Our message last month was “don’t be bearish too early,” and that remains our stance. A measured tariff outcome, China’s re‑rating, and Korea’s industrial upswing have rewarded patience, while AI’s diffusion is shifting value to B2C adopters. These calls have underpinned the Fund’s strong year-to-date performance. In this commentary, we unpack the reasoning behind each view and how our on‑the‑ground diligence, cross‑market signals, and disciplined approach are informing our positioning.

The MSCI All Country Asia Ex-Japan Index was up 11.07% (in USD terms1) over Q3 2025, driven by a strong rally in September of 6.84%. Relative to the rest of the region, China and Thailand were the top performers for the quarter, while the Philippines and India were the laggards. Sector-wise, Communication Services and Consumer Discretionary led the performance over Q3, while Energy and Utilities were the worst-performing sectors.

MSCI China surged 9.80% in September, bringing Q3 returns to 20.79%. China and Hong Kong equities staged a strong rally, led by AI and tech sector optimism, anti-involution efforts, and momentum-driven buying after persistent underweight positioning. Upbeat sentiment around AI investment and capital expenditure propelled Alibaba’s share price higher in September, lifting the broader supply chain. Meanwhile, ongoing US-China trade dialogue and the upcoming release of the 15th 5-Year Plan at the Fourth Plenum in October reinforces a more constructive domestic and external backdrop.

MSCI India Index declined 6.63% in Q3 2025. Investor sentiment weakened in July and August due to US tariff announcements, but September recorded a modest gain of 0.51%, driven by domestic policy support. Automobile sales were strong towards the end of September, supported by the recent GST reforms, indicating sustained domestic demand. India’s consumer price index (CPI) inflation rose to 2.07% y/y in August from 1.61% in July, reflecting the first monthly increase in 10 months. Economic activity stayed resilient, though the manufacturing PMI eased to 57.7 in September from 59.3 in August2. Similarly, the services PMI declined by 1.6 points to 60.9, influenced by softer overseas orders.3 Despite these moderations, India’s PMI readings remain the highest in the region.

After a slight pullback, Korean equities rebounded sharply in September, rising 10.54% and bringing Q3 returns to 12.83%. KOSPI reached an all-time high, driven by renewed AI optimism and continued momentum in Korea’s reform agenda. Foreign investors purchased a net $5.3 billion of KOSPI-listed stocks, the largest monthly inflow since February 2024. Gains were led by technology stocks, supported by strength in HBM and AI names, as sentiment improved on expectations of US interest rate cuts and developments around Project Stargate. Investor confidence was further lifted by Lee’s confirmation that the major-shareholder threshold for capital-gains tax would remain at W5 billion, reinforcing optimism in the government’s pro-investor stance.

Taiwanese equities gained 14.66% in Q3. Like South Korea, following a brief pullback in August, the market rebounded strongly in September, rising 9.43% for the month. The rally pushed Taiwan to new highs, supported by continued AI-related capital expenditure from US hyperscalers and a robust earnings season from TSMC and key supply-chain players.

ASEAN markets saw mixed returns in Q3. Thailand was a standout, with equities gaining 17.57% over the quarter, driven by a rebound that began in July, when foreign inflows resumed amid easing concerns. The momentum carried into September following the appointment of Prime Minister Anutin Charnvirakul and the unveiling of a clearer political transition framework. The Philippines and Indonesia were the region’s laggards, despite modest foreign buying following US interest rate cuts. Meanwhile, Singapore and Malaysia came in the middle of the pack, with gains of 8.27 % and 6.41 %, respectively, in Q3. Singapore’s upturn was broad-based, driven by strong bank earnings and inflows into REITs, while Malaysia benefited from commodity strength and a rebound in consumer discretionary names.

Back in March, we wrote that it was the darkest before dawn. While markets panicked over US tariff headlines, we focused on the broader implications and likely geopolitical pathways. Coupled with a level-headed view of rapid AI advances and tech disruption, that framework helped us make several key calls that have driven our strong YTD performance.

