Indian equities finally began to reflect the activity we’ve been seeing – broader earnings beats, improving trade optics, and liquidity that is finding productive channels. We lean into this with measured confidence: AI is a real risk to white‑collar roles, but the growth mix from the gig economy, tourism, and new businesses offers ballast and time to adapt. Our positioning stays selective, focusing on quality franchises with strong right-to-win, while fading areas where moats are eroding. This month, we also feature notes from our analysts on the ground and share their takeaways from recent channel checks. Overall, while we are mindful of near‑term noise, India continues to be a “buy” for us, and a “buy-on-dips” whenever possible.

Indian equities returned 4.41% (in USD terms1) in October, extending their rebound from September despite heightened volatility. Strong Q2FY26 earnings and optimism around domestic demand recovery drove performance. By sector, Real Estate and Communication Services were the top performers, while Consumer Staples and Consumer Discretionary were the laggards. Foreign institutional investors turned net buyers after several months of outflows, purchasing USD 1.7 billion of Indian equities in October.2

Early festive season data showed record spending, with the Confederation of All India Traders (CAIT) reporting +41% growth to INR 6 trillion, with 87% on Indian-made goods, and consumer durables like TVs surging 20%.3 This led to a boost in sentiment in discretionary and retail banking names.

India’s manufacturing purchasing managers’ index (PMI) rose 1.5 points to 59.2 in October, mainly due to strong domestic demand and the goods and services tax (GST) relief measures, which boosted new orders and factory activity. On the other hand, services PMI eased slightly to 58.9 in October (vs 60.9 in September), showing slower expansion due to competition and heavy rains, but it still indicated strong growth above the long-run average.

India’s consumer price index (CPI) inflation eased to1.54% y/y in September, signaling a sharp slowdown from August and marking one of the lowest readings in years. Core-CPI (items excluding food and fuel) remained subdued at 4.2% y/y in September, reflecting tame underlying price pressures despite some volatility in food items.

The market was also supported by easing US trade tensions, following earlier tariff shocks. October trade talks showed incremental progress between the US and India, with discussions signaling potential phased concessions but no final agreement. Positive signals included moves on market access and energy trade, while sensitivity remained in agriculture and dairy, keeping a comprehensive deal contingent on further negotiations.

Last month, we wrote that confidence was rising on the ground in India, and October data reinforced that trend.

Earnings breadth is improving while GST tailwinds are coming through. Q2FY26 earnings were broadly positive, led by Financials and Telecom. Consumer names saw a brief distortion from GST rate cuts (with some demand deferred), but normalization is underway. The benefits of GST rationalization have been most visible in autos – industry estimates point to ~470,000 cars, sedans, and SUVs sold in October, up 17% y/y and surpassing the prior record of ~405,000 units set in January 2025.4 The demand backdrop remains healthy, with momentum broadening across categories.

Trade discussions are moving in the right direction. On the trade front, India was always a bit stuck between the US and Russia, particularly over discounted energy imports and defense procurements. The US’s August 50% tariff on Indian exports included an explicit “penalty” for undermining sanctions, exacerbating this bind. However, the US’s latest sanctions on Russia’s largest oil firms have inadvertently provided India with a diplomatic cover to recalibrate: major refiners like Reliance are signaling reduced Russian purchases amid compliance risks and narrower discounts. This dovetails with bilateral talks, as India diversifies toward US and Middle Eastern crude as a practical concession. We see a viable path forward for the 50% tariffs to unwind, and we’ll continue to watch for signs of progress in trade negotiations.

Liquidity conditions are favorable. In general, liquidity remains easy, funding costs are falling, and capital is circulating in the Indian economy. Lower borrowing rates are encouraging corporate capex, feeding directly into demand. Ample system liquidity is visible in primary markets – IPO activity and deal sizes have trended higher over the past decade, with deepening domestic participation. Investment interest is also picking up externally from Japan and the Middle East. This broad investor base helps recycle capital back into growth projects and balance‑sheet strengthening.

