While short-term headwinds may be testing investor patience (whether it’s tariffs, urban demand softness, or shifting global trade), India’s structural story remains intact. Amid the market volatility and geopolitical noise, we remain constructive – favoring a ‘buy on dips’ view and focusing on long-term fundamentals. In this report, we share our responses to the key debates within Shikhara’s Investment Team that are shaping our investment outlook for the months ahead. This report addresses both global market themes and India-specific developments, with deep dives into local dynamics such as the recent 50% tariff. Enjoy!

MSCI India fell 5.00% (in USD terms1) over July, underperforming regional peers as the 25% US tariff announcement weighed heavily on sentiment. All sectors ended lower during the month, though Consumer Staples and Health Care were the relative top performers, while IT and Real Estate were the laggards.

The Nifty experienced consecutive weekly declines as global and domestic headwinds compounded the impact of a mixed earnings season. Foreign portfolio investors were net sellers in July, with net outflows of USD 2.1 billion, more than offsetting the net inflows of USD 1.7 billion in June.2

Goods and services tax (GST) collections continued to signal stable underlying consumption, with gross receipts rising 7.5% y/y to INR 1.96 trillion (USD 22.4 billion) in July, up from INR 1.84 trillion (USD 21.1 billion) in June. Digital payments also maintained robust momentum, with Unified Payments Interface (UPI) transactions hitting 19.5 billion in volume and INR 25.1 trillion (USD 287 billion) in value for July, representing a 35% y/y growth in volume and 22% in value.

Other leading indicators also remained resilient. Manufacturing purchasing manager’s index (PMI) climbed to a 16-month high of 59.1 in July (vs 58.4 in June), reflecting a sharp surge in new orders and robust output.3 Despite the operational strength, business sentiment softened somewhat, as concerns over rising competition and inflation emerged. This did not prevent firms from passing on costs, as improved pricing power was evident. Services activity also gained momentum, with the Services PMI reaching an 11-month high of 60.5 in July (vs 60.4 in June) and marking a fourth consecutive year of uninterrupted expansion for the services sector.4

External demand conditions also showed some improvements. Services exports led the gains, even as goods exports remained flat on a year-on-year basis. The goods trade deficit narrowed to USD 18.8 billion in June, down from USD 21.9 billion in May, as imports declined more sharply than exports.5 However, net services exports fell to a seven-month low of USD 15.3 billion, indicating some volatility on the external front.6

Headline consumer price index (CPI) inflation continued to moderate, falling to 2.1% y/y in June – the lowest reading since February 2019 and bringing the average for H1 2025 to 3.2%. The slowdown was led by a contraction in food prices, though both core (4.5%) and core-core (3.6%) measures of inflation remain relatively elevated compared to recent historical averages.

At Shikhara, we believe that navigating volatile markets requires discipline, open debate, and a focus on substance over noise. India’s underperformance relative to peers YTD has been closely linked to global market movements and evolving trade dynamics, which we are monitoring and actively debating within the team. When we look at our model portfolio, we feel confident that it is positioned in the right sectors with the most dynamic companies to capitalize on the profound changes happening today. Below, we share some of the key debates shaping our current portfolio positioning and outlook.

No. While it’s common to draw comparisons with the tariff increases during the Roosevelt era in the early 1930s, we believe these analogies oversimplify the issue. The dramatic market collapse during the Great Depression was primarily due to a highly leveraged banking system and a lack of appropriate regulation in both the financial system and capital markets.

The reality is that the globalization experiment arguably went too far, especially with the mercantilist strategies pursued by Japan, Korea, Taiwan, and, most notably in recent years, China. Between 2005 and 2018, it became almost unimaginable how much of the world’s manufacturing was concentrated in China, while the rest of the world effectively levered to buy these goods. This model is unsustainable, especially post the supply disruptions during COVID-19, and with the realization that China is not a close geopolitical ally, global supply chains are being re-evaluated.

Compounding this, job creation in developed markets remains a challenge, and we are on the cusp of significant disruption driven by artificial intelligence and automation. These forces are reshaping the global economic landscape, not destroying it. As we have written over the past 12 months, deglobalization is more a process of rebalancing than a harbinger of collapse. Opportunities will emerge for dynamic companies and investors who can adapt to these changes.

