October’s market narrative is one of divergence. While developed markets grappled with private credit wobbles, rising sovereign yields, and deepening political fragmentation, the Asia region emerged as a beacon of stability and opportunity. This month, we explore how dollar weakness and abundant liquidity are redirecting capital flows, examine where we stand in the AI infrastructure cycle, and share ground-level insights from our analyst’s recent trip to China. As the developed-emerging market narrative evolves, the investment implications are becoming impossible to ignore.

The MSCI All Country Asia Ex-Japan Index gained 4.50% (in USD terms1) over the month of October. Relative to the rest of the region, South Korea and Taiwan were the top performers, while China and Singapore were the laggards. Sector-wise, IT and Industrials led performance, while Communication Services and Consumer Discretionary were the worst performers.

MSCI China declined 3.80% in October, consolidating after five consecutive months of gains. Escalating US-China tensions (e.g., rare earth curbs, proposed sanctions on Chinese tech, and new port fees on Chinese vessels) drove risk-off sentiment until the Trump-Xi meeting on October 30 saw the two sides reach an agreement. The release of the 15th Five-Year Plan reaffirmed Beijing’s focus on advanced manufacturing, AI infrastructure, and green transition, though market response was muted. China’s GDP grew 4.8% y/y in Q3, meeting expectations but underscoring moderating momentum amid weak domestic demand. Meanwhile, despite persistent deflation, industrial profits surged 13% y/y in Q3, driven by a low base and strong exports in high-tech sectors.

Indian equities returned 4.41% in October, extending their rebound from September despite heightened volatility. Strong Q2FY26 earnings and optimism around domestic demand recovery drove performance. Early festive season data showed record spending, with the Confederation of All India Traders (CAIT) reporting +41% growth to INR 6 trillion, with 87% on Indian-made goods, and consumer durables like TVs surging 20%. This led to a boost in sentiment in discretionary and retail banking names. The market was also supported by easing US trade tensions and optimism around a potential trade deal.

Korean equities surged 22.65% in October, as the KOSPI broke above 4,000 to a record 4,107.50, driven by AI/semiconductor momentum and US-Korea trade deal progress. Semiconductor names led on HBM and memory supercycle optimism, with SK Hynix up +58% (best month since 2005) and Samsung up 26.1%, though the two companies saw divergent foreign flows (foreigners sold SK Hynix but bought Samsung). Korean electric vehicle (EV) battery names and shipbuilders also rallied on constructive 3Q25 earnings and optimism around cooperation with the US.

Taiwanese equities rallied 9.84% in October, with the TAIEX extending a six-month winning streak to record a high of 28,527, led by AI and semiconductor momentum. TSMC powered gains with strong earnings beats and full-year guidance upgrades, while legacy memory names also surged on the DRAM/NAND cycle recovery. Meanwhile, power supply stocks also rallied on Nvidia’s 800VDC push for gigawatt AI factories.

ASEAN equities posted modest gains in October amid mixed flows, with Thailand (+4.68%) and Indonesia (+4.06%) leading on resilient tourism and foreign inflows, while Singapore (-0.40%) lagged on bank profit-taking. Indonesian banks outperformed on robust 3Q25 results and expectations for stronger 4Q25 earnings, supported by higher NIM and fee income. Meanwhile, in Singapore, Sea Limited was a drag on the market due to profit-taking following expectations of softer gaming and e-commerce momentum.

Developed market jitters are creeping in

October exposed cracks in developed markets (DMs), yet the global recovery remains intact. Excesses in US private credit were highlighted by the collapses of Tricolor Holdings and First Brands, which sparked a pullback in bank stocks and heightened volatility. While we don’t see this as a systemic threat, it is a reminder of the fragilities in certain DMs.

The greater concern lies in sovereign debt dynamics. Rising bond yields in France, the UK, Japan, and the US signal mounting stress. Policymakers will likely act to contain yields through fiscal restraint, selective spending cuts, and what amounts to financial repression, encouraging domestic institutions to absorb sovereign paper. Over time, this could redirect capital toward emerging markets (EMs) with stronger balance sheets and more disciplined policy frameworks.

The US backdrop has also become more unsettled. The record government shutdown, deteriorating sentiment, and an unprecedented wave of layoffs (150,000 alone in October) underscore that the “Magnificent 7” rally sits atop a fragile base.2 The University of Michigan’s sentiment index dropped to 50.3 for November, near multi-decade lows, reflecting widespread fatigue with inflation, unemployment, and political gridlock.

Political fragmentation in the US is becoming more entrenched. Mamdani’s recent win in New York highlights the widening divide between liberal urban centers and conservative heartlands, a reflection of the ideological rift now defining much of the developed world. This polarization constrains policy coherence and undermines investor confidence in long-term fiscal planning.

Emerging markets poised to benefit

In contrast, EMs, particularly in Asia, benefit from comparatively stable governance, prudent fiscal frameworks, and clearer policy direction. As DMs contend with internal political gridlock, emerging economies appear more cohesive and better positioned to attract capital seeking stability and consistency.