Here are the four key calls that we got right:

China will re-rate as economic structures converge. Economic structures globally are looking more and more similar. The US’s approach to capital allocation echoes elements of state capitalism, e.g. reallocating capital through incentives to onshore manufacturing, and pursuing industrial policy such as the CHIPS Act. As economic structures converge, we think valuation multiples should converge as well. The key question then is: why should China trade at a 50–70% discount to the US? Perhaps a narrower gap of 20-30% would be more reasonable. We acted on this view early, increasing allocations to China and Hong Kong since late last year. Our approach was nuanced, with a focus on category disruptors and market share gainers across sectors. We maintained our conviction through all of the noise this year, and the subsequent re-rating validated our call.

US-China tariffs will not be as bad as feared. Our China positioning also benefited from a more measured view on tariff outcomes. Despite campaign‑trail rhetoric touting triple‑digit tariffs, the eventual measures were far less extreme. Much of the interaction has been rhetorical “shadowboxing” between the two leaders, constrained by deep economic interdependence that would take years to unwind. The US relies heavily on China for critical inputs, including rare earths and battery materials, and policymakers faced the practical risk of consumer shortages and inflation. Large US retailers were warning that shelves could be empty by May and that restocking cycles would slip, which tempered Washington’s appetite for escalation. For China’s part, the goal is to avoid social unrest. Headlines about contract factory workers being laid off and temporary lines going dark underscored the risk of layoffs feeding social tension. We judged a sharp escalation as unlikely given these constraints, which strengthened our conviction in our exposure to China even as many investors pulled back.

Korea will emerge as a global trading partner. If the US is intent on reducing reliance on China, who will fill the gap for needs in defense, industrials, and power grid upgrades? And it’s not just the US. In May, we argued that a major, multi‑year capex cycle was forming after 17 years of underinvestment post‑GFC. US infrastructure rebuilds, rising European defense budgets, and India’s expansion are creating openings for Asian industrial champions, and Korean industrials are the natural partners. They have strong preservation of heavy-industry ecosystems, access to cost-efficient inputs, deep engineering know-how, and a long track record of execution with developed-market (DM) clients. We leaned into this early, adding to our Korea exposure since May, with positions including Hyundai Electric in transmission and grid systems, and Hyundai Heavy and Samsung Heavy in shipbuilding. A further tailwind to the Korea story is the country’s Corporate Value‑up agenda. Greater parliamentary stability is refocusing attention on governance, capital returns, and re-ratings for Korean equities.

AI-driven B2C platforms will be the real AI story. Tech enablers have a compelling capex story, with extraordinary sums flowing into data centers. This echoes prior buildouts around Y2K of fiber optics and telco networks. As in those cycles, heavy spending on backbone infrastructure risks low returns for the builders. In our view, the greater value accrues to the users of that infrastructure. We wrote in January that as AI infrastructure and hardware become commoditized, attention will shift to companies that deploy AI to enhance their core businesses. B2C platforms with large, engaged user bases and rich behavioral data can deliver true hyper-personalization with AI, delighting customers and capturing greater market share. In our August commentary, we highlighted how Tencent, Sea Limited, and Grab are applying AI to personalize discovery, pricing, and engagement. These platforms have been among the Fund’s top contributors YTD.

How did we get these calls right? At the outset of the trade war, intent was unclear. We had to take a step back to map the pain points in each economy. With our investment team members based in New York, Hong Kong, and Mumbai, our internal debates focused on first-hand signals from business and policy leaders in each market.

When we launched Shikhara with a three-location model, investors often asked why we were managing Asian equities out of New York. For us, the answer was straightforward – geopolitics would be a major source of uncertainty for the coming decade. Technological disruption and AI would be another. The US remains the largest consumer market and the global innovation leader, so we chose to be close to the action and gain direct perspectives from within the US. Today, no one questions our New York presence.

Another reason we’ve been able to get the big calls right is the team’s depth of experience. Our analysts have lived through multiple cycles, and have covered many companies for more than a decade. Some of these companies came to market with distinct business models but had clear issues to address. With strong management and disciplined execution, the successful ones were able to address those issues and scale.

That focus on quality helps contain portfolio volatility. We back durable franchises that can be the “last man standing” in difficult environments. Risk-adjusted returns and liquidity remain a key focus for us – the Fund’s 12‑month Information Ratio is 1.19. Even with these results, we’ve not taken excessive risk – as of end September, the portfolio trades at just 14.3x P/E on 2‑year forward earnings. Moreover, this is not the end of the cycle. We believe there is still a meaningful runway for growth and cycle longevity as core Asian themes continue to play out.

