August highlighted both challenges and opportunities for India. US tariffs and global headwinds tested export competitiveness, yet domestic demand and consumption held firm. Policymakers are seizing this moment to advance reforms, setting the foundation for stronger growth. For investors, we think the recent pullback is not a warning but a strategic entry point into structurally robust sectors, including AI-enabled consumer platforms and industrials powering India’s domestic-led recovery. Amid persistent global uncertainty, India’s fiscal discipline, new reform momentum, and capacity for innovation make it a market positioned to emerge stronger and more competitive in the long run.

MSCI India fell 2.21% (in USD terms1) over August, pulling back for a second consecutive month amid heightened US tariff pressures and persistent foreign investor selling. Foreign portfolio investors (FPIs) net sold USD 4.0 billion of Indian equities in August, though this was more than offset by domestic institutional investor buying.2 Consumer Discretionary and Consumer Staples were the only positive-returning sectors, while Financials and Real Estate were the worst-performing sectors.

On August 27, 2025, the US imposed an additional 25% tariff on Indian exports, bringing the total to 50%, citing India’s Russian oil imports and trade surplus. The escalation heightened concerns over India’s export competitiveness and amplified volatility in globally exposed sectors such as IT and Industrials. This came on top of softer balances, with July’s goods trade deficit widening to USD 27.4 billion (vs USD 18.8 billion in June), the highest in eight months, as imports outpaced exports.3 Meanwhile, the net services balance narrowed to an eight-month low of 4.6% of GDP on a monthly annualized basis in July (vs 4.9% of GDP in the previous month.4

Domestic demand indicators remained robust. Goods and Services Tax (GST) collections rose 6.5% y/y to INR 1.81 trillion (USD 20.5 billion) in August, though was slightly down from INR 1.96 trillion (USD 22.4 billion) in July.5 The Unified Payments Interface (UPI) set a record 20 billion transactions in August (worth INR 24.9 trillion in value), underscoring healthy consumption and digitization trends.6

Other leading indicators also remained resilient. Manufacturing purchasing managers’ index (PMI) rose to 59.3 (vs 59.1 in July), its highest level in nearly 18 years.7 While international demand growth softened slightly due to tariff uncertainties, overall order inflows held up well, supported by a surge in domestic demand. Services PMI also surged, increasing by 2.0 points to 62.5, marking the strongest expansion in the services sector since June 2010.8

Headline consumer price index (CPI) inflation eased to 1.55% y/y in July, down from 2.10% in June, marking the lowest rate since January 2019. The slowdown was led by a contraction in food prices, though both core (4.2%) and core-core (3.0%) measures of inflation also moderated from the prior month.

By now, market participants are becoming used to the news cycle. There continues to be no shortage of headlines over the past month, yet investors are starting to accept that the only thing certain is uncertainty. Through all the noise, global markets continue to climb, and like the Roaring 20s, the market is overshooting expectations.

While everyone is focused on the issue of tariffs, the negative impact of tariffs is being mitigated by operating leverage and lower headcount, particularly in white-collar jobs where AI is suppressing entry-level hiring. With the existing workforce, it seems like another company is announcing layoffs every other day. So why isn’t this impacting the numbers?