It may seem that way, but what we’re witnessing is a world where the tech sector approach to driving innovation has been adopted in national policymaking. The mantra is to iterate quickly, tolerate failure, and prioritize action over endless deliberation. This is a marked departure from the slower, consensus-driven models of the past.

In China, India, and now increasingly in the US, decision-making is concentrated in the hands of a strong leader and a small circle of trusted advisors. With such concentration, there is limited bandwidth and often little patience for deep, exhaustive debate. Yet, paradoxically, this can allow for rapid course correction when things go off track.

Recent examples abound: India’s sudden demonetization in 2016, global COVID-19 restrictions, China’s restrictions on the tech sector, or the US’s abrupt shifts in industrial policy. These are not always the product of long planning cycles, but rather of leaders willing to experiment, fail fast, and pivot as needed.

While this style of governance can generate headlines about “chaos” or “uncertainty,” it also means governments are not afraid to change their approach when circumstances require. In today’s complex global environment, agility may be as important as foresight.

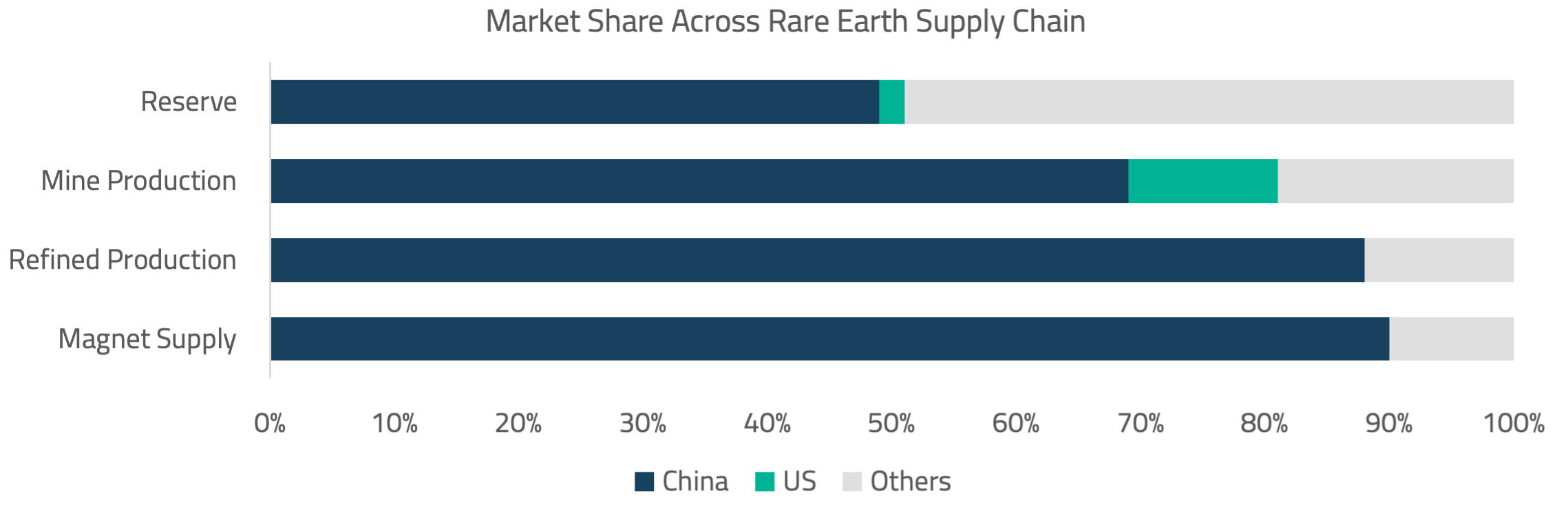

We do not anticipate a direct conflict between the US and China within the next three years. Strategic realities (such as the US’s current dependence on Chinese rare earths and China’s need for further military development) act as constraints on escalation. Moreover, China faces significant internal challenges: high youth unemployment (now exceeding 25%), and export sectors sensitive to global demand. Recent military engagements have exposed the need for further battleground experience for Chinese equipment.

