The market in August reminds us that volatility and opportunity coexist. Amid the noisy news cycle, Asian markets have continued to climb – so don’t be bearish too early. This month, we deep dive into two durable themes: 1) hyper-personalization powered by AI as the new consumer moat, and 2) Asia’s central role in a multipolar industrial revival. For each theme, we highlight companies that exhibit durable competitive advantages; these are the firms best positioned to be the “last man standing” as disruption and geopolitics reshape the investment landscape.

The MSCI All Country Asia Ex-Japan Index gained 1.29% (in USD terms1) over the month of August. Relative to the rest of the region, Singapore and China were the top performers, while India and South Korea were the laggards. Sector-wise, Communication Services and Materials led performance, while Energy and Utilities were the worst performers.

MSCI China gained 4.96% in August, building on momentum since May as the extension of the tariff truce and pro-growth policies fueled the onshore rally. ChiNext and tech/semi stocks led returns, driven by import-substitution and AI chip support as authorities urged for greater reliance on domestic AI chip supply chains. Retail turnover and margin financing hit multi-month highs, as government measures, including interest subsidies for consumer loans and targeted support for EV/tech supply chains, boosted sentiment. July macro was largely weak, including retail sales, FAI (infrastructure and manufacturing investment), and property sales, which came in lower than expected. The only bright spot was exports, which grew 7.2% y/y.

India continued to be the index laggard in August, with equities correcting 2.21%. Foreign portfolio investors remained net sellers, though this was more than offset by domestic institutional investors. Weakness was concentrated in financials and small/mid-cap segments, while the market also faced headwinds from US tariff concerns that added caution ahead of seasonal September volatility. India’s consumer price index (CPI) inflation eased to 1.55% y/y in July, down from 2.10% in June, marking the lowest rate since January 2019. Economic momentum remained strong, with manufacturing PMI rising to 59.3 (vs 59.1 in July).2 Services PMI also surged, increasing by 2.0 points to 62.5, marking the strongest expansion in the services sector since June 2010.3

After a strong 4-month rally, Korean equities pulled back in August, correcting 1.87%. The decline reflected a momentum unwind and month‑end profit‑taking, with foreigners net‑selling ~USD $1.2 billion of KOSPI stocks. Profit‑taking hit defense names hardest despite solid results, while shipbuilding and nuclear‑related names showed mixed reactions amid policy and settlement headlines. Investor caution was also tied to renewed scrutiny around semiconductor supply‑chain developments and qualification progress for advanced memory technologies. Despite the pullback, Korea still remains the top index performer year-to-date (YTD), with equities up 42.58%.

Taiwanese equities returned -0.80% in August as month-end profit taking pared earlier gains after the TAIEX hit a record high on August 27th. Returns were also diminished by a weakening TWD due to capital outflows. Foreign institutional investors were active net sellers, led by outflows from TSMC, Quanta, and Realtek, signaling rotation out of large-cap, AI-exposed names into more defensive, catch-up positions. Hon Hai was a notable exception, drawing ~USD 2.3 billion of inflows on robust AI server demand. On the positive side, Taiwan’s defense complex outperformed amid stronger local drone manufacturing discourse and a significant hike to its 2026 defense budget.

ASEAN posted mixed returns in August, led by Singapore (+6.95%) and Malaysia (+4.66%), while Thailand lagged, slipping 0.25%. Singapore’s rally was broad‑based, driven by strong bank earnings, heavyweight tech exits from net‑selling flows, and inflows into REITs and industrials. Malaysia benefited from commodity strength and recovery in consumer discretionary names, with domestic funds providing steady support. Indonesia and the Philippines saw modest gains as commodity and domestic cyclical themes held up, but foreign selling persisted in selective pockets. Thailand underperformed on profit‑taking in exporters and tourism‑sensitive stocks amid slightly softer macro prints. Across the region, local retail and mutual fund buying helped absorb some foreign outflows, and FX movements modestly trimmed USD returns in several markets.

By now, market participants are becoming used to the news cycle. There continues to be no shortage of headlines over the past month, yet investors are starting to accept that the only thing certain is uncertainty. Through all the noise, markets continue to climb, and like the Roaring 20s, the market is overshooting expectations.

