History rarely repeats, but it often rhymes in unexpected combinations. Today’s investment landscape offers a new cocktail on the menu: AI-led productivity gains that remind us of the 1920s, blended with a geopolitical race to dominate emerging technologies reminiscent of the 1950s. This duality – innovation accelerating while nation-states compete for strategic advantage – defines the opportunity set before us. In this report, we reflect on what drove our strong 2025 performance, share our outlook for 2026, and explain how we are positioning to navigate a world that is, once again, investing in its future. Enjoy!

The MSCI All Country Asia Ex-Japan Index was up 15.89% (in USD terms1) for the second half of 2025, bringing full-year returns to 33.02%. Relative to the rest of the region, South Korea and Taiwan were the top-performing markets in H2, while the Philippines and India were the laggards. Sector-wise, IT and Materials led performance in H2, while Consumer Staples and Real Estate were the worst performers.

MSCI China gained 11.93% in H2 2025, bringing full-year returns to 31.37%. Q3, in particular, saw a strong rally, driven by AI and tech sector optimism, policy support, and momentum-driven buying after persistent underweight positioning. The US-China trade agreement in late October also eased geopolitical tensions and supported risk appetite. The 15th Five-Year Plan, released at the Fourth Plenum in October, reaffirmed Beijing’s focus on advanced manufacturing, AI infrastructure, and green transition. From a macro perspective, China’s GDP grew 5.2% y/y in the first three quarters, meeting expectations but reflecting moderating momentum amid weak domestic demand. However, exports proved resilient as manufacturers successfully diversified away from the US market: China’s annual trade surplus exceeded USD 1 trillion for the first time in history, with exports to Europe, Southeast Asia, and Africa more than offsetting the plunge in shipments to the US.

Indian equities were the regional laggard in H2, declining 2.12%, though full-year returns remained positive at 4.29%. Foreign portfolio investors continued their selling streak throughout the year, marking the worst year on record with total net outflows of USD 18.9 billion.2 However, the market stabilized in Q4, supported by robust domestic fundamentals. Q2 FY26 GDP (July to September) came in at a stronger-than-expected 8.2% y/y (the fastest pace in six quarters) with manufacturing expanding 9.1% and services 9.2%. India’s inflation trajectory was notable: CPI eased to just 0.25% y/y in October, a record low in the current series, driven by a sharp moderation in food prices, but edged up to 0.71% y/y in November. The Reserve Bank of India (RBI) delivered a 25bp rate cut in December, bringing the repo rate to 5.25%, and upgraded its FY26 GDP forecast to 7.3%.

South Korea was the standout performer in H2 2025, with equities surging 43.72%, bringing full-year returns to 100.76% – the best among major global equity markets. The KOSPI broke through the symbolic 4,000 level in October and continued climbing to fresh record highs in December, powered by the AI-driven memory semiconductor supercycle. SK Hynix and Samsung Electronics led gains as HBM demand from AI accelerators outstripped supply. Beyond semiconductors, the market benefited from President Lee’s Corporate Value-up Program (CVP), continued progress on US-Korea trade negotiations, and resilient defense and shipbuilding sectors. Full-year exports reached a record USD 709.7 billion, up 3.8%, with December shipments surging 13.4% y/y.

Taiwanese equities rallied 26.63% in H2, bringing full-year returns to 39.84%. The TAIEX extended its winning streak to new highs, underpinned by continued AI-related capital expenditure from US hyperscalers and a robust earnings season from TSMC and key supply chain players. TSMC delivered strong earnings beats with full-year guidance upgrades, while power supply stocks rallied on Nvidia’s push for gigawatt AI factories. The market experienced a brief pullback in November amid a global reassessment of AI valuations, but recovered as expectations for Fed rate cuts and Nvidia’s strong earnings reaffirmed confidence in AI demand.