Dollar weakness is adding another tailwind for EM assets, and China’s recent dollar bond issue at the same yield as US Treasuries marks a symbolic shift: that the US is no longer the sole benchmark for risk-free pricing. Global liquidity remains abundant, yield differentials have collapsed, and sovereign buyers are looking for alternatives to diversify away from dollar assets for optionality and hedging.

For Asia, rising capital inflows translate directly into investment, job creation, and productivity gains. India provides a clear example. Over the past decade, the government has laid the groundwork for durable productivity growth through infrastructure build-out, digitalization, and financial inclusion. Flagship programs such as Make in India, the Digital India initiative, PM Gati Shakti infrastructure plan, and the expansion of the Unified Payments Interface (UPI) have collectively enhanced logistics efficiency, reduced transaction costs, and broadened access to credit. The formalization of the economy has improved tax collection and funding availability, creating a virtuous cycle of reinvestment and rising household consumption. A similar productivity flywheel is set to play out across the region as capital, technology, and policy catalyze durable efficiency gains.

Across North Asia, automation and industrial upgrading are the drivers. China and Korea are at the forefront of robotics, semiconductor capacity, and green manufacturing technologies. China’s latest plenum reaffirmed a shift toward quality growth, emphasizing technology self-sufficiency and more efficient capital allocation. The country is deliberately curtailing traditional infrastructure and property investment in favor of productivity-led growth. This is what we wrote back in March – that the world needs to invest while China needs to cut back on investments to correct the decades-long imbalance. That is now happening.

Elsewhere in Asia, Southeast Asia, Vietnam stands out: with strong skills, healthy balance sheets, and deep customer support and servicing, Vietnamese firms are winning share from developed-market suppliers across various manufacturing segments. As global customers diversify, they need partners that are equally competitive, and Vietnam is meeting that bar. These shifts reinforce Asia’s position at the center of global supply chains and as a supplier of key inputs for automation and energy transition worldwide.

In this context, Asia is an incredibly exciting landscape for bottom-up stock selection, but we are concentrating on the most resilient businesses that can be the last man standing through cycles. The market is not without its risks, and we are monitoring these risks (e.g., rates, tariffs, supply chains, etc.) in the companies we own, adjusting exposure as signals change. Near term, rate cuts will remain a positive for markets, while the trade deal cadence is better seen as an evolving annual negotiation rather than a one-off event, reinforcing the need for durable franchises that can compound through policy noise.

There is plenty of talk about an “AI bubble.” Our view is more nuanced. Transformative technology waves require vast, upfront infrastructure before adoption scales. Not all of that buildout will earn compelling returns, yet many technology firms must invest existentially to stay relevant. That imperative creates opportunity – for the adopters who convert AI into productivity and revenue, and for the platforms whose core businesses become more valuable as AI usage deepens.

A sharp pullback wouldn’t surprise us, but we are still early in the buildout. AI data center capex spans a wide range, anywhere between USD 7–50 billion per GW. At the upper end, standalone projects not anchored by hyperscalers or a robust end-market may struggle to earn acceptable returns. By contrast, the bulk of spend by hyperscalers is supported by durable, existing business models. Even if the data center return on investment (ROI) looks modest in isolation, AI can enhance the economics of their core franchises (e.g., through hyper-personalized consumer experiences, better ad targeting, higher developer engagement, and improved retention). As use cases mature and value delivery becomes visible, we expect more of the economics to accrue back to these platforms. Returns may dilute at the project level, but they need not undermine the investment case.

The risk sits with high‑capex builders lacking scale, ecosystem pull, or customer monetization, especially outside the mega‑cap tech cohort. Standalone AI/data center efforts without clear revenue flywheels could face tougher capital cycles. That’s why we’re seeing aggressive user-acquisition tactics from large language model (LLM) platforms to seed habits and accelerate network effects.