While everyone is focused on the issue of tariffs, the negative impact of tariffs is being mitigated by operating leverage and lower headcount, particularly in white-collar jobs where AI is suppressing entry-level hiring. With the existing workforce, it seems like another company is announcing layoffs every other day. So why isn’t this impacting the numbers?

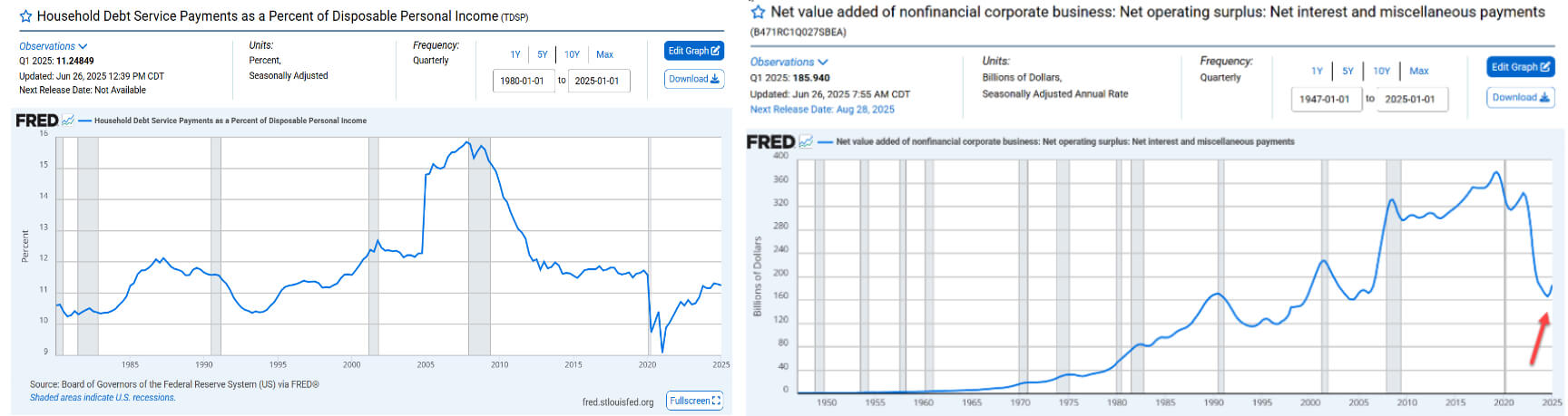

Firstly, consumers still have resilient balance sheets and can absorb near-term impacts. Household balance sheets are the strongest they’ve been in decades, and the same goes for corporates. Interest expense for non-financial corporations has climbed but remain at 20-year lows. In short, there is no balance sheet stress.