ASEAN markets delivered mixed performance in H2. Thailand staged a remarkable comeback, surging 23.40% in H2 after being the worst performer in H1, as both local and foreign investors judged that much of the bad news had been priced in. The rally accelerated following the appointment of Prime Minister Anutin Charnvirakul in September and the unveiling of a clearer political transition framework. Malaysia gained 15.12% in H2, supported by commodity strength and a rebound in consumer discretionary names. Singapore returned 9.35%, benefiting from strong bank earnings, inflows into REITs, and ongoing MAS-SGX reform initiatives to revitalize the equity. Indonesia posted a modest gain of 1.56%, supported by 5.04% GDP growth in Q3 and resilient domestic consumption, though foreign flows remained subdued. The Philippines was the weakest performer, declining 4.46% in H2, as political tensions and muted foreign buying weighed on sentiment despite the central bank easing.

Through all the volatility and uncertainties of 2025, we could not be more proud of our team’s ability to navigate the landscape with discipline and insight, delivering strong performance for the Fund. While the results speak for themselves, we think reflection is always essential. The Investment Team convened before the holidays to reflect thoughtfully on what contributed to our successes, where we fell short, and how we can refine our approach to drive even better outcomes in the year ahead.

First, three clear themes worked well for us this year that we will continue –

Next, here are the lessons we’ll be taking into 2026 –

Overall, we’re giving ourselves a pat on the back for the strong year in 2025. Our stock picking was disciplined, our thought leadership was perceptive, and we called the right trends at the right time. However, we remain grounded and focused on improvements, so we’ll be reflecting on these lessons throughout the new year.

We believe the global economy has entered a new industrial era. Much like the transformative period of the 1950s – when the space race, interstate highways, and early computing laid the foundations for decades of growth – the world is investing again. The secular stagnation that characterized much of the post-GFC decade is behind us. Countries are now focused on national and regional building, e.g., the US is rebuilding its manufacturing and infrastructure base, Europe is investing in defense and energy security, and India is running parallel consumption and investment cycles. Meanwhile, China is pivoting from investment-led growth toward consumption – a healthy rebalancing that remains underappreciated by the market.

Yes, there will be noise – geopolitical tensions, policy shifts, and occasional moments where we miss a heartbeat. But the overarching direction is constructive. Earnings revisions are trending positively, productivity gains from AI adoption are on the horizon, and decades of underinvestment have created latent demand for capital spending across critical sectors.

That said, we are mindful of key risks heading into 2026 –

A significant shift in global capital flows is underway. After two years of strong NASDAQ performance in 2023 and 2024, US tech lagged emerging markets (EMs) in 2025, particularly in the back half of the year. The early weeks of 2026 have reinforced this trend – NASDAQ names are struggling to touch new highs, while Asian and EM equities are seeing strong bids.

This rotation is driven by fundamentals. Stocks trade on earnings growth momentum and return on equity (ROE). US hyperscalers are investing heavily in AI infrastructure – capex that is essential to their long-term competitiveness but will weigh on near-term ROEs and earnings growth. The market is recognizing this and rotating toward more capital-efficient users of AI, i.e., the adopters rather than the enablers, such as Asian consumer internet names.

Deglobalization is also accelerating this shift. As nations become more inward-looking and prioritize building local capacity, governments are actively working to bring capital back home. Korea recently announced a new tax incentive plan to encourage the return of overseas investment capital to domestic markets. Once one government moves, others follow – we saw this with capital market reforms, where Korea followed Japan’s Corporate Governance Code playbook. Japan will likely implement similar measures to help manage JGB yields. Capital that had been parked in the US will increasingly be attracted back to home markets.

The implications are significant. The US was the disproportionate beneficiary of global capital flows over the past decade. While it will remain the bulk of global portfolio allocations, the complacency of holding ~65-70% US weightings will now be questioned. At the margin, flows are turning negative for the US (especially NASDAQ) and positive for EMs and precious metals.

Geopolitical tensions remain elevated across multiple fronts – the US, Latin America, Europe, the Middle East, and Asia. The recent US-Venezuela situation bears watching, but our sense is that the tensions are contained and unlikely to escalate beyond regional boundaries.

