India’s 2025 underperformance masks a structural transformation gaining momentum beneath the surface. While global markets chased AI enablers and infrastructure plays, we maintained our focus on AI adopters and domestic cyclicals – a contrarian stance that we believe will prove prescient as capital rotates toward companies deploying rather than building technology. In this report, we examine the lessons from a challenging but instructive year, explore why India’s policy pivot creates compelling opportunities ahead, and outline how we’re positioning for what we expect to be a meaningful recovery in 2026. The best opportunities often emerge when sentiment is most pessimistic!

Indian equities were the regional laggard in H2, declining 2.12% (in USD terms1), though full-year returns remained positive at 4.29%. Sector-wise, Consumer Discretionary and Materials were the top performers, while Real Estate and Utilities were the laggards.

Foreign portfolio investors continued their selling streak throughout the year, marking the worst year on record with total net outflows of USD 18.9 billion.2 However, the market stabilized in Q4, supported by robust domestic fundamentals. Q2 FY26 GDP (July to September) came in at a stronger-than-expected 8.2% y/y (the fastest pace in six quarters) with manufacturing expanding 9.1% and services 9.2%.

Activity indicators softened towards year-end but remained firmly expansionary. Manufacturing purchasing manager’s index (PMI) eased to 55.0 in December (vs 56.6 in November), its lowest reading in 38 months, as export order growth moderated amid tariff uncertainties.3 Services PMI slipped to 58.0 (vs 59.8 in November), an 11-month low, though still well above the 50 threshold separating expansion from contraction.4

Despite equity outflows, India secured a record USD 135 billion in foreign direct investment (FDI) commitments during the year, with global corporations including Google, Microsoft, and Amazon collectively pledging over USD 70 billion across technology, semiconductors, automobiles, and energy.5 FDI inflows rose 16% to USD 50.4 billion in the April–September period, with the government expecting overall inflows to exceed USD 100 billion for the first time in FY26.6

Consumption turned decisively in H2, especially auto retail sales, which rose 7.7% in calendar year 2025 to 28.2 million units.7 While the January-August period remained muted due to cautious consumer spending and selective financing approvals, demand rebounded sharply from September following GST 2.0 rate rationalization, which reduced taxes on mass-market vehicles, including small cars, two-wheelers, and three-wheelers. December delivered a particularly strong finish, with overall auto retail sales surging 14.6% y/y, led by passenger vehicles (+26.6%) and commercial vehicles (+24.6%).8

India’s inflation trajectory was notable: CPI eased to just 0.25% y/y in October, a record low in the current series, driven by a sharp moderation in food prices, but edged up to 0.71% y/y in November. The Reserve Bank of India (RBI) delivered a 25bp rate cut in December, bringing the repo rate to 5.25%, and upgraded its FY26 GDP forecast to 7.3%.

Through all the volatility and uncertainties of 2025, we could not be more proud of our team’s ability to navigate the landscape with discipline and insight, delivering resilient performance across our strategies. While the results speak for themselves, we think reflection is always essential. The Investment Team convened before the holidays to reflect thoughtfully on what contributed to our successes, where we fell short, and how we can refine our approach to drive even better outcomes in the year ahead.

First, three clear themes worked well for us this year that we will continue –

Next, here are the lessons we’ll be taking into 2026 –

Overall, a difficult year in 2025, but the portfolio showed signs of resilience. Our stock picking was disciplined, our thought leadership was perceptive, and we remained true to our investment approach. In the near term, we’re willing to sacrifice short-term performance rather than chase stocks in businesses we lack confidence in. Protecting downside and foregoing cyclical upside when conviction is absent remains crucial to our approach – if you’re right on the medium-term trajectory, the returns will inevitably follow.

Here we provide a summary of the key themes shaping our view heading into 2026. For our full global macro outlook, please refer to our Asia Half-Yearly commentary for H2 2025.

Today’s investment landscape offers a new cocktail on the menu: AI-led productivity gains that remind us of the 1920s, blended with a geopolitical race to dominate emerging technologies reminiscent of the 1950s. The secular stagnation of the post-GFC decade is behind us, with countries now focused on national and regional building. India is particularly well-positioned, running parallel consumption and investment cycles that should drive sustained growth.

Key risks to monitor include rising JGB yields triggering yen carry trade unwinding, elevated sovereign debt dynamics in developed markets creating persistent capital costs, and tightened liquidity conditions that may create periodic volatility but also opportunities for fundamental investors.

A significant shift in global capital flows is underway. After strong NASDAQ performance in 2023-2024, US tech lagged emerging markets in 2025, with Asian and EM equities seeing strong bids in early 2026. This rotation is driven by:

While geopolitical tensions remain elevated, we expect them to stay contained regionally. The investment implication is increased government defense spending globally, benefiting Indian defense contractors, shipbuilders, and industrial champions. Recent US policy discussions around limiting corporate actions in defense and housing sectors add uncertainty to US assets, encouraging geographic diversification.