Therefore, rather than direct conflict, we expect to see a period of intense strategic competition and innovation between the US and China. An appropriate comparison is the 1950s Sputnik era, where the race to be the first on the moon sparked an innovation boom in the US and the Soviet Union. Today, both the US and China are likely to channel resources into technology and industrial policy as they vie for leadership across critical sectors. This environment may accelerate innovation on both sides, but with competition unfolding in economic, technological, and geopolitical arenas rather than through open conflict.

We see a shift in corporate profitability patterns. Consumer companies that boosted margins by outsourcing to China may now face cost pressures as supply chains diversify and localize. However, advances in AI and automation could mitigate some of these pressures by enabling new productivity gains.

Given a choice, we will be long investment cycle plays, particularly those enabling the reshoring of US manufacturing. We estimate that the US manufacturing will eventually account for 25-30% of domestic consumption. Policy incentives, such as accelerated depreciation from the One Big Beautiful Bill Act (OBBBA), are likely to further support capital investment and potentially lower effective tax rates by 7-13%. OBBBA’s permanent expensing provisions for domestic R&D and equipment are expected to accelerate technology upgrades across the industrial base. Additionally, new auto loan interest deductions and increased standard deductions may stimulate demand for US-made goods.

In India, we remain constructive on the country’s robust economic foundations. However, recent events have impacted near-term earnings and sentiment – notably, the India-Pakistan skirmish and the ongoing process of household balance sheet repair have weighed on consumer confidence and select corporate results.

Despite these short-term headwinds, India stands out as one of the strongest structural stories globally, supported by low debt-to-GDP and a healthy fiscal position. Additionally, India’s broader appeal is enhanced by its emergence as an alternative manufacturing hub (benefiting from China+1 and government incentives like PLI) and a global services powerhouse with the rise of Global Capability Centers (GCCs).

Recent hiring trends reinforce these shifts: July data showed non-IT sectors such as hospitality, insurance, education, accounting, and architecture leading job growth, while IT and telecom hiring contracted.7 Major players like TCS announced significant layoffs, highlighting stress in the traditional IT sector. These trends underscore the broadening of corporate profitability and opportunity beyond the traditional IT sector as India’s economic transformation accelerates.

This is a “Buy on Dips” market. Unlike the early 2000s or 2008, there’s been no major capital misallocation; in fact, most of the world (outside China) has underinvested since the GFC and is now looking to renew and expand capacity. While there are some pockets of bubbles, they aren’t large enough to trigger a 30% drawdown, though a 5–10% correction could happen at any time, as we estimate one-third of volumes are driven by machines and quant funds.

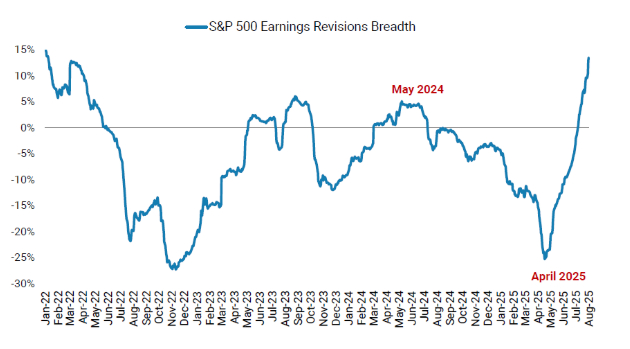

Importantly, the underlying market signals continue to reinforce our “buy on dips” stance. Since April, we’ve seen a V-shaped recovery in the breadth of positive earnings revisions, with analysts raising estimates across a wide range of sectors. This has been accompanied by a decisive rotation into cyclical stocks, which typically lead in the early stages of a healthy market recovery. The combination of broad-based earnings upgrades and cyclical outperformance is a classic sign of improving fundamentals and investor confidence, not of a late-cycle rally or a market on the verge of a downturn.

