Our commentary this month arrives at an inflection point. While Indian equities have lagged and sentiment remains subdued, we see this as healthy pressure rather than alarm. After three weeks of travelling across Asia last month, I came away more confident in India’s entrepreneurial energy. Companies acknowledge near‑term pressure from US demands and tariff noise, but they’re responding with resilience. Moreover, encouraging signs are emerging beneath the headlines, with stronger household balance sheets, strong IPO activity, and policymakers doing all the right things to stimulate growth. The market is yet to take notice, and we think this is exactly the best time to buy.

Indian equities have underperformed regional peers in recent months, declining 6.63% (in USD terms1) in Q3 2025. Investor sentiment weakened in July and August due to US tariff announcements, but September recorded a modest gain of 0.51%, driven by domestic policy support. Foreign Institutional Investors (FIIs) net sold USD 8.8 billion of Indian equities in Q3, bringing year-to-date (YTD) net outflows to USD 17.6 billion.2

Consumer Discretionary was the only sector to deliver positive returns in Q3, while all other sectors corrected. IT and Real Estate were the worst-performing sectors, down almost 16% each over the quarter. The IT sector faced headwinds from the US’s $100,000 hike in H-1B visa fees, raising concerns about squeezing margins for Indian IT firms reliant on US clients. Real Estate equities slumped amid declining housing sales and elevated property prices, despite the Reserve Bank of India (RBI) cutting interest rates in H1 2025. Across the top eight Indian cities, housing sales were up just 1% y/y in Q3 2025.3 However, demand for premium housing (>USD 113k) saw strong demand, and accounted for more than half of the property sales.4

On the positive side, Consumer Discretionary names like B2C consumer platforms and autos performed well over the quarter, buoyed by India’s recent goods and services tax (GST) reforms. The move to simplify rates to 5% and 18% (from 4 GST tiers) came into effect on September 22, 2025, reducing taxes on essentials, electronics, small cars, two-wheelers, and durables. Automobile sales were strong towards the end of September, thanks to the GST changes. The price cuts, high discounts, and pent-up demand drove 17% and 23% growth in passenger vehicle (PV) and two-wheeler (2W) sales during Navratri (the major Hindu festival period) of 2025 vs 2024.5

India’s consumer price index (CPI) inflation rose to 2.07% y/y in August from 1.61% in July, reflecting the first monthly increase in 10 months. Economic activity stayed resilient, though the manufacturing purchasing managers’ index (PMI) eased to 57.7 in September from 59.3 in August. Similarly, the services PMI declined by 1.6 points to 60.9, influenced by softer overseas orders. Despite these moderations, India’s PMI readings remain the highest in the region.

Indian equities have lagged regional peers year to date, and sentiment is subdued. We see that as healthy pressure rather than a red flag. After an unusually strong post‑COVID rebound, policy makers prioritized macro stability over growth. Nominal GDP growth has moderated from 12–13% to 7–8%, which feels like a slowdown only because of the high base. In absolute terms, India remains the fastest‑growing large economy. The grind is forcing a pivot toward productivity, which is precisely what is needed to sustain multi‑year cycles.

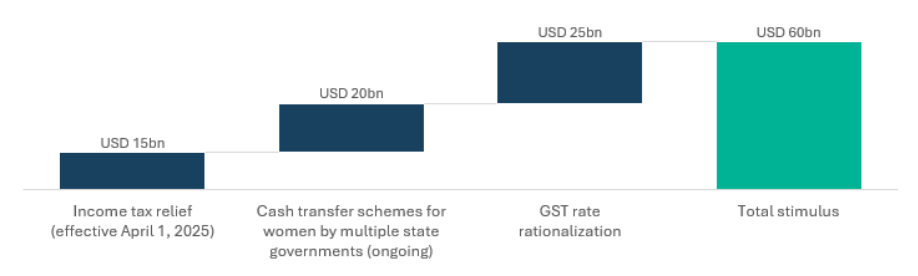

Household balance sheets are quietly improving. Credit taken 12-18 months ago is getting repaid as disinflation eases the burden on wallets. That matters for consumption durability into FY26, particularly for discretionary spending and services. We also expect a policy-driven lift: roughly USD 60 billion of annualized consumption stimulus over FY26–27 (about 1.4% of GDP) via GST rate rationalization, personal income tax relief, and ongoing state cash-transfer schemes for women, supported by monetary easing and better credit availability. With private consumption at roughly 60% of GDP, even modest multipliers can meaningfully support growth.

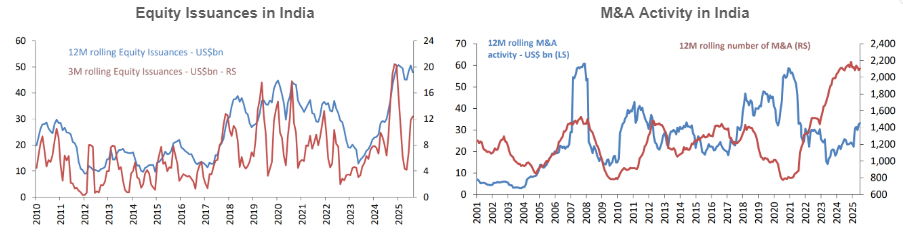

On the corporate side, India has hosted a robust IPO calendar this year and ranks as the fourth‑largest market globally for IPO fundraising in 2025.6 Fresh equity has recapitalized a new cohort of companies that are beginning to hire, invest, and compete.

Policy is catching up to this reality. Twelve to fifteen months ago, we sensed that policymakers were complacent about growth. Today, the tone is more urgent and execution‑led. We are seeing targeted measures in areas like GST simplification, accelerated infrastructure spending, production-linked incentive (PLI) disbursements, and credit support for micro, small, and medium enterprises (MSMEs) and green manufacturing. This is similar to what we observed in China in mid‑2024, when the Chinese authorities leaned in to revive animal spirits. India is now doing all the right things, even if markets have not yet rewarded it.