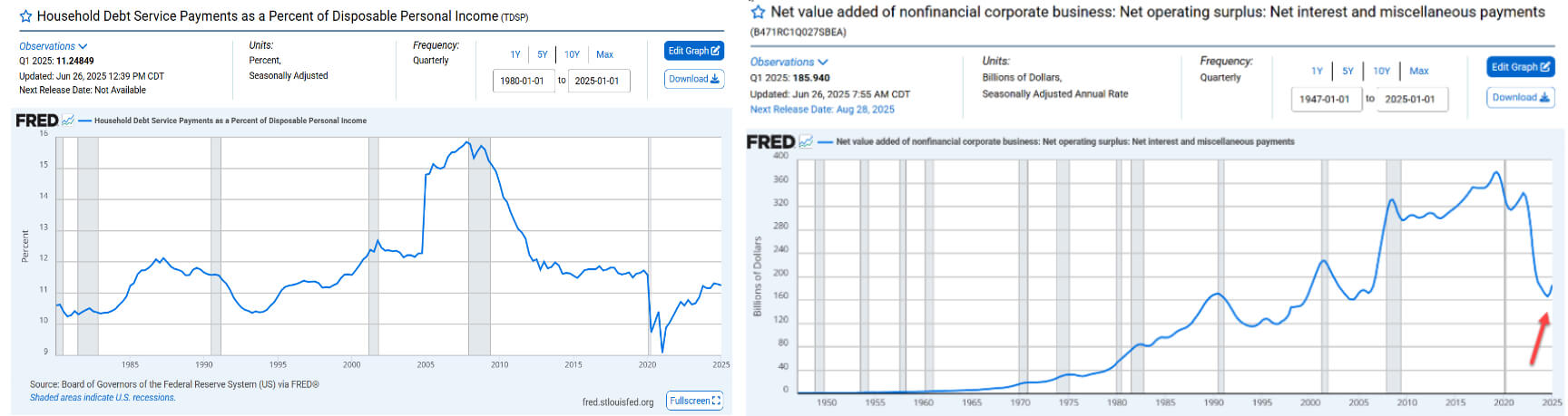

Firstly, consumers still have resilient balance sheets and can absorb near-term impacts. Household balance sheets are the strongest they’ve been in decades, and the same goes for corporates. Interest expense for non-financial corporations has climbed but remain at 20-year lows. In short, there is no balance sheet stress.

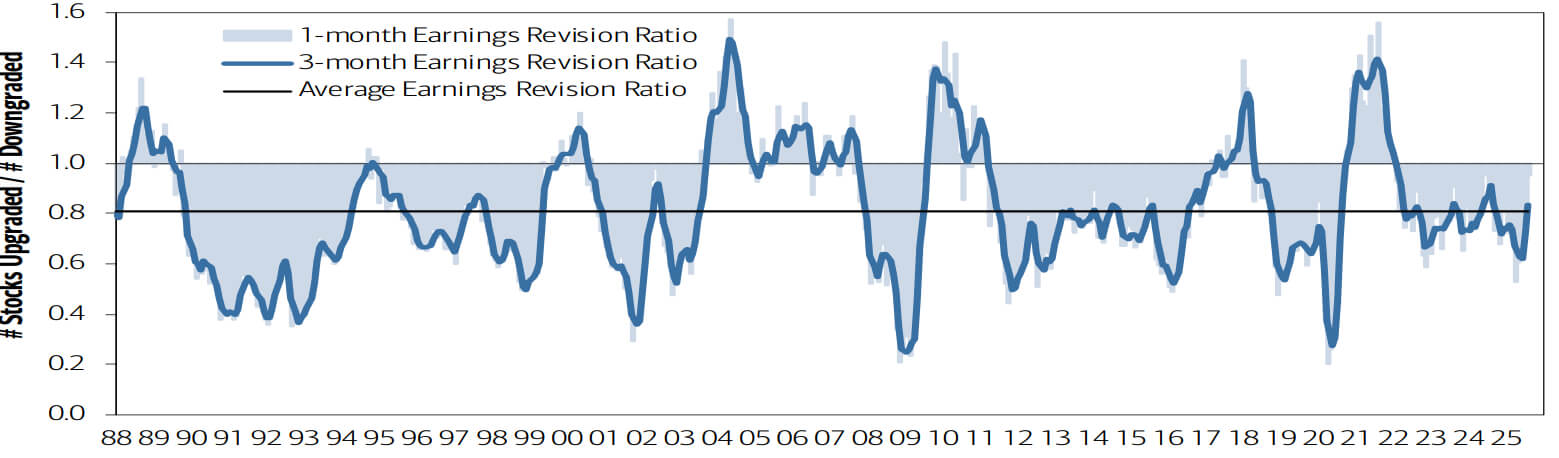

Secondly, corporations will first reap the productivity benefits and can absorb near-term tariff impacts through better operating leverage and AI adoption. The benefits of deregulation are still to come and will also help with productivity gains. We see this through recent earnings upgrades, such as with Amazon and Walmart. BofA’s Global Earnings Revision Ratio (a breadth measure of how consensus earnings expectations are trending) also jumped significantly in August from 0.81 to 0.95 and is approaching a four-year high.9 Historically, when the ratio was near current levels and rising, global equities averaged 10.8% over the subsequent 12 months.10 The ratio is near multi-year highs for the US and China, and has also improved in Europe. All this is happening in the absence of Fed interest rate cuts, which are still on the cards for the coming quarters.