From an investment perspective, the implication is that government defense spending will increase. If countries choose to address geopolitical uncertainty by strengthening their industrial-military complexes, that is positive for jobs and investment. Korean and Indian defense contractors, shipbuilders, and industrial champions are well-positioned to benefit.

We are also monitoring policy developments in the US. Recent statements about limiting dividends, stock buybacks, and executive compensation in the defense industry, and restricting institutional purchases of single-family homes are reminiscent of China in 2021, when the government intervened in real estate and private education. From a societal perspective, such measures may make sense. But if implemented with a sledgehammer approach, they risk dampening animal spirits. These developments add to the uncertainty around US assets and, at the margin, will encourage investors to diversify exposure away from the US.

AI infrastructure investment remains a dominant theme. Total global data center capex through 2028 is forecast at USD 2.9 trillion.3 Of this, roughly USD 1.4 trillion is expected from the Mag 7 hyperscalers. But the remaining USD 1.5 trillion represents a funding gap that will need to be filled by external capital from credit markets, private equity, and sovereign sources.

As we have emphasized in prior commentaries, we continue to favor AI adopters over pure enablers. The hyperscalers must invest to remain competitive – but the economic returns from that investment are more likely to accrue to companies deploying AI to enhance customer experiences, improve operational efficiency, and capture market share.

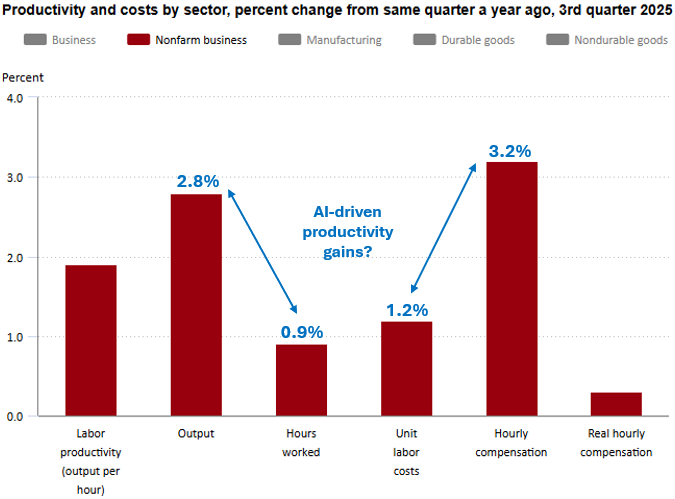

Early evidence suggests AI is already delivering tangible productivity gains. US nonfarm business sector labor productivity surged 4.9% in Q3 2025, driven by 5.4% output growth while hours worked increased just 0.5%.4 Crucially, unit labor costs declined 1.9% in Q3 despite wage increases, as productivity gains more than offset compensation growth.5 These metrics suggest that AI adoption is beginning to translate into meaningful economic returns – validating our focus on companies that can effectively deploy these technologies rather than simply build them.

A central question for 2026 is where AI value will ultimately accrue: to incumbent consumer internet platforms that successfully integrate AI into their existing businesses, or to the large language model (LLM) providers themselves who capture value at the model layer?

The landscape is already shifting in certain sectors. In travel, OpenAI’s October 2025 launch of ChatGPT Apps gave Booking.com and Expedia direct integration with ChatGPT’s 800 million weekly active users – allowing travelers to search for hotels, compare prices, and view itineraries without leaving the chat interface.6 Agentic AI tools like ChatGPT’s Agent Mode can now complete bookings end-to-end, raising the question of whether online travel agents/aggregators (OTAs) risk becoming mere fulfillment arms of LLM platforms. Nearly a third of ChatGPT’s first app partners were OTAs – a clear signal that conversational AI is not displacing incumbents so much as becoming the next distribution layer.