Supply chain share gains. Tariff dynamics have put pressure on European suppliers, prompting end clients to reassess counterparty risk and resilience. We heard this from Indian auto component manufacturers: customers are shifting toward Indian vendors with stronger balance sheets, healthier margins, faster service, and shorter turnaround times. Boeing, for example, is ramping up work in India, focusing on manufacturing, IT services, and components for their aircraft, and aims to expand annual spending in India to USD 1.3 billion.5

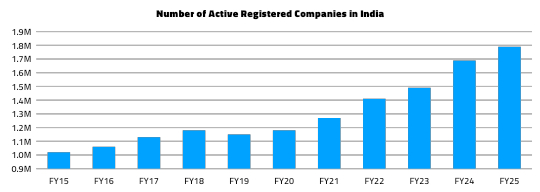

The knock‑on effects are visible in the real economy – new business registrations are rising at one of the fastest clips globally, supporting job creation and reinforcing a virtuous cycle of investment and growth.

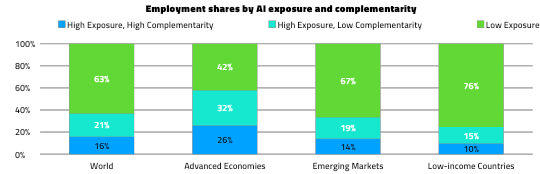

One risk that could derail India’s growth story is AI. The near-term shock from AI is likely to be felt most acutely in developed markets, where middle‑income, white‑collar roles in routine cognitive work are most exposed, potentially widening inequality and weighing on global demand.

But India is not immune. With over a billion AI users and deep exposure to services, certain white‑collar functions in IT-enabled services, customer support, and back‑office operations will face automation pressure.6 Productivity gains will offset some of this over time, but the transition will be uneven across firms and skills.

Set against that risk is a powerful offsetting engine on the ground. Job creation in India over the past 3-4 years has been anchored in the gig economy (e.g., food delivery, ride hailing, and local services) and the bigger story for the next decade is the rise of new enterprises from tier‑2/3 cities. New business registrations are growing rapidly, supported by national infrastructure build‑out, financial inclusion, GST‑led formalization, and e‑commerce as a low‑cost distribution channel. These platforms lower barriers to starting and scaling, broadening employment beyond traditional white‑collar pools and seeding AI‑complementary roles in sales, field services, compliance, and domain‑augmented IT.

Domestic tourism adds another labor‑intensive buffer. Investments in connectivity and destination development are catalyzing activity across hospitality, transport, retail, and local services. This creates meaningful employment for lower‑ and mid‑skill workers and supports artisanal and experiential demand, which are less susceptible to near‑term AI substitution. As these domestic growth drivers compound, they help set a floor under employment even as AI adoption accelerates.

Policy readiness also matters. In a way, we think that the 50% tariffs from the US are a blessing in disguise, forcing the Indian government to get its act together. As tariffs unwind, the bigger threat from AI will still remain, but Indian policymakers already have plans in motion to limit the impact and provide a buffer on jobs in the real economy. When markets begin to price in AI impacts on jobs next year, India will be 6-12 months ahead in their preparations.

Our base case is that AI will compress some service margins and slow headcount growth in routine functions, but India’s dynamic growth mix of domestic consumption, small-medium enterprises (SMEs), infrastructure, tourism, etc. will remain resilient. We expect net employment to continue expanding, with churn toward new enterprise formation and higher‑productivity roles, supporting a durable medium‑term trajectory.

Given this backdrop of firm domestic demand, improving trade dynamics, easy liquidity, and a manageable AI transition, we remain selectively pro‑cyclical – leaning into domestic demand, financials, and AI‑enabled productivity, fading areas where competitive intensity is eroding moats, and shorting areas facing structural de-rating.

Overall, we see India’s cycle as intact and skewed to the upside: domestic demand is resilient, trade frictions are easing at the margin, liquidity is supportive, and AI is more a reshaper than a spoiler. Execution, regulation, and global growth remain watch-items, but the breadth of engines across India’s dynamic economy supports a constructive risk stance into the next leg of the cycle.

Here, we capture some on‑the‑ground observations from our India team – stories and signals that serve as practical barometers for demand, sentiment, and execution.

India’s approval of a ~USD 8 billion maritime package in September 2025 marks a turning point for the country’s shipbuilding sector and broader economy. The move signals both the scale of India’s ambition and the recognition that shipbuilding, which has been long underleveraged, is central to national security and economic resilience.

