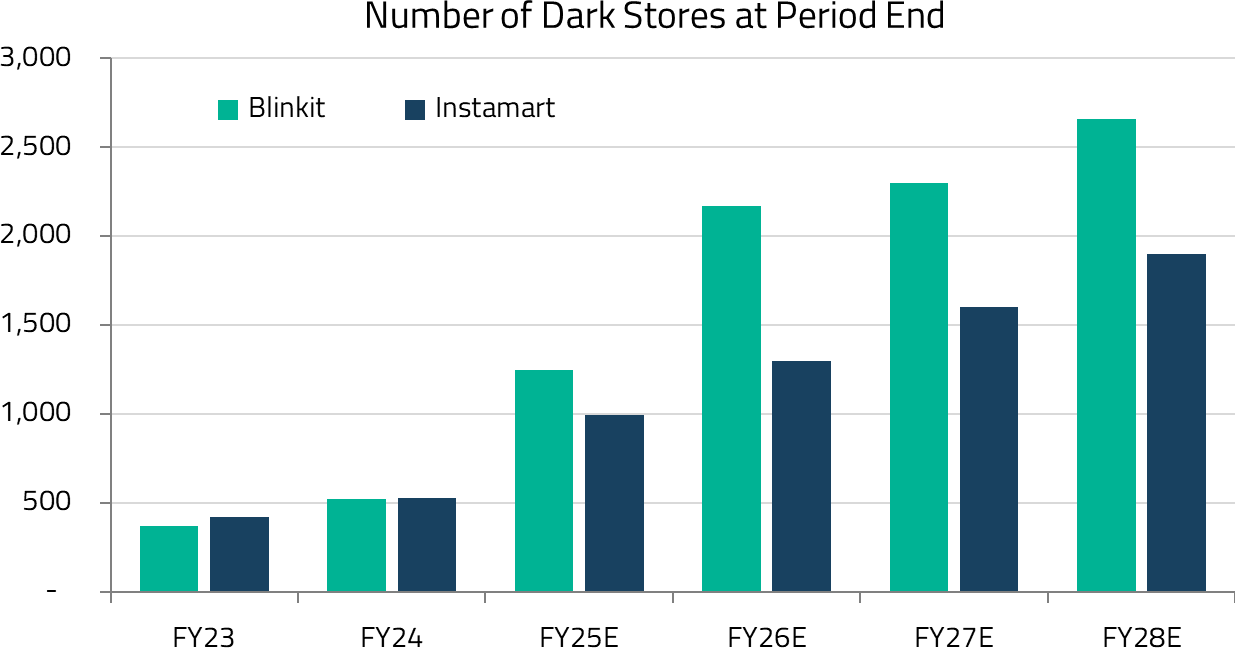

As confidence in both demand and unit economics grows, quick commerce players are aggressively expanding their store networks. Zomato (Blinkit) is leading the charge, while competitors like Zepto and Swiggy (Instamart) are close behind. Flipkart has also entered the space with “Flipkart Minutes”, and all of these players are aggressively expanding their dark store networks.

Given the immense market opportunity and strong initial operational metrics, we remain highly optimistic about the industry’s long-term growth potential. However, aggressive expansion and rising competitive intensity would weigh down on the margin profile of the sector in the near term.

As the next leg of India’s consumer story unfolds, the key to successful investing lies in identifying sectors where competitive dynamics remain favorable and growth trajectories are sustainable. While increased competition and evolving consumer preferences present challenges across many segments, select opportunities in jewelry retail, travel, quick commerce, and beauty & personal care offer compelling investment cases.

Companies that can maintain their competitive moats while adapting to changing market dynamics will likely emerge as the primary beneficiaries of India’s consumption boom. For investors seeking exposure to this transformative growth story, a selective approach focused on market leaders with proven execution capabilities will be crucial in navigating this dynamic landscape.

For sophisticated investors only. For informational purposes only. The information presented in the material is not and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP (“Shikhara”) is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission. This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this material are prepared and maintained by Shikhara and has not been reviewed by the Securities and Exchange Commission of the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.