That said, risks are uneven. Small/medium-sized businesses and low-wage workers will feel wage and employment frictions first, and inflation pass-through could amplify those effects. Trade policy remains a wildcard, though rhetoric is moderating and negotiations are mixed (e.g. as in the case of India – more on that below), which likely limits further tariff escalation but does not eliminate trade-related uncertainty. In short: stay disciplined, favor companies with durable cash flows and scalable productivity gains, and don’t be bearish too early.

In a typical emerging market (EM) recovery cycle, North Asian economies lead the initial phase on the back of export growth and liquidity, while capital eventually rotates into more domestically driven stories like India. That cycle is playing out again. South Korea, China, and Taiwan have powered Asia’s rally year-to-date (YTD), but as valuations there stretch into next year, India’s relative attractiveness will strengthen.

A softer US dollar can be constructive for global growth as capital moves out of the US and into other economies. That dollar relief eases external financing costs for emerging markets (EMs), lowering FX‑adjusted debt burdens and making dollar‑denominated liabilities easier to service, which accelerates balance‑sheet repair. As corporates and households rebuild buffers and confidence improves, the natural follow‑on is stronger domestic demand and investment. This is the classic EM recovery cycle.

As we wrote back in March, the global economic realignment is increasingly being defined by nation states. With more countries adopting elements of state capitalism, valuation differentials are likely to narrow. The US is moving in the direction of this model. Recent examples include the US government’s 9.9% passive equity stake in Intel, announced in August, and the Department of Defense’s multibillion‑dollar public‑private partnership with MP Materials, the operator of the only rare earth mine in the US, announced in July. If the US is using direct capital and strategic partnerships to secure supply chains and steer industrial policy, it is harder to justify why countries such as China should trade at a persistent discount.

Thus, in a world of state capitalism and growing macroeconomic vulnerabilities in many developed economies, the valuation gap between competitive companies in developed and emerging markets should compress. EM firms are increasingly likely to be re-rated higher – a trend already visible YTD, led by North Asian peers such as South Korea, China/HK, and Taiwan, which have driven much of Asia’s rally.

So, what about India? There remains some near-term time correction in India, but we don’t expect to see a significant price correction. What time correction does is that it provides a pause for households to repair their balance sheets and set the stage for the next leg of growth. Policy moves have also been supportive, e.g. the GST rate rationalization improves affordability and demand for the middle class.

In the regional context, as the valuation gap with North Asian peers narrows in the coming quarters, the relative attractiveness will increasingly shift toward India. In the meantime, the Indian government is not letting this slowdown go to waste.

India remains a compelling long-term structural story: a large, domestic-oriented market with sovereign debt levels under control. The latter is not a given today’s world, as illustrated by the situation with France, where the sovereign debt issue has triggered discussions of a potential bailout. In an environment where sovereign balance sheets are stretched, India’s relative fiscal stability stands out.

Rather than retreat, the government is using the current slowdown and tariff headwinds to advance reforms. It is standing its ground against US demands while prioritizing domestic stimulus, such as GST cuts on hundreds of goods, and market diversification through FTAs with the EU, UK, and countries like Peru. These measures signal a clear push to revive reform momentum and restore animal spirits to kick-start growth.

For foreign investors, the pullback offers attractive entry points into a market that retains strong structural appeal.

To quote NVIDIA CEO Jensen Huang, “Greatness comes from character, and character isn’t formed out of smart people, it’s formed out of people who have suffered.” The same applies to countries. Adversity often forces economies to sharpen their competitiveness. Over the past five years, China faced trade wars, Covid disruptions, and a domestic real estate crisis. Policymakers and corporates responded by investing in innovation and new growth segments, producing global leaders such as CATL, BYD, and Xiaomi.