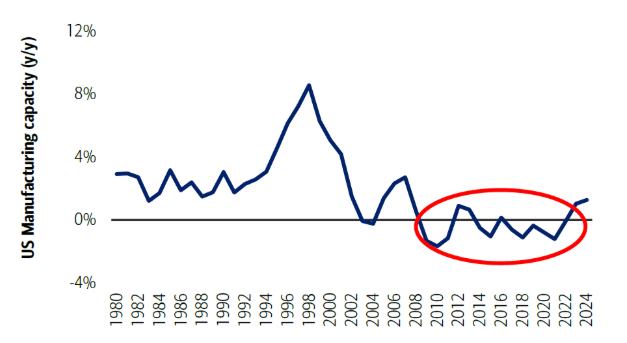

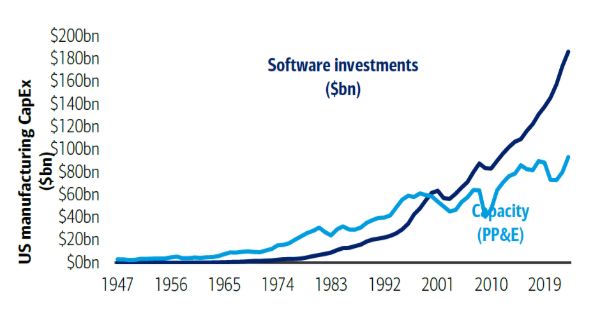

Another reason to stay constructive is the sheer age of U.S. capital stock, which now averages over 23 years – the oldest in post-war history. Years of underinvestment have left infrastructure and industry overdue for renewal. This creates a powerful, multi-year tailwind for capital spending, supporting both earnings growth and a broad-based market recovery.

For India, history shows that during periods of global recovery (e.g. in 2016 and 2019), North Asian markets tend to outperform first due to cheaper valuations and greater cyclicality, but India catches up to deliver strong performance in the subsequent year. We see this pattern repeating, with India underperforming its peers YTD. Additionally, household balance sheet repair continues after two years of excessive, unconstrained growth in unsecured consumer lending – a trend that regulators stepped in to control last year. While this necessary process is weighing on urban demand, the rural economy is showing notable strength. We anticipate urban recovery to follow by late Q3 or early Q4 and maintain a “buy on dips” view for India.

In an era of state capitalism, the traditional boundaries between governments and central banks are increasingly blurred. Today, policymakers in the US, Europe, India, and China are closely coordinating fiscal and monetary responses, often prioritizing national objectives over central bank independence.

This dynamic resembles the pre-1985 Reagan/Thatcher era, when monetary and fiscal authorities worked in tandem to manage economic challenges. The playbook is to inflate out of the debt problem, like in the 1950s. We see this with the European Central Bank (ECB), Reserve Bank of India (RBI), and the People’s Bank of China (PBOC) – all central banks are closely aligned with the respective government’s priorities.

Thankfully, AI-driven productivity gains and a surplus of white-collar workers should help contain wage inflation pressures.

In a world where growth is uneven and opportunities are scarce, emerging markets reliant on favorable terms of trade may struggle. However, those with strong talent pools like China, India, Korea, Taiwan, and Vietnam are better positioned to succeed.

This is especially true with the AI revolution. For countries to fully capitalize on such transformative technological change, they must combine large, skilled workforces supported by effective education systems, with sophisticated financial markets capable of mobilizing large-scale industrial investment, and robust patent ecosystems to protect and monetize innovation. These elements amplify technological advantages into multi-generational economic leadership. Among EMs, Asia stands out as best positioned on these fronts, having invested heavily in talent, patents, and advanced financial systems, which sets the region apart from its EM peers.

Within Asia, India stands out for its young, rapidly growing workforce, robust digital infrastructure, and proactive policy reforms. Its emergence as a global services hub, expanding manufacturing base under “China+1,” and commitment to education and innovation position India uniquely to capture long-term growth. These factors, combined with prudent fiscal management, make India a compelling structural opportunity among both Asian and emerging markets.

In an era of state capitalism, the key risk comes from overconfident, authoritarian leaders who believe they are bigger than the markets. Geopolitical dynamics are especially fluid. The US administration faces its own pressures (e.g., from the ongoing Epstein files to Trump’s shifting support within his core MAGA base), which is creating a desire to gain some “victories” ahead of the mid-term elections next year.

For markets like Korea and Japan, it seems Trump was willing to settle for 15% tariffs. In the case of India, however, the situation has escalated: an initial 25% tariff imposed in July was followed by an additional 25% on August 6th, bringing the total to a striking 50%.