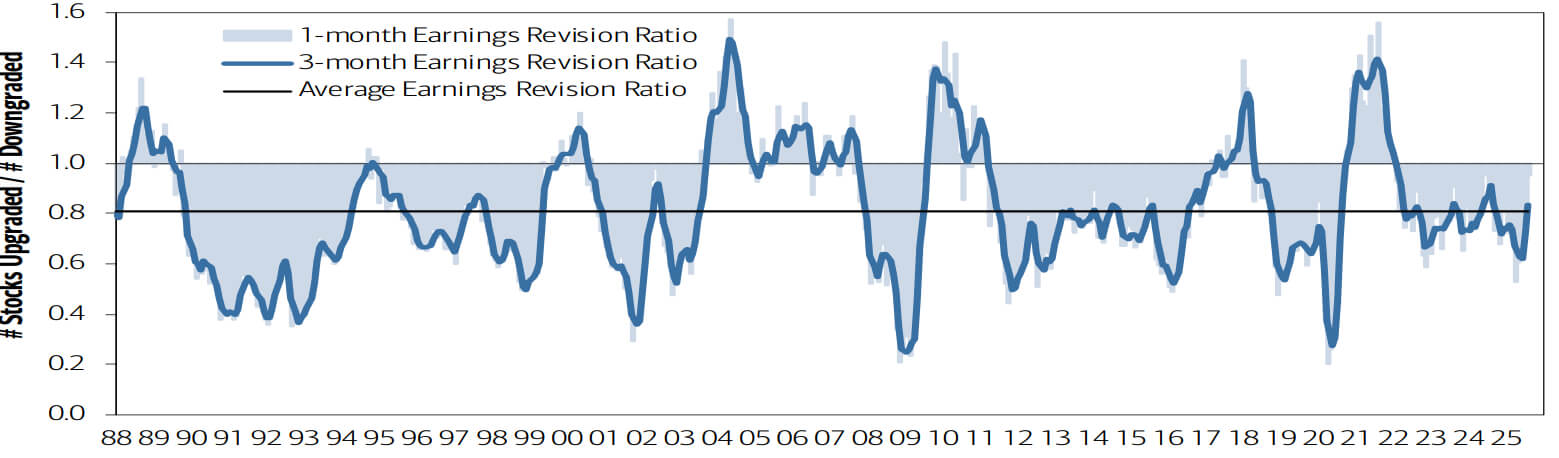

Secondly, corporations will first reap the productivity benefits and can absorb near-term tariff impacts through better operating leverage and AI adoption. The benefits of deregulation are still to come and will also help with productivity gains. We see this through recent earnings upgrades, such as with Amazon and Walmart. BofA’s Global Earnings Revision Ratio (a breadth measure of how consensus earnings expectations are trending) also jumped significantly in August from 0.81 to 0.95 and is approaching a four-year high.4 Historically, when the ratio was near current levels and rising, global equities averaged 10.8% over the subsequent 12 months.5 The ratio is near multi-year highs for the US and China, and has also improved in Europe. All this is happening in the absence of Fed interest rate cuts, which are still on the cards for the coming quarters.

That said, risks are uneven. Small/medium-sized businesses and low-wage workers will feel wage and employment frictions first, and inflation pass-through could amplify those effects. Trade policy remains a wildcard, though rhetoric is moderating and negotiations are mixed (e.g. as in the case of India – more on that below), which likely limits further tariff escalation but does not eliminate trade-related uncertainty. In short: stay disciplined, favor companies with durable cash flows and scalable productivity gains, and don’t be bearish too early.

A softer US dollar can be constructive for global growth as capital moves out of the US and into other economies. That dollar relief eases external financing costs for emerging markets (EMs), lowering FX‑adjusted debt burdens and making dollar‑denominated liabilities easier to service, which accelerates balance‑sheet repair. As corporates and households rebuild buffers and confidence improves, the natural follow‑on is stronger domestic demand and investment. This is the classic EM recovery cycle.

As we wrote back in March, the global economic realignment is increasingly being defined by nation states. With more countries adopting elements of state capitalism, valuation differentials are likely to narrow. The US is moving in the direction of this model. Recent examples include the US government’s 9.9% passive equity stake in Intel, announced in August, and the Department of Defense’s multibillion‑dollar public‑private partnership with MP Materials, the operator of the only rare earth mine in the US, announced in July. If the US is using direct capital and strategic partnerships to secure supply chains and steer industrial policy, it is harder to justify why countries such as China should trade at a persistent discount.

Thus, in a world of state capitalism and growing macroeconomic vulnerabilities in many developed economies, the valuation gap between competitive companies in developed and emerging markets should compress. EM firms are increasingly likely to be re-rated higher – a trend already visible YTD, led by North Asian peers such as South Korea, China/HK, and Taiwan, which have driven much of Asia’s rally.

India remains a compelling long-term structural story: a large, domestic-oriented market with sovereign debt levels under control. There remains some near-term time correction in India, but we don’t expect to see a significant price correction. What time correction does is that it provides a pause for households to repair their balance sheets and set the stage for the next leg of growth. Policy moves have also been supportive, e.g. the GST rate rationalization (to take effect on 22 September ahead of the festive season) improves affordability and demand for the middle class.