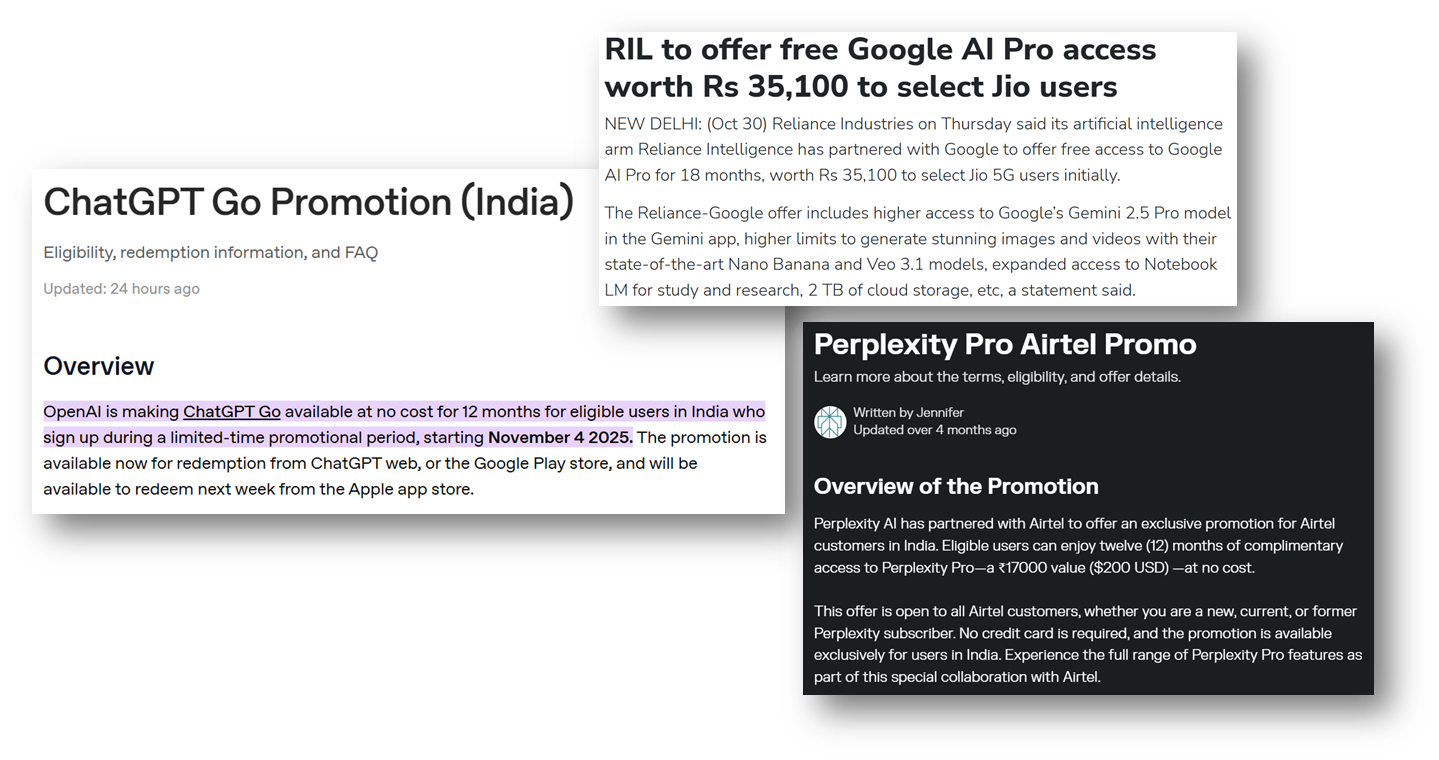

In India, offers from OpenAI for ChatGPT Go, Perplexity via Airtel promos, and Google Gemini bundled for Jio users echo the early ride-hailing playbook, when Uber and Lyft subsidized usage to drive adoption. We also saw this in early streaming platforms, where free trials, aggressive intro pricing, and telecom/device bundles were offered to seed habits and scale before pivoting to tighter monetization. A similar playbook is happening with AI. As mass adoption sets in, monetization typically follows. Casual users may remain on free tiers, but power users and businesses deriving tangible productivity gains will tend to convert to paid plans, creating the revenue engine these platforms need.

As we’d published in our recent white paper on the AI value chain, we view the AI investment landscape as an infrastructure-led transformation where value accrues at two ends of the chain: 1) to scarce, mission-critical enablers and 2) to adopters that convert AI into tangible productivity and revenue. It’s a multi-year build marked by surging hyperscaler capex, rapid accelerator roadmaps, and a supply chain in which Asia holds a disproportionate share of leading-edge foundry, advanced packaging, HBM memory, and rack integration.

On the enabler side, that means leading-edge foundry and CoWoS capacity at TSMC, HBM memory leaders in Korea, and select Taiwan rack/server OEMs with hyperscaler design wins – segments tied directly to the AI capex wave and protected by scale, technology moats, and supply discipline. On the adopter side, we prioritize platforms already monetizing AI through better engagement and efficiency. For example, Chinese internet leaders (e.g., Alibaba, Tencent) and SEA champions the use of AI to lift conversion, ad yield, and unit economics, as well as targeted IT services partners where enterprise integration spend is building. This barbell of critical enablers and high-ROI adopters positions us to capture the multi-year opportunity as capex broadens from training to inference and custom ASICs, while remaining selective to avoid duplicating the same underlying driver and to navigate any mid-cycle pause.

Our Senior Investment Analyst, Marcus Chu, met with corporates and domain experts across China in October. Here are some of his key takeaways from the trip:

Overall, we remain constructive on markets and would be buyers of pullbacks. A near-term correction could persist for a couple of weeks, given the prolonged standoff between Republicans and Democrats on the government shutdown, and a natural inclination to lock in gains after a strong 2025. But our medium-term thesis is intact: EM balance sheets are healthier, Asia’s productivity flywheel will continue to gain momentum, and AI-driven capex and adoption are broadening.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return, and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Private Placement Memorandum for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The MSCI AC Asia ex Japan Index captures large and mid-cap representation across Developed Markets (DM) countries (excluding Japan) and Emerging Markets (EM) countries in Asia. The index covers approximately 85% of the free float-adjusted market capitalization in each country. The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips, and foreign listings (e.g. ADRs). The index covers about 85% of the Chinese equity universe.

The contents of this material are prepared and maintained by Shikhara and have not been reviewed by the Securities and Exchange Commission of the United States.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom and the European Union and pending registration in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.