The Emerging Market melt-up

There are always two sides to a coin, and the same can be said of the current global macro setup. In the US, the economy is in a detox phase with a gradual pullback in excess consumption. On the flip side, in China, reflexivity is at work. Easing monetary policy and government support are driving a market recovery, improving consumer sentiment, and the early return of animal spirits amongst businesses and entrepreneurs.

We often think of the Causeway Bay shopping district in Hong Kong as a barometer of mainland consumer confidence. When I visited a few weeks ago, the area was busy! Mall traffic in the area was some of the strongest I’ve seen since pre-COVID times.

And it’s not just China and Hong Kong. Macro data points across Asia and Emerging Markets (EMs) are inching better rather than worse. For example, Asia ex-India’s PMI4 rose to a six‑month high in September, with new orders strengthening on gains in China, Korea, and Thailand, while India’s PMI, though moderating, remains the region’s highest at 57.7.5

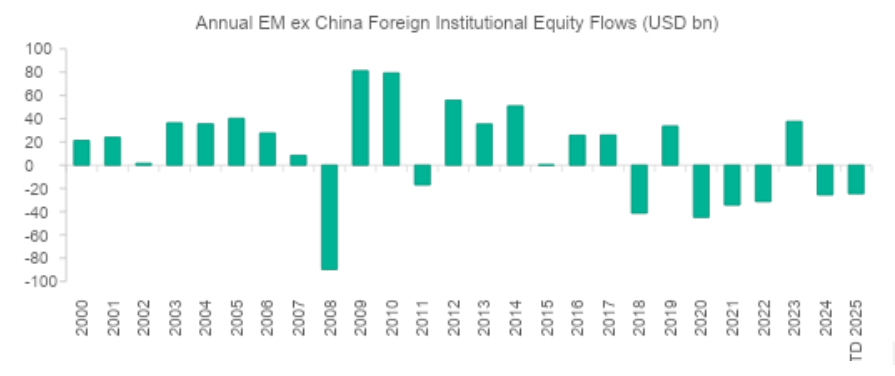

Building on those undercurrents, EMs are also being powered by a weaker US dollar and easier financial conditions. This lowers dollar-debt burdens and pulls capital toward higher real yields in local markets.

On the equity side, investors are rotating from expensive US markets into cheaper EMs, driving multiple expansion. Meanwhile, the AI supply‑chain boom is lifting Korea and Taiwan through chips and power equipment. With inflation easing in parts of Asia and positioning still light despite strong YTD gains, there is room for further inflows as the macro data inches better. European allocators have yet to move meaningfully into EMs, and many APAC investors have sat out the rally. These are ripe conditions for a broad-based EM melt-up, and it’s only just begun.

EMs have been disciplined over the last two decades, strengthening their macro frameworks, e.g. embracing inflation targeting and building FX reserves, resulting in lower external vulnerabilities and higher real yields. In contrast, we joke that Developed Markets (DMs) today look like the EMs of 20 years back, with many exhibiting sustained fiscal deficits, rising debt burdens, heavy use of subsidies and industrial policy, and greater policy uncertainty. The narrowing credibility gap suggests investors may reassess risk premia.

Within EMs, we think Asia is best positioned to win. Why? We have a paper coming out in November that addresses this exact topic. In essence, AI represents the fourth industrial revolution, and Asia has the critical mass of engineering talent, deep supplier ecosystems, and high‑tech manufacturing know-how to scale and monetize this shift. In contrast, most of LatAm and EMEA lack comparable clusters in AI hardware and precision manufacturing, leaving them less able to leverage the immediate capex and productivity gains of this cycle.

Navigating the AI surge: Prioritizing adopters

The AI landscape has accelerated dramatically in recent months, with headlines underscoring the scale of innovation and investment. September alone saw OpenAI’s USD 100 billion partnership with NVIDIA for Project Stargate, expansions to five new US data centers in collaboration with Oracle and SoftBank, and Alibaba’s launch of advanced Qwen3 AI models alongside a USD 3.2 billion funding round for cloud infrastructure. Early October saw OpenAI commit to 6GW of AMD-powered data centers, while also signing partnerships with Samsung and SK Hynix for Korean chips and AI data centers. This rapid progress makes it challenging to track developments or confidently back individual winners amid a proliferation of large language models (LLMs).