In the regional context, a typical cycle is unfolding. Export-oriented North Asian economies typically lead the way in a global recovery, supported by easy liquidity and strong external demand. As the valuations in those markets become stretched, capital tends to rotate into domestically driven economies such as India. For example, we expect multiples of leading Chinese names like BABA to expand 30-40% higher next year. As the valuation gaps narrow, the relative attractiveness will increasingly shift toward India.

In the meantime, the Indian government is not letting this slowdown go to waste. They’re also standing their ground against US demands despite hefty tariffs to protect their own national interests. Rather than direct retaliation, the government has prioritized domestic stimulus like the GST cuts on hundreds of goods (potentially lifting consumption by ~USD 20 billion), and market diversification via free trade agreements (FTAs) with the EU, UK, and others like Peru. As India enters a tough season of challenge, these measures signal a clear push to revive reform momentum and restore animal spirits to kick‑start growth.

We have written extensively about our macro outlook, including our 8 key market debates, the coming investment cycle, and the global investment distortion over the last two decades. What does this mean in terms of our investment focus? While it helps to know what policies are coming next, the most durable opportunities lie in companies that directly address two defining themes of the next decade: 1) rapid AI and technology advancement, and 2) rising geopolitical fragmentation in a multipolar world.

More importantly, we know that because of excessive debt for developed market sovereigns and AI-led job displacement, there’s a deflationary challenge coming. That makes it critical to prioritize companies that are disruptors within their category who can emerge as market leaders – these are the businesses that will be the last man standing. Let’s dive into what we mean.

A lot of the attention has gone to the AI data infrastructure buildout and the vendors that supply it. However, the bigger value creation, which we’ve always maintained, will come through margin expansion of consumer companies. Even amid softer top-line growth that’s not fully reflective of a global recovery, operating profits are rising as companies extract efficiencies from cost rationalization and AI adoption. The question for consumer firms in a fast-moving tech era is: how do you ensure that you are the last-man-standing? The answer is hyper-personalization.

We wrote about this back in January. The winners will have three characteristics that they can leverage:

With those building blocks in place, integrating large language models (LLMs) and AI tools enables consumer-facing companies to materially improve and deepen customer engagement and experience. Some firms are already raising the bar, becoming more relevant and personalized than ever, and consumers now expect that level of tailored interaction. Of course, ethical use and robust data‑privacy safeguards are non‑negotiable. But the truth is – people respond to personalization. When firms can deliver the most relevant content, information, or product at the exact moment of need, then engagement, conversion, and loyalty rise.

Here are some companies that we think exemplify this theme:

| Companies Benefiting from the Adoption of Hyper-Personalization | |

|---|---|

| Tencent | Tencent launched its proprietary LLM, Huanyuan, in September 2023. It was developed in-house to power AI-driven applications across its ecosystem, including WeChat, QQ, gaming, and enterprise services like SiriusBI.

In WeChat, the Yuanbao AI assistant, powered by Hunyuan Turbo S, offers tailored document analysis, smart replies, and real-time translation, adapting to user behavior for intuitive interactions. Hunyuan’s advanced natural language processing (NLP) curates personalized content feeds to boost engagement while filtering out spam. In gaming, player data analysis drives customized challenges, increasing immersion. Tencent’s domestic games revenue grew 17% y/y in Q2 2025, with AI mentioned as a strong contributor.6 Hunyuan’s AI accelerates content production, enabling richer Player versus Player (PvP) and Player versus Environment (PvE) experiences with virtual teammates and realistic non-player characters (NPCs) for human-like interactions. Elsewhere, AI-powered adtech helped the Marketing Services business revenue grow 20% y/y in Q2 2025, with Video Accounts and Mini Programs marketing up ~50% y/y, and Weixin Search up ~60% y/y.7 All of this was in addition to the AI-driven cost efficiencies, which contributed to solid margin improvements, stronger operating profit, and free cash flow. |

| Prosus | As the largest shareholder of Tencent, Prosus has been actively learning from its holding, applying insights from Tencent’s strategies to its own portfolio companies.In OLX, Prosus’ classifieds business, AI helps personalize listings by turning searches and behavior into searchable vectors, combining that with recommendations based on what similar users like, and quickly updating rankings so that users see the most relevant items. As of late 2024, this AI use case resulted in >230% increase in listing views, +450% in buyer replies, +118% in deliveries, and 22% revenue growth from value-added services.8

