India’s policy pivot is now unmistakable. November saw the most comprehensive labor reforms in decades, consolidating 29 laws into four codes and bringing 250 million unorganized workers into the formal economy. Combined with the RBI’s December rate cut, conditions are aligning for a cyclical recovery backed by structural reform. While market participants fret over rupee weakness and foreign outflows, we see these as lagging indicators. Foreign positioning is the lightest in history and valuations have reset, setting the stage for what we believe will be a constructive year in 2026.

Indian equities edged up 0.89% (in USD terms1) in November, extending their recovery for the third consecutive month. By sector, IT and Energy were the top performers, while Utilities and Real Estate were the laggards. Foreign portfolio investors (FPIs) remained net sellers for the month, withdrawing approximately USD 425 million from Indian equities in November.2 However, the headline figure masks a notable divergence: FPIs continued to favor IPOs, channeling ~USD 1.3 billion into the primary market, while pulling ~USD 1.8 billion from secondary markets.3

The highlight of the month was the release of India’s Q2 FY26 (July- September) GDP data, which came in at a stronger-than-expected 8.2% y/y, recording the fastest pace in six quarters and well above the Reserve Bank of India’s (RBI) projection of 7%. Growth was driven by strong manufacturing output (9.1%) and services (9.2%), while private final consumption expenditure (PFCE) grew 7.9%, supported by income tax cuts and robust rural demand.

India’s manufacturing purchasing managers’ index (PMI) eased to 56.6 in November from 59.2 in October, marking the slowest improvement in factory activity in nine months.4 The deceleration was attributed to softer new order inflows and the impact of US tariffs on export orders, which grew at their slowest pace in over a year. However, the reading remained well above the long-run average of 54.2, indicating continued expansion. On the other hand, services PMI rose to 59.8 in November (vs 58.9 in October), signaling a historically sharp expansion driven by robust new business intakes, with the sector now in expansion territory for 52 consecutive months.5

India’s consumer price index (CPI) inflation fell to 0.25% y/y in October, the lowest on record and well below the RBI’s 4% target. Food prices, which account for nearly half of the consumer basket, declined by 5.0% annually, reflecting improved harvest conditions and the full-month impact of GST rate cuts implemented in September.

US-India trade negotiations showed ongoing momentum in November, with senior US officials describing positive developments and suggesting a deal could be reached before year-end. India announced a landmark LPG import agreement as part of efforts to diversify energy sourcing and reduce the bilateral trade surplus with Washington. While key sticking points remain around agricultural imports and tariff structures, both sides have signaled flexibility.

While investors were preoccupied with market volatility and the AI-driven pullback in November, Indian equities were quietly reaching all-time highs. The RBI’s widely anticipated rate cut materialized in early December, with the central bank reducing interest rates by 25 basis points to stimulate economic growth. Markets had priced in this move throughout November, fueling optimism in rate-sensitive sectors such as financials, real estate, and automobiles.

This monetary easing coincided with India’s recent transformational labor reforms implemented on November 21st – the most comprehensive overhaul of labor governance in decades. Just as the introduction of GST unified India’s fragmented indirect tax system for businesses, these labor reforms do the same for the country’s unorganized workforce. The new regime consolidates 29 fragmented laws into four unified codes, creating the operational predictability and digital compliance systems that global investors have long demanded.

Critically, the reforms expand coverage from 80 million organized workers to approximately 330 million, bringing an estimated 250 million unorganized workers into the formal economy.6 This formalization could generate an additional INR 4 trillion in social security contributions, translating to roughly USD 5 billion in annual passive equity inflows.7 Additionally, the reforms significantly strengthen India’s “China+1” positioning by extending social security to gig workers, improving workplace standards, and aligning labor governance with international ESG norms.

The reform’s success depends on consistent state-level execution, but early indicators point toward meaningful productivity gains as administrative burdens decrease and worker retention improves. Most critically, formalizing India’s 450 million-strong labor force should unlock sustained consumption growth. Higher disposable incomes and lower borrowing costs for these consumers will also enable a new set of cohorts for consumer companies to recruit in the future. We think this structural upgrade positions India to sustain growth beyond the current cycle through enhanced manufacturing competitiveness and deeper economic formalization.

Global policy stimulus broadening – A new era of state-led innovation

It’s not just India that on a policy overdrive. Governments globally are turning highly proactive, reigniting business confidence through industrial policy and AI-driven productivity agendas.

The US administration recently launched the Genesis Mission, described as “comparable in urgency and ambition to the Manhattan Project,” mobilizing the Department of Energy’s 17 National Laboratories to build integrated AI platforms accelerating breakthroughs in biotechnology, nuclear fusion, quantum computing, semiconductors, and space exploration.8 Japan is pursuing a parallel strategy, designating six strategic technology fields for prioritized research funding while advancing its fusion energy timeline from 2050 to the 2030s. The US-Japan Technology Prosperity Deal signed in October 2025 deepens collaboration across these critical technologies.

Meanwhile, China’s state-led innovation drive is already yielding visible results. The country granted over 1 million new patents in 2024, over 3 times more than the US and underscoring how rapidly the global innovation balance is shifting.9

This reminds us of the Sputnik era, when superpower competition led to unprecedented innovation. That period spawned the invention of the internet (ARPANET), GPS, integrated circuits and advanced computing, satellite communications, and more. When great powers compete technologically with strategic funding, innovations extend far beyond military purposes to profound commercial and consumer applications.