We’ve seen this playbook before with China – using dramatic tariffs as a pressure tactic to bring the other party to the negotiating table. India initially stood its ground, believing that its strategic alignment with the US would offer some protection. However, after this latest round of tariffs, we believe that practicality should eventually prevail on both sides. As we’ve seen in the US-China trade talks, headline tariffs ultimately gave way to ongoing negotiations.

Recent press reports underscore how quickly India is adapting to shifting geopolitical realities. Under mounting Western pressure to reduce Russian oil imports, India’s largest refiners have already started to buy millions of barrels from the US and UAE. As the world’s largest buyer of Russian seaborne crude, India’s balancing act between energy security, cost savings, and new geopolitical risks highlights the challenges it faces as global trade alliances and sanctions evolve.

From a macro perspective, we don’t expect the immediate impact of higher tariffs to derail India’s domestic economy. The country’s growth remains robust, driven by internal demand. However, the longer-term impact is on sentiment – especially among multinational companies weighing India as a manufacturing hub in their China+1 strategy. Unpredictable trade policies and tariff shocks can delay or divert investment, undermining India’s ambitions to capture a larger share of global supply chains.

At the heart of the standoff is the agricultural sector, where the US is pressing for greater market access. India’s perspective is that its fragmented farm holdings won’t be able to compete with the scale and efficiency of US agribusiness. However, it’s worth noting that US agricultural exports to India would come in at different price points to local Indian farm produce and would therefore only be relevant to some high prosperous pockets of tier 1 cities, not the mass rural areas.

There is no question that Modi’s government has delivered real progress – for example, digitization, financial inclusion, and governance reform are meaningful achievements. But there is hope for more reform in his third term. Legal, land, and agricultural reforms, along with greater ease of doing business, are now urgent.

Crucially, the need for reform is not just about appeasing the US, as the AI revolution presents an even greater threat. History is clear: the countries that were able to embrace innovation and reform during the last three industrial revolutions are the ones that have enjoyed disproportionate and lasting gains. As the world enters the age of AI, India must open up, modernize, and double down on its tech stack and regulatory overhaul.

Outside of geopolitics, another key risk is the potential for rising bond yields. If uncertainty stemming from the Trump administration undermines US institutions to the extent that investors lose confidence, then capital that was once almost automatically allocated to the US could look for opportunities elsewhere. That kind of outflow puts upward pressure on bond yields and downward pressure on the dollar, making it harder for the Fed to cut rates. The end result is a stickier inflation environment and a structurally higher cost of capital for businesses and consumers alike.

Given this, and contrary to conventional views, we actually consider some softness in economic data as beneficial. Recent signs, such as a slowdown in consumption and weaker labor figures, are welcome, as robust data often emboldens policymakers to take more aggressive, and potentially disruptive, actions. Softer data serves as a reminder of economic fragility and helps temper the risk of overreach, especially in the context of escalating tariffs.

On the market side, however, underlying conditions remain robust. With earnings breadth improving and cyclicals outperforming defensives, recent market signals point to continued resilience. Meanwhile, our conversations with corporates confirm a significant commitment to capital expenditure, particularly in the US, where hyperscalers are driving demand.

The key constraint for this capex is energy availability, with companies willing to pay higher prices to secure it. Once corporates commit to capacity, utilities follow suit. The US’s time-bound incentives, such as those in the “Big Beautiful Bill,” further encourage this investment. From an AI perspective, rapid capital deployment is necessary, and the government appears focused on removing bureaucratic hurdles to accelerate these trends. This alignment of sovereign priorities, corporate investment, and infrastructure buildout is what keeps us bullish on the new investment cycle.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objectives and risk tolerance levels. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

MSCI India Index is designed to measure the performance of the large and mid-cap segments of the Indian market. The index covers approximately 85% of the Indian equity universe. MSCI Emerging Markets Index captures large and mid-cap representation across 24 Emerging Markets (EM) countries. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

The contents of this material are prepared and maintained by Shikhara and have not been reviewed by the Securities and Exchange Commission of the United States.

The Fund managed by Shikhara may or may not hold all of or some of the securities mentioned in the article.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, and the European Union and pending registration in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.