Rather than chasing specific technologies or frontrunners, we adopt an attributes-based lens to identify countries poised to benefit from these themes. Which nations possess the infrastructure, talent pools, policy frameworks, and supply-chain integration to contribute meaningfully to and capture value from this tech evolution? Our emphasis remains on AI adopters over enablers, as outlined in prior commentaries: economies leveraging AI for productivity gains across sectors like manufacturing, services, and logistics, and businesses leveraging AI for greater consumer connect and hyper-personalization.

In this vein, China and India exemplify adopters excelling in AI inference and customization, rather than foundational LLM development like ChatGPT. China’s robust data centers and semiconductor ecosystem enable efficient model deployment and tailored applications for e-commerce and logistics, while India’s software talent and digital public infrastructure drive enterprise adoption in fintech and healthcare. These strengths position both to harness AI’s downstream benefits without leading the core R&D race.

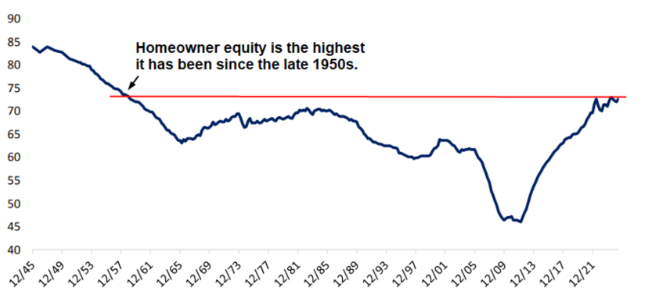

On labor, concerns about AI displacing white collar roles, especially entry-level and middle management, are valid but not yet decisive at a macro level. We have not seen job losses reach a tipping point that becomes a material drag on aggregate demand. Household balance sheets remain resilient, buoyed by the wealth effect from higher stocks, which keeps consumer spending strong. In the US, we see this evidenced in homeowner equity rates, which are the highest they’ve been since the late 1950s.

Even in a scenario of moderated consumption, leading businesses that adopt AI well will consolidate market share in a smaller pie. Thus, we favor disruptors and firms with the balance sheet, data assets, and operational flexibility to become the “last man standing” even if overall demand softens.

Hybrid threats reshaping global risk

The other headlines grabbing our attention lately are the increased hybrid warfare provocations across Europe. Signals from Russia’s hybrid tactics appear to be intensifying, which may warrant a reassessment of risk exposures. Reports in September included unidentified drones entering NATO airspace over Poland and Denmark, and MiG-31 fighter jets briefly crossing into Estonian airspace. The European Parliament characterized these actions as hybrid aggression and urged readiness, though the precise intent and coordination remain difficult to gauge.

A reasonable interpretation is that Moscow could be testing NATO cohesion and exploiting perceived political openings while avoiding explicit escalation. The opacity of authoritarian systems and the deniable nature of cyber and information operations add to attribution challenges and tail-risk uncertainty. While it’s difficult to draw firm conclusions, these developments amplify baseline global risks, underscoring a fraying international order with diminished US-led policing and emergent alliances like expanded BRICS.

From an investment perspective, we would frame this as a discussion on diversification. Investors might consider increasing exposure to EMs with stronger institutional frameworks. Hedging policy and security shocks, including potential NATO-related volatility, may be prudent.

The way we think about our portfolio is the ability to invest across five economic regions (China, Korea, Taiwan, India, and ASEAN), with the flexibility to rotate toward the best risk-reward as conditions evolve.

China/Hong Kong remains our largest exposure and has performed well YTD. We deliberately did not participate in the small- and mid-cap rally, which we view as high beta and vulnerable to sharp reversals if liquidity tightens or US-China tensions re-emerge. Our China positioning centers on B2C consumer platforms that are integrating AI to improve engagement and unit economics, and on companies evolving into global champions with growing overseas revenue. As select names approach fair value and the re-rating phase matures, we will look to use China as a funding source for opportunities elsewhere with better risk-reward.

Korea remains a core allocation across memory, defense, industrials, and shipbuilding, complemented by targeted small and mid-cap exposure through Cosmecca. In Taiwan, our holdings in TSMC, Quanta, and MediaTek anchor our participation in compute, AI hardware adjacencies, and edge devices. Within ASEAN, we are focused on consumer platforms such as Sea and Grab, and on Vietnam through Mobile World Group. Vietnam’s anticipated upgrade to FTSE Emerging status in 2026 could attract meaningful inflows and broaden the investor base.