In search, the disruption is more structural. Zero-click searches now account for nearly 60% of Google’s mobile queries, and AI overviews increasingly form part of processed search results, summarizing information before users ever visit publisher sites.7

The incumbents have powerful advantages: large, engaged user bases, rich behavioral data, established monetization engines, and the ability to deploy AI to enhance hyper-personalization, ad targeting, and operational efficiency. We are already seeing evidence of this. Tencent’s Q3 2025 results showed that AI-powered ad targeting contributed roughly half of its 21% y/y growth in marketing services revenue – one of the first detailed quantifications of AI’s economic impact from a major platform.

That said, LLM platforms are not standing still. The aggressive user-acquisition tactics we observed in 2025 (e.g. OpenAI’s ChatGPT Go promotions in India, Perplexity’s Airtel partnership, Google Gemini bundled with Jio) echo the early ride-hailing playbook, where subsidized usage was used to seed habits before pivoting to monetization. As mass adoption deepens, casual users may remain on free tiers, but power users and enterprises deriving tangible productivity gains will convert to paid plans, if not already.

The winners in 2026 will be those who deploy agentic AI to deepen user engagement and operational efficiency. We are watching closely for evidence of successful AI monetization beyond the model layer – and for now, our positioning favors incumbents with durable franchises, scale advantages, and clear paths to convert AI capabilities into revenue.

The growth-versus-value debate is particularly nuanced in today’s environment. On the growth side, elevated funding costs create natural headwinds. Investors may tolerate stretched valuations for early-stage companies with genuinely disruptive potential, but mid-cycle discipline will be necessary. Not every growth story will compound through higher rates – we are selective, favoring companies with clear paths to profitability and the balance sheet strength to weather volatility.

On the value side, the risk of “value traps” is heightened when AI-driven disruption threatens to render certain business models obsolete. A cheap stock is not necessarily a good investment if its industry is facing structural decline. Instead, we look for companies that remain critical for the future – businesses with durable competitive positions, essential infrastructure roles, or the operational flexibility to adapt to technological change.

Our investment approach is deliberately unconstrained, spanning the growth-value spectrum to capture the best opportunities. Selectivity is key on both sides of the spectrum. We favor disruptors and firms with the balance sheet and operational flexibility to become the “last man standing” even if overall demand softens. And we remain vigilant against overpaying for growth or being lured by optically cheap valuations in structurally challenged sectors.

| Key Markets | Outlook |

|---|---|

| China | Neutral: Our China stance is neutral, balancing near-term tailwinds against medium-term uncertainties. In the near term, markets are benefiting from breathing room on US tech restrictions. The easing of semiconductor export controls and a more constructive tone following the Trump-Xi summit have supported sentiment. RMB appreciation and Beijing’s renewed focus on consumption revival are positive for select consumer discretionary names – particularly those with pricing power and strong brand loyalty in categories where consumers remain willing to spend despite deflationary pressures.

Medium-term, however, trade tensions will persist. Deep economic interdependence limits the scope for full decoupling – the US relies on China for critical inputs, including rare earths and battery materials, while China cannot afford the social instability that would accompany a sharp export contraction. But the relationship will remain transactional and subject to periodic flare-ups. We remain selective, focusing on companies with defensible global market access: category leaders expanding into the Global South, platforms monetizing AI to deepen consumer engagement, and exporters with diversified customer bases that can navigate tariff uncertainty. |

| India | Overweight: The delayed trade deal pushes out any near-term re-rating catalyst, but we think this creates attractive entry points for patient, long-term investors. India remains a compelling structural story: a large, domestically oriented market with sovereign debt levels under control and a rare ability to sustain 8-10% growth over the next decade.

Domestically, the outlook is also improving. Fiscal easing, GST rationalization, and a pickup in foreign direct investment (FDI) are supporting growth. India has secured USD 135 billion in FDI commitments in 2025 amid an investment surge, most notably from tech giants Google, Microsoft, and Amazon, whose cumulative commitments exceed USD 70 billion.8 Our India exposure is focused on domestic cyclicals and consumption plays, including leading private sector banks and consumer platforms that are uniquely positioned to capture India’s expanding middle class. As the global recovery cycle matures and North Asian valuations become stretched, capital typically rotates into domestically driven economies like India. We are positioning for that rotation. |

| Korea | Overweight: Despite strong performance in 2025, we see room to run. Valuations at ~10x forward P/E sit at the 20-year average, which is reasonable for a market on the cusp of a multi-year growth cycle in industrials and technology.