What looked like near-term headwinds became a medium-term opportunity when officials and firms raised their game. India may now be at a similar inflection point. While Indian markets have performed well over the past five years, the “edge” in corporate competitiveness has not fully emerged. Gains in market capitalization without much work can breed complacency – a point often noted within our investment team. We believe adversity, from tariffs, global supply chain shifts, or rising competition, can ignite the hunger and fire Indian firms need to advance. The India that emerges from this period, like China before it, is likely to be structurally stronger than ever.

With the current US administration in place, tariff cycles are likely to recur every 12–18 months, so India must focus on strengthening its competitiveness and bargaining power rather than expecting tariff relief. Practically, this means maintaining a stable defense relationship with Russia to secure critical equipment while expanding domestic capabilities, and keeping channels open with China for investment and essential machinery and components for India’s manufacturing ambitions.

While the US and Europe are focusing investment at home, China remains a major source of investment and critical machinery and equipment for India’s manufacturing ambitions. In the past year, India has eased visa rules for Chinese nationals and China has worked to improve approvals for plant and machinery equipment, reflecting a deliberate effort to strengthen ties even before the current spotlight on India-China relations. We expect this gradual warming in India-China economic engagement to continue, driven by mutual commercial needs.

We have written extensively about our macro outlook, including our 8 key market debates, the coming investment cycle, and the global investment distortion over the last two decades. What does this mean in terms of our investment focus? While it helps to know what policies are coming next, the most durable opportunities lie in companies that directly address two defining themes of the next decade: 1) rapid AI and technology advancement, and 2) rising geopolitical fragmentation in a multipolar world.

More importantly, we know that because of excessive debt for developed market sovereigns and AI-led job displacement, there’s a deflationary challenge coming. That makes it critical to prioritize companies that are disruptors within their category who can emerge as market leaders – these are the businesses that will be the last man standing.

A lot of attention has gone to the AI data infrastructure buildout and the vendors that supply it. However, the bigger value creation, which we’ve always maintained, will come through margin expansion of consumer companies. Even amid softer top-line growth that’s not fully reflective of a global recovery, operating profits are rising as companies extract efficiencies from cost rationalization and AI adoption. The question for consumer firms in a fast-moving tech era is: how do you ensure that you are the last-man-standing? The answer is hyper-personalization.

We wrote about this back in January. The winners will have three characteristics that they can leverage:

With those building blocks in place, integrating large language models (LLMs) and AI tools enables consumer-facing companies to materially improve and deepen customer engagement and experience. Some firms are already raising the bar, becoming more relevant and personalized than ever, and consumers now expect that level of tailored interaction. Of course, ethical use and robust data‑privacy safeguards are non‑negotiable. But the truth is – people respond to personalization. When firms can deliver the most relevant content, information, or product at the exact moment of need, then engagement, conversion, and loyalty rise.

Here are some of the companies in India that we think exemplify this theme:

| Companies Benefiting from the Adoption of Hyper-Personalization | |

|---|---|

| Ixigo | Ixigo, trading under Le Travenues Technology, is a leading Indian travel tech platform. Founded in 2007, Ixigo has transformed from a travel search engine into an AI-first online travel agency (OTA).

Ixigo has actually been investing heavily in AI over the past decade to boost engagement and efficiency. AI chatbots, deployed in 2017, now resolve roughly 90% of customer queries end-to-end, delivering major operating leverage.11 The company also applies AI for dynamic pricing of add-on services, intelligent trip planning via Ixigo Plan, and real-time flight monitoring with Flight Tracker Pro. These innovations have improved conversion rates and supported strong GTV growth across trains, flights and buses, while enabling deeper reach into Tier-3 and Tier-4 markets and accelerating platform stickiness and revenue growth. |

| Eternal | Eternal, rebranded from Zomato in February 2025, is a leader in AI adoption in India, particularly within food delivery and quick commerce.