At the core of the package is the Shipbuilding Financial Assistance Scheme (SBFAS), extended to 2036 with an allocation of ~USD 3 billion. This program directly subsidizes new builds and retrofits, with higher support for advanced projects (up to 25% for green/hybrid/specialized ships; 20% for large vessels; 15% for smaller builds). A new shipbreaking credit of about USD 0.5 billion incentivizes scrapping in Indian yards and recycling proceeds into new construction, promoting circularity and sustainability.

A second pillar focuses on financing and capacity building through the Maritime Development Fund (MDF) and the Shipbuilding Development Scheme (SbDS). Together, these form the complementary funding of roughly ~USD 5 billion. Within this, the MDF includes a Maritime Investment Fund of USD 2 billion and an Interest Incentivization Fund of USD 1 billion, while the SbDS carries around USD 2 billion to expand yards, coastal clusters, repair facilities, and provide risk coverage.

Perhaps the most consequential policy change is granting “infrastructure status” to shipbuilding. This reclassification puts shipyards on par with highways and power projects for long-term credit, tax, and regulatory benefits, addressing a chronic barrier to cheap, long-term financing and improving the sector’s bankability.

Collectively, these measures are expected to unlock up to USD 51 billion in broader investment and create as many as 3 million jobs, with spillovers to steel, components, logistics, and ports. Annual shipbuilding capacity is targeted to rise to 4.5 million gross tons, signaling an ambition to scale from a marginal position today to a significant manufacturing hub within two decades.

In the global context, India accounts for under 1% of world shipbuilding output while China, South Korea, and Japan dominate over 90% of new builds. As the US and the rest of the world diversify from China, South Korea has been a key beneficiary in shipbuilding, but India could rise to take share. The package and infra status provide a necessary financial and policy foundation, but moving into the global top tier will also require productivity gains, large-scale skilling, deeper supply-chain integration, technology partnerships, and consistent R&D investment.

While India’s top 10 cities continue to dominate overall consumption, a growing share of incremental growth is now coming from smaller towns. The purchasing power and aspirations of consumers in Tier-2 and Tier-3 cities are often underestimated, yet recent trends demonstrate their rising influence. Companies with strong distribution networks or platforms that resonate with these markets are the ones gaining the most.

Key examples of this shift include:

In summary, India’s next wave of consumption growth is being powered by smaller cities. Companies that can penetrate these markets, through stronger distribution, localized offerings, and data-driven expansion, are best positioned to capture the opportunity.

Value fashion continues to outpace premium/branded apparel, aided by a relatively stronger rural backdrop versus metros and visible down-trading as consumers manage tighter budgets. The segment is also benefiting from the shift from unorganized to organized formats and aggressive store rollouts. In 1QFY26, the four listed value retailers posted 24% revenue growth, supported by an 18% increase in retail area and mid-single-digit normalized same-store-sales-growth (SSSG).

Our channel checks to a Vishal Megamart in Dehradun (a large 30,000 sq ft, four‑floor store spanning apparel, footwear, home essentials, and grocery) reinforced the value thesis. The proposition is unambiguous – “Pay Less Always”, with apparel priced below Zudio (shirts at roughly USD 3–7); while quality and design trail Zudio, they exceed other value peers like V‑Mart, and a broader SKU breadth than Zudio’s curated assortment suits small‑town, low‑ticket priorities. Private label penetration is 100% in apparel and extends into food staples and snacks (instant noodles, tea, oats, cereals, biscuits), where sharper promotions are driving traction. Weekend sales average about INR 1.2 million per day (vs roughly INR 0.6 million on weekdays), and inventory turns are aided by replenishment every other day.

This is a segment we’ll continue to monitor in terms of store economics, private-label traction, and share gains versus curated/value peers to gauge the segment’s durability and pace of expansion.

In summary, India’s next wave of consumption growth is being powered by smaller cities. Companies that can penetrate these markets, through stronger distribution, localized offerings, and data-driven expansion, are best positioned to capture the opportunity.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. Whereas Shikhara has, to the best of its endeavor, ensured that such, information is accurate, complete and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this material are prepared and maintained by Shikhara and has not been reviewed by the Securities and Exchange Commission of the United States.

The Fund managed by Shikhara may or may not hold all of, or some of the securities mentioned in the article.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom and the European Union and pending registration in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.