The USD 2.9 trillion global data center capex forecast through 2028 includes a USD 1.5 trillion funding gap beyond Mag 7 spending.9 We continue favoring AI adopters over enablers, with early productivity data validating this approach – US productivity surged 4.9% in Q3 2025 while unit labor costs declined despite wage growth.10

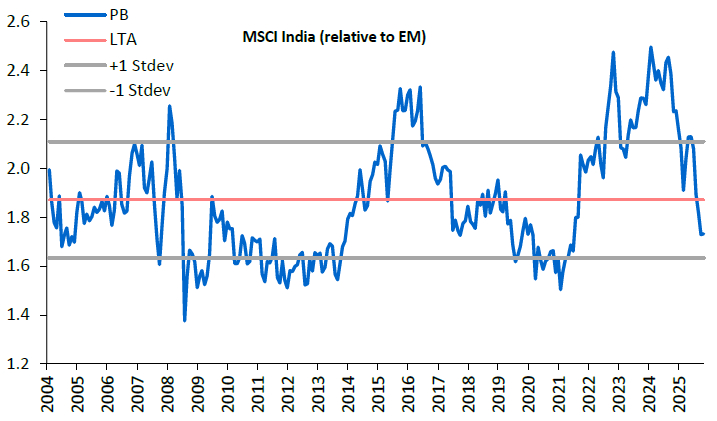

We are optimistic about India for 2026, viewing current conditions as creating attractive entry points for patient, long-term investors. While the delayed US trade deal removes a near-term re-rating catalyst, the underlying structural story remains compelling: India offers a large, domestically oriented market with sovereign debt levels under control and a rare ability to sustain 8-10% growth over the next decade.

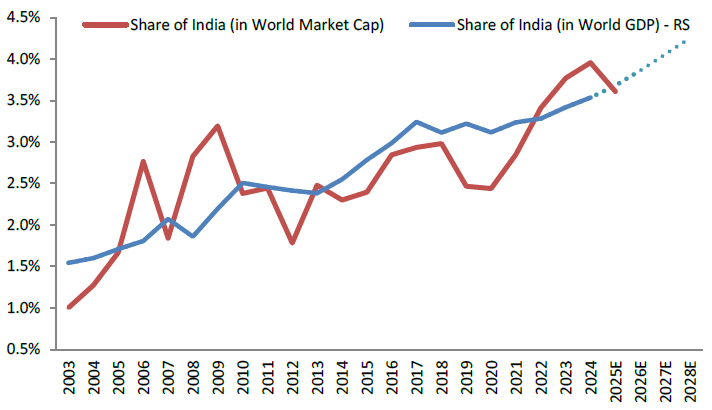

The domestic outlook is significantly improving. Fiscal easing measures, GST rationalization, and a notable pickup in foreign direct investment are providing strong growth tailwinds. India secured USD 135 billion in FDI commitments in 2025 amid a pronounced investment surge, with tech giants Google, Microsoft, and Amazon contributing over USD 70 billion in cumulative commitments.11 This validates our thesis that global capital is recognizing India’s long-term potential despite near-term volatility.

As the global recovery cycle matures and North Asian valuations become increasingly stretched, we expect capital to rotate into domestically driven economies such as India. This rotation typically favors markets with strong domestic demand drivers and structural growth stories – precisely India’s positioning.

Domestically, the policy pivot toward reflation has been decisive. The government and RBI have coordinated unprecedented stimulus measures, including rate cuts, cash reserve ratio (CRR) reductions, bank deregulation, front-loaded capex spending, and GST rate cuts targeting mass consumption.

India’s transformation continues through improved macro stability, world-class digital infrastructure, and declining oil intensity. The country’s rising export share, particularly in services, combined with fiscal consolidation, creates space for private investment to flourish while reducing external vulnerabilities.

Our India exposure focuses on domestic cyclicals and consumption plays, positioning for both India’s internal growth story and its emerging role in global supply chains. We target leading private-sector banks, consumer platforms serving the expanding middle class, industrial companies benefiting from manufacturing growth, and healthcare companies benefiting from rising penetration.

Overall, we view India’s current positioning as setting the stage for a meaningful recovery. The convergence of supportive policy, compelling valuations, and India’s deepening integration into global supply chains reinforces our conviction in the country’s long-term prospects.

India’s investment landscape is undergoing a shift that plays to our strengths. The boundaries between sectors are blurring much faster than before, particularly in India’s dynamic economy. Companies like Reliance have evolved from energy conglomerates into technology and retail platforms, while fintech players are becoming full-service financial institutions. In a world where tech companies are becoming consumer companies and vice versa, the old frameworks no longer apply. A siloed approach to business analysis – evaluating a company purely through its sector lens – misses the crosscurrents that increasingly define competitive dynamics in India’s rapidly evolving market.

Our edge lies in our reaction function and global perspective. With teams in Hong Kong, New York, and Mumbai, we analyze competitive dynamics across markets to understand their implications for India. We focus on getting medium-term trends right, avoiding the noise of near-term, algorithm-driven markets. Not being active while markets are live gives us the headspace to see the bigger picture – to see the forest for the trees.

On the micro level, our investment process evaluates Indian companies from multiple angles, considering both domestic dynamics and global competitive positioning. When assessing a business, we put ourselves in the founder’s shoes: Would we run the business in the same way? Is this company prepared for the radical disruption that may come as India integrates deeper into global supply chains? Our cross-border expertise allows us to benchmark Indian companies against global peers and identify which are genuinely world-class versus those riding domestic tailwinds.

That is the edge we bring to the table, and it is why we believe we are well-positioned to continue delivering for our investors as India’s transformation accelerates.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objectives and risk tolerance levels. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

MSCI India Index is designed to measure the performance of the large and mid-cap segments of the Indian market. The index covers approximately 85% of the Indian equity universe. MSCI Emerging Markets Index captures large and mid-cap representation across 24 Emerging Markets (EM) countries. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

The contents of this material are prepared and maintained by Shikhara and have not been reviewed by the Securities and Exchange Commission of the United States.

The Fund managed by Shikhara may or may not hold all of or some of the securities mentioned in the article.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, and the European Union and pending registration in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.