Given the focus to date on the North Asian recovery, we currently maintain a modest exposure to India. Our long-term conviction in India’s structural growth story remains intact, and the current market consolidation should largely be done. We see India at a stage that, in some respects, resembles China’s position around June 2024, when the PBOC began to shift and policy efforts helped rekindle the animal spirits. India is now pursuing its own mix of pro-growth measures, yet the market doesn’t seem to be taking notice yet. Over the coming months, we expect to gradually rebuild our India exposure, funded by trimming positions in China and Korea as more of the upside is priced in.

Looking ahead, we are reassessing what AI-led disruption implies for end demand. Business models tied to the organized middle class could face pressure if white-collar employment softens at the margin. In this scenario, we may look to increase our exposure to healthcare and select pharma names, where demand is less cyclical and innovation pipelines are improving, and reduce exposure to large-ticket discretionary categories that depend on upper-middle-income spending.

Our edge lies in combining low-volatility construction with dynamic country and sector weighting. The objective here is to compound and generate alpha through uncertainty by adapting to changes in valuation, earnings breadth, and AI adoption, rather than relying on high-beta calls.

Each quarter, we highlight a select number of companies that showcase exceptional growth potential. These stocks on our conviction list represent opportunities we believe will deliver substantial value over the coming years. Here are the standout stocks we’re featuring this quarter.

| Stock | Investment Rationale |

|---|---|

| Alibaba Group Holding Limited |

The underappreciated shift is in Alibaba’s execution. After losing share to PDD, JD, and Douyin, the decline has stopped, and early gains are now visible. Jack Ma’s return has reinvigorated the management team, while the company’s internal message boards are lit up with ideas for “MAGA: Make Alibaba Great Again.” This shows in the integration of its consumer-facing platforms like Tmall and Eleme, and the recent CMR revenue growth numbers. Looking ahead, the real driver of growth is Alibaba Cloud, fortifying its moat in China’s nascent AI boom. We are still in the early innings of AI cloud adoption, and we think Alibaba’s platform is primed for growth acceleration in the coming quarters. Additionally, there is additional value to be unlock from the Ant IPO, which markets have not reflected in the price. |

| Zijin Mining Group Co., Ltd. |

Zijin Mining offers rare volume growth at scale. Over the past decade it has delivered sustained production increases while peers have struggled to add volume. The company sits in the top quartile for cost efficiency in both copper and gold, supporting its resilient margins. Copper and gold drive about 70% of profits for Zijin Mining, which is a powerful mix. Copper is leveraged to electrification, grid and datacenter build-outs, and US reindustrialization. Gold benefits from rising geopolitical risk and a softer dollar. Despite a strong run, the stock trades around 15x CY26 forward earnings for one of the sector’s highest growth profiles. Zijin Mining has also materially improved its carbon footprint in recent year, screening well on ESG versus peers. With durable growth and a tight copper market, we see a credible path to further upside. |

| Cosmecca Korea Co., Ltd. |

Cosmecca is a top three Korean original design manufacturer (ODM) with a differentiated edge: a US manufacturing footprint. In a world of tariff uncertainty and policy support for onshoring, brand owners increasingly prefer domestic production, and Cosmecca is positioned to win in that shift. The company also benefits from the rise of indie brands that prize speed, flexibility, and bespoke formulations. These are areas where Cosmecca’s R&D and agile capacity stand out. Valuation is compelling at roughly 13.8x two-year forward earnings, a discount to peers given its global optionality. As utilization improves at overseas plants, we expect operating leverage to drive a positive surprise in margins and earnings. |

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return, and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Private Placement Memorandum for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The MSCI AC Asia ex Japan Index captures large and mid-cap representation across Developed Markets (DM) countries (excluding Japan) and Emerging Markets (EM) countries in Asia. The index covers approximately 85% of the free float-adjusted market capitalization in each country. The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips, and foreign listings (e.g. ADRs). The index covers about 85% of the Chinese equity universe.

The contents of this material are prepared and maintained by Shikhara and have not been reviewed by the Securities and Exchange Commission of the United States.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom and the European Union and pending registration in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.