Given this global context, India’s policy overdrive mode becomes imperative to maintain economic momentum. We believe meaningful progress is being made across multiple fronts, and current trade tensions will eventually be resolved through diplomatic channels. Once tariff uncertainties are settled, foreign investors should return to Indian equity markets with renewed confidence, providing support for Rupee strengthening. For now, it makes strategic sense for India to focus on domestic policy measures (e.g. labor reforms, fiscal stimulus, and infrastructure investment) that build long-term competitiveness regardless of external headwinds. As India’s structural reform story gains clarity and differentiates itself from regional peers next year, we expect to see significantly improved capital flows as global investors recognize the country’s unique combination of demographic dividends, policy momentum, and manufacturing potential in an increasingly multipolar innovation landscape.

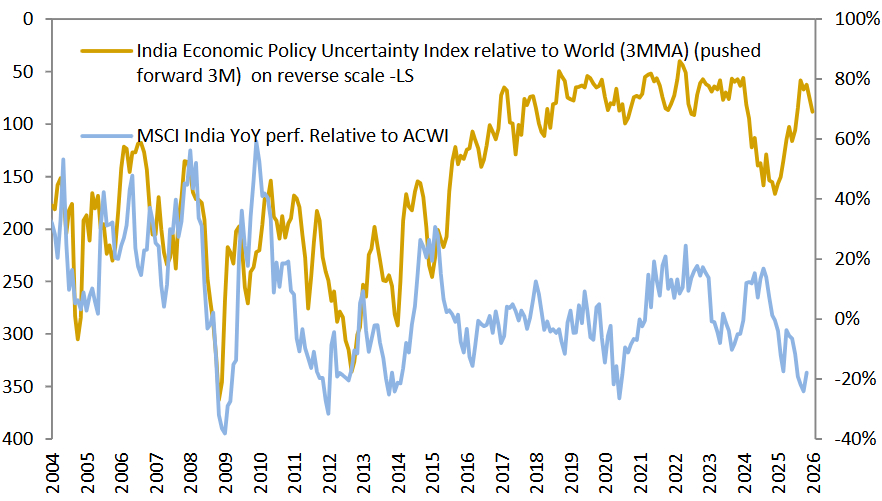

Our recent interactions with market participants in India revealed a degree of anxiety – concerns about the Rupee potentially weakening toward 90, particularly as it has slipped while most Asian currencies appreciated against the dollar over the past 9-12 months. Investors are watching FPI outflow figures and questioning why foreigners continue to sell.

We take a different view. As we have always done, we look past headline flows to the underlying health and fundamentals of the economy. The question we ask is simple: are conditions at the macro and micro level improving or deteriorating?

On the macro side, the government is advancing labor reforms, working toward GST rationalization, and pursuing privatization of state utilities on the distribution side – all structural positives. Importantly, India does not carry the heavy subsidy burdens that weigh on many developed economies today, giving policymakers greater fiscal flexibility.

On the micro side, we are encouraged by the competitive intensity emerging among Indian corporates. A recent “war cry” from one of India’s most prominent banking industrialists, urging companies to adopt a paranoid mindset to survive in this era, reflects a healthy self-awareness. We have seen some of India’s largest industrial conglomerates actively discussing disruption and adaptation. It would be welcome to see this same urgency from large established technology companies and legacy financials. We are less concerned about newer fintech and digital platforms – these companies have grown the hard way over the past five years, making them sharp, nimble, and quick to adapt. Many of these names will become increasingly prominent in benchmark indices over time.

Foreigners are selling India because it has been one of the top-performing markets globally. But outperformance does not preclude future returns – India’s growth dynamics remain sound, and we believe the market can continue to deliver over the next 5-7 years. The challenge it must navigate is the AI-led job disruption that lies ahead, but this is a challenge facing most economies. India’s young, adaptable workforce and entrepreneurial culture position it relatively well for this transition.

For these reasons, we have turned more constructive on India from October onwards, modestly increasing net equity exposure as valuations became more attractive following the correction. We continue to like domestic consumption and financial deepening plays, including leading private banks, differentiated lenders, and tech-forward platforms in e-commerce, travel, and food delivery. We also favor manufacturing and industrial leaders, spanning infrastructure, power transmission, and auto components with export optionality. Healthcare offers a defensive ballast through hospitals and domestic pharma. Meanwhile, our short book remains focused on richly valued consumer staples and large-cap IT services with limited near-term catalysts.

Our positioning reflects conviction in India’s underlying fundamentals and the firm policy pivot now underway. Following this year’s pullback, we believe Indian equities will regain momentum in 2026. Foreign investor positioning remains the lightest in history, relative valuations are consistent with improved forward performance, and the structural domestic bid remains intact. As the tariff overhand clears and India’s reform story gains clarity, we expect capital flows to return to Indian equity markets.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. Whereas Shikhara has, to the best of its endeavor, ensured that such, information is accurate, complete and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this material are prepared and maintained by Shikhara and has not been reviewed by the Securities and Exchange Commission of the United States.

The Fund managed by Shikhara may or may not hold all of, or some of the securities mentioned in the article.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom and the European Union and pending registration in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.