In food delivery, Eternal’s Nugget platform automates over 85% of customer interactions, cutting handling time by 30% and boosting satisfaction by 25%, while AI delivers personalized food recommendations based on user preferences, mood, and dietary needs.12 By integrating image analysis, multi-modal language models, and real-time data, Eternal is reducing friction in delivery and order resolution. In quick commerce, Blinkit incorporates AI features like Recipe Rover. Powered by ChatGPT and Midjourney, the tool helps users discover recipes and instantly source ingredients via the app, creating a seamless shopping experience that boosts retention and loyalty. Blinkit also utilizes AI and machine learning (ML) for demand forecasting and location intelligence, strategically placing dark stores within a 2-3 km radius of high-demand areas in major metros, ensuring 10-minute deliveries that differentiate it in the hyperlocal market. This has allowed Blinkit to expand to over 1,500 stores by mid-2025, boosting gross order value (GOV) by 140% y/y in Q1FY26.13 These AI-driven capabilities not only enhance the user experience but also positions Eternal to capture greater market share and improve long-term profitability. |

| Nykaa | Another Indian consumer platform we’ve like for a while is Nykaa, trading as FSN E-commerce. Nykaa is a leading Indian omnichannel beauty and fashion retailer serving over 40 million monthly active users and offering 8,600+ brands.14

Since 2023, the company has been using AI-driven recommendations and Google’s Performance Max ads to tailor product suggestions and campaigns, boosting acquisitions. Nykaa leverages ML-powered recommendation engines to analyze purchase history, browsing behavior, social media activity, and skin type data. It then uses this data to suggest personalized and relevant products, boosting conversion rates and repeat purchases with its user base. |

These are great examples of B2C companies that are tech-native and have effectively adopted AI to create a durable competitive advantage. While platform companies and e-commerce are becoming more commoditized with increasing competition, those that can optimize through hyper-personalization and offer experiences with deep consumer connections will capture disproportionate market share.

In July, we published our white paper “The Industrial Revival: Asia’s Strategic Role in a Multipolar World.” That paper set out the framework: governments across the globe are embracing industrial policy, supply chains are fragmenting under geopolitical pressure, and Asia, led by South Korea, Japan, India, and China, has become the backbone of global industrial renewal. In a world where every nation is moving to safeguard its own interests, the industrial and defense companies that are able to supply critical capabilities will be the last man standing.

In India, the industrial revival is being supported by a concurrent energy transition and a significant power infrastructure upcycle. Ambitious targets for non-fossil fuel capacity by 2030 and rising capital expenditure across generation, transmission, and distribution are reversing years of underinvestment, enabling localized manufacturing, data centers, and urban electrification. The long-standing transmission and distribution bottleneck is finally gaining momentum as policymakers prioritize grid modernization to integrate renewables and meet growing baseload demand, with new technologies and large projects driving multi-year workstreams.

One company that stands out is Kalpataru Projects, a leading EPC (Engineering, Procurement, and Construction) and infrastructure contractor. We see Kalpataru as a high-conviction way to play India’s multi-year transmission and distribution boom. The National Electricity Plan’s almost INR 9.9 trillion transmission capex and the push to 500 GW of non-fossil capacity create an estimated INR 1 trillion addressable opportunity for Kalpataru over the next eight years, where it already holds a meaningful share of the inter-state transmission market.15

Near-term catalysts should reaccelerate revenue, with stronger transmission and distribution (T&D) order flow at home, a recovery in Brazil and Europe, and renewed traction in the water business, while margin leverage comes from higher utilization and operational tightening. Crucially, management’s plan to monetize non-core assets will unlock capital, boost return ratios, and de-risk the balance sheet, turning a lumpy, project-driven profile into a clearer earnings growth story. Taken together, these factors make Kalpataru a compelling way to capture durable infrastructure upside as India builds the grids that will underpin its industrial revival.

The flexible workspace industry in India has experienced rapid growth over the past decade, particularly since the COVID-19 pandemic. Several factors have contributed to this trend, including the boom in startups, a growing preference for hybrid and remote work models, and the increasing presence of Global Capability Centers (GCCs). The pandemic significantly accelerated the adoption of flexible work arrangements, demonstrating to many companies that remote work can be highly effective across a range of roles.

Today, the flexible workspace sector (including both coworking spaces and managed offices) accounts for 14% of India’s total office leasing (amounting to 89 million square feet), highlighting its rising importance in the commercial real estate sector.16 Flexible workspaces now cater not only to freelancers and startups but also attract established corporations and multinational firms (notably GCCs, which prefer managed offices). These setups offer companies fully-equipped offices with services like security, pantry, and cleaning staff, along with numerous amenities – all at negligible upfront costs and greater lease flexibility (typically 1-3 years).