AI adoption also led to significant outcomes in Prosus’ food delivery business, iFood9:

|

| Sea Limited | We first wrote about Sea in our Q4 2024 commentary (see pg7), but this is a company that we’ve liked for some time. Sea continues to deepen its competitive moats, notably through a robust AI strategy deployed across Shopee (e-commerce), Garena (gaming), and Monee (fintech). Combining external partnerships (e.g. with OpenAI, Google, WIZ.AI) with internal R&D from Sea AI Lab, the company has delivered greater hyper-personalization and automation across:

|

| Grab | In a similar approach to Sea, Grab is leveraging AI across its super-app through a mix of partnerships and in-house innovation. Collaborations with OpenAI and Anthropic have produced tools like the AI Merchant Assistant and AI Driver Companion, while its Singapore-based AI Centre of Excellence develops foundation models that predict user actions and enable hyper-contextual features such as Shared Saver, Grab for Families, and travel-focused services.AI also powers large-order logistics, real-time flight-linked ride booking, restaurant discovery, and inclusive accessibility features like improved voice recognition for local accents. On the business side, AI optimizes campaigns, e.g. to boost high-value users while reducing costs, and enhances operational efficiency to support profitability. |

These are great examples of B2C companies that are tech-native and have effectively adopted AI to create a durable competitive advantage. This is particularly critical in China, which is experiencing a deflationary period. Here, we want to focus on sectors with high emotional connection where consumers are less price-sensitive. While shopping and e-commerce have become commoditized, companies that can optimize through hyper-personalization and offer experiences with deep consumer connections (e.g. in music, gaming, etc.) will capture disproportionate market share. Tencent Music, for example, is a position we’ve held since Q4 2024 and exemplifies this trend. Gains in average revenue per user (ARPU) and a steady uptick in Super VIP (SVIP) subscriptions show consumers are willing to pay for premium, individualized experiences.

In July, we published our white paper “The Industrial Revival: Asia’s Strategic Role in a Multipolar World.” That paper set out the framework: governments across the globe are embracing industrial policy, supply chains are fragmenting under geopolitical pressure, and Asia, led by South Korea, Japan, India, and China, has become the backbone of global industrial renewal. In a world where every nation is moving to safeguard its own interests, the industrial and defense companies that are able to supply critical capabilities will be the last man standing.

We also return to the theme this month, following our Senior Investment Analyst, Marcus Chu, who attended an investor conference and site visits in Korea in late August. The conference made clear that Korea is emerging as a central pillar of the global capex cycle. Attendance was the strongest in years, reflecting renewed global investor interest. Corporates were also more proactive in addressing governance reforms through the government’s Value-Up Program. Local investors remain skeptical until they see concrete progress, but global institutions are already positioning for upside.

What Marcus noted from the conference is that industrial activity is on the rise. Management teams across shipbuilding, defense, and power equipment pointed to sustained US capex demand, strong order books, and structural drivers in energy security and defense. This is not a short-lived recovery. These firms are establishing themselves as indispensable in a world that is fragmenting into multiple power blocs. Here, we dive into some of the companies we met:

These meetings reaffirmed our view that, in a multipolar world shaped by geopolitical fragmentation, South Korea’s industrial and defense sectors are pivotal to the global industrial revival. Their export-driven backlogs, technological leadership in defense, power equipment, and shipbuilding, as well as their alignment with US/European reindustrialization efforts, position them as vital global partners.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return, and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Private Placement Memorandum for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The MSCI AC Asia ex Japan Index captures large and mid-cap representation across Developed Markets (DM) countries (excluding Japan) and Emerging Markets (EM) countries in Asia. The index covers approximately 85% of the free float-adjusted market capitalization in each country. The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips, and foreign listings (e.g. ADRs). The index covers about 85% of the Chinese equity universe.

The contents of this material are prepared and maintained by Shikhara and have not been reviewed by the Securities and Exchange Commission of the United States.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom and the European Union and pending registration in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.