Korea has emerged as an indispensable partner in the global reindustrialization theme. If the US is intent on reducing reliance on China, who will fill the gap for needs in defense, power grid upgrades, and industrial capacity? Korean industrials are the natural answer: they possess preserved heavy-industry ecosystems, access to cost-efficient inputs, deep engineering know-how, and a long track record of execution with developed-market clients. Order books in shipbuilding, defense, and power equipment now stretch into the late 2020s – far longer than a normal cycle. The Corporate Value-up agenda provides an additional catalyst. Greater parliamentary stability under the new administration is refocusing attention on governance reform, capital returns, and minority shareholder protections. We remain constructive on Korean exposure, with positions across tech, power infrastructure, shipbuilding, and defense. |

From a sector perspective, we would look to maintain an overweight stance across Consumer Discretionary, select Industrials, and Healthcare, while reducing exposure to AI/Semiconductors in 2026. Consumer discretionary offers attractive risk-reward after earnings expectations reset lower, with China’s policy pivot toward domestic demand and India’s GST rationalization providing tailwinds. Korean industrials remain core holdings, benefiting from reindustrialization themes, defense spending, and infrastructure upgrades with multi-year order visibility. Healthcare provides defensive characteristics with secular growth potential, particularly as Asian pharmaceutical companies gain global market share through innovation. We would look to trim AI enablers after their strong run, rotating toward AI adopters that are converting capabilities into tangible revenue gains rather than depending on continued capex buildout momentum.

Beyond our near-term outlook, we believe the investment landscape itself is undergoing a fundamental transformation that plays to our strengths. The boundaries between sectors are blurring much faster than before. Amazon was a retailer; now it is a technology company. The future leaders of the auto industry may well be tech companies, like Waymo and Pony AI in the driverless car space. In a world where tech companies are becoming consumer companies and vice versa, the old frameworks no longer apply. A siloed approach to business analysis – evaluating a company purely through its sector lens – misses the crosscurrents that increasingly define competitive dynamics.

This is where our edge lies – in our superior reaction function. We focus on getting medium-term trends right while not trying to compete in the near-term, noisy part of the market dominated by quant funds and pods. Not being active while markets are live gives us the headspace to see the big picture clearly. It allows us to see the forest for the trees.

Getting our calls right in 2025 required an unlearning. What worked in the last decade – lower cost of capital, capital account surpluses flowing from the West – no longer applies in a world reshaped by geopolitics. While capital remains available, it is increasingly restricted by geopolitical considerations, and the assumptions that underpinned the previous cycle must be questioned. So, we learned from financial history – studying the trade wars and protectionism of the 1920s and 1930s, the massive government-led investment cycles and space race of the 1950s and 1960s, and the Plaza Accord and market crises of the 1980s and 1990s. This gives us a solid grip on the macro.

On the micro, our investment process is built around evaluating companies from multiple angles. When assessing a business, we put ourselves in the founder’s shoes: Would we run the business in the same way? Is this company prepared for the radical disruption that may come in the next three to five years? Our investment team regularly debates these questions for stocks across sectors, continuously enhancing our ability to identify trends early and assess sustainability over the coming decade.

That is the edge we bring to the table, and it is why we believe we are well-positioned to continue delivering for our investors in the years ahead.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return, and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Private Placement Memorandum for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The MSCI AC Asia ex Japan Index captures large and mid-cap representation across Developed Markets (DM) countries (excluding Japan) and Emerging Markets (EM) countries in Asia. The index covers approximately 85% of the free float-adjusted market capitalization in each country. The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips, and foreign listings (e.g. ADRs). The index covers about 85% of the Chinese equity universe.

The contents of this material are prepared and maintained by Shikhara and have not been reviewed by the Securities and Exchange Commission of the United States.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom and the European Union and pending registration in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.