The business model for flexible workspace operators is quite lucrative and is scaling rapidly, drawing significant investor interest. Operators lease office space, which they then sublease to tenants by individual seat. Currently, most operators are enjoying high occupancy rates and are targeting medium-term growth of over 20% CAGR.17 Several leading players are even preparing for IPOs to take advantage of robust investor appetite and capital requirements.

We think that the positive momentum for flexible workspaces is strong and likely to persist. However, supply is also expanding quickly, which could pose challenges. Additionally, given the limited differentiation among operators, customers tend not to be brand loyal. For these reasons, we would look for operators with a diversified portfolio (to limit micro-market risk), a balanced mix of small and large clients (for margins and revenue stability), and a low asset-liability mismatch (ALM) risk profile.

Over the past ten years, India’s pharmaceutical ecosystem has been reshaped by a notable rise in the use of generic medicines. This change has been driven not only by the central government’s Jan Aushadhi initiative but also by the emergence of trade-generic pharmacy chains like MedPlus, Zeno, Generic Aadhar, Generico, etc. These players have popularized access to significantly more affordable alternatives to branded drugs (often priced 50% to 90% lower) making them particularly valuable for patients managing chronic diseases. Collectively, these shifts have significantly altered how medicines are distributed, priced, and consumed across the nation.

At the core of this transformation is the remarkable expansion of Jan Aushadhi Kendras (JAKs) under the central government scheme. From a modest network of 100 stores in 2014, the initiative has grown into a vast distribution platform with over 11,000 operational outlets by mid-2025.18 This growth has also been mirrored in its financial scale, with annual revenue rising from less than INR 500 million a decade ago to over INR 18 billion in FY24.19 The program’s extensive catalogue now includes more than 1,800 medicines and 300 surgical products, catering to a broad spectrum of health needs.

Although the rise of Jan Aushadhi and trade generics has likely eroded some market share from established branded generics, their larger impact has been expansive rather than reductive. These initiatives have helped bring previously neglected or excluded populations into the formal healthcare system. For millions who earlier couldn’t afford treatment, Jan Aushadhi has offered their first consistent access to essential medicines, helping improve medication adherence and public health outcomes.

Despite these achievements, systemic barriers remain. Repeated efforts to enforce prescriptions using only generic names have been met with resistance from doctors, largely due to doubts about drug quality, existing brand loyalty, and financial incentives tied to prescribing branded products. Additionally, inconsistent regulatory compliance among some generic manufacturers has reinforced this skepticism, contributing to a persistent lack of confidence among prescribers and patients. The lack of uniform manufacturing standards continues to undermine public trust in the efficacy and safety of generics.

Addressing these gaps requires urgent action to improve regulatory oversight and quality standards across the generic manufacturing sector. Unless these issues are resolved, the dominance of branded generics, buoyed by physician trust and brand recognition, will likely remain unchallenged. Generics must demonstrate not just affordability, but also consistent quality and regulatory reliability to gain wider acceptance in the medical community.

Even so, the Jan Aushadhi initiative, along with the expanding trade-generic ecosystem, has laid the groundwork for more inclusive healthcare access in India. Far from threatening the established pharmaceutical order, these models are complementing the private sector by serving previously unreachable segments of the population. With continued support in the form of robust policy, public awareness, and improved quality benchmarks, these efforts can evolve from supplementary channels into a core component of India’s healthcare delivery architecture.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objectives and risk tolerance levels. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

MSCI India Index is designed to measure the performance of the large and mid-cap segments of the Indian market. The index covers approximately 85% of the Indian equity universe. MSCI Emerging Markets Index captures large and mid-cap representation across 24 Emerging Markets (EM) countries. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

The contents of this material are prepared and maintained by Shikhara and have not been reviewed by the Securities and Exchange Commission of the United States.

The Fund managed by Shikhara may or may not hold all of or some of the securities mentioned in the article.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, and the European Union and pending registration in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.