India: Confidence rising on the ground

On the ground, our conviction is rising. After three weeks across Asia last month, I came away more confident in India’s entrepreneurial energy. Companies acknowledge near‑term pressure from US demand and tariff noise, but they’re responding with productivity gains, disciplined pricing, and new order wins beyond the US. Export‑oriented pockets will feel the US slowdown, yet we’re seeing firms diversify with orders across Europe, deepen ties in China, and broaden their customer mix.

For us, this is a kid‑in‑a‑candy‑store moment. Everyone is reading the negative headlines, but few are sensing the micro data points and the operating tempo on the ground. Foreign institutional investors remain cautious, citing tariff frictions, a slower US end‑market, and headline risks. That pessimism has pushed attention toward China and Korea at India’s expense. History suggests the best time to add India is when investors are a bit bearish.

Investor positioning amplifies the opportunity. While Western FIIs are staying on the sidelines, strategic capital is stepping in. We hear of Japanese investors taking equity stakes in smaller Indian financial firms and adding system liquidity, and Middle Eastern pools and Singaporean pensions increasing allocations. In a world keen to diversify geopolitical and institutional risk, India stands out as a natural regional ally with a reform‑minded policy backdrop.

Our sense is that India won’t let this current discomfort go to waste. The resilience of Indian entrepreneurs, honed by growing up in resource‑scarce environments, positions them to navigate today’s frictions and compound through the cycle. With sentiment still fragile and FIIs underweight, we’re using weakness to add selectively to high‑quality franchises tied to productivity, domestic capex, and the formalization of consumption. The resilience is intact, and the opportunity set is broadening. Now is the time for India to up its game.

The recent H‑1B developments are largely symbolic for now. Leading Indian IT and services firms have already pivoted to local hiring in the US, so near‑term effects look limited. In a world of AI and job protection politics, we think that the more material watchpoints are onshore role exposure and AI‑driven job replacement within the formal sector. More on that below.

Tariff noise remains the key uncertainty. Headlines, such as 100% tariffs on branded pharmaceuticals, underscore the US push to localize 20–30% of consumption. Regarding the tariff on branded drugs, regionally, pharmaceutical contract development and manufacturing organizations (CDMOs) may be affected, but given their relatively low value add in the context of big pharma’s 80–90% gross margins, much of the cost can be passed through. For India, the setup is relatively favorable for generic manufacturers, who stand to benefit.

The AI landscape has accelerated dramatically in recent months, with headlines underscoring the scale of innovation and investment. September alone saw OpenAI’s USD 100 billion partnership with NVIDIA for Project Stargate, expansions to five new US data centers in collaboration with Oracle and SoftBank, and Alibaba’s launch of advanced Qwen3 AI models alongside a USD 3.2 billion funding round for cloud infrastructure. Early October saw OpenAI commit to 6GW of AMD-powered data centers, while also signing partnerships with Samsung and SK Hynix for Korean chips and AI data centers.

Tech enablers have a compelling capex story, with extraordinary sums flowing into investments. This echoes prior buildouts around Y2K of fiber optics and telco networks. As in those cycles, heavy spending on backbone infrastructure risks low returns for the builders.

Rather than chasing specific technologies or frontrunners in large language models (LLMs), we adopt an attributes-based lens to identify countries poised to benefit from these themes. Which nations possess the infrastructure, talent pools, policy frameworks, and supply-chain integration to contribute meaningfully to and capture value from this tech evolution?

In this vein, India exemplifies adopters excelling in AI inference and customization. In our view, the greater value accrues to the users of the AI infrastructure. We wrote in January that as AI infrastructure and hardware become commoditized, attention will shift to companies that deploy AI to enhance their core businesses. B2C platforms with large, engaged user bases and rich behavioral data can deliver true hyper-personalization with AI, delighting customers and capturing greater market share.

This adoption-focused strategy is already materializing across Indian enterprises. While India may not develop foundational LLMs like those emerging from the US and China, Indian companies are pioneering agentic AI applications tailored to their specific industries to drive substantial productivity gains. Some examples include a healthcare company leveraging AI to optimize prescription recommendations across its 15,000 clinicians, ensuring better drug allocation nationwide. One hotel chain we spoke with is deploying AI for predictive building maintenance, reducing downtime and operational costs. These targeted applications are demonstrating how AI adoption can enhance return on equity (ROE).

As adoption scales, dispersion within sectors will widen. We will see a clear divergence between companies that successfully integrate AI and those that lag behind. In this environment, traditional valuation metrics alone are insufficient. We are increasingly focused on identifying companies with the “right to win”. These are companies that possess the organizational capabilities, data assets, and strategic positioning necessary for successful AI transformation.

History suggests that transformative technology cycles create new market leaders, and the winners of today may not be the same tomorrow. While still early stage, we expect superior AI adoption to manifest in accelerated growth rates over the coming years. India’s current growth transition mirrors China’s shift of the last decade, which produced multibagger winners like BYD, Xiaomi, and CATL. Indian entrepreneurs of today are a lot more confident compared to the previous generation, have greater access to credit, and thanks to better infrastructure, digitization, and e-commerce/quick commerce platforms, have a much larger consumer market at their disposal.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. Whereas Shikhara has, to the best of its endeavor, ensured that such, information is accurate, complete and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this material are prepared and maintained by Shikhara and has not been reviewed by the Securities and Exchange Commission of the United States.

The Fund managed by Shikhara may or may not hold all of, or some of the securities mentioned in the article.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom and the European Union and pending registration in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.