The first quarter of 2026 was a study in how quickly narratives can shift. What began as a constructive setup across Asia gave way, in March, to an indiscriminate sell-off as the US-Iran conflict upended global risk appetite. But dislocations of this kind are where conviction matters most. In this quarter’s commentary, we explain why the US is turning inward, why the LLM disruption thesis (upending smart, innovative companies) is losing steam, and why Asia, with its structural resilience, attractive valuations, and high-quality businesses on sale, presents one of the most compelling entry points we have seen in years. Enjoy!

The MSCI All Country Asia Ex-Japan Index was down 1.13% (in USD terms1) over Q1 2026, pulling back 13.70% in March alone. Relative to the rest of the region, South Korea and Thailand were the top performers for the quarter, while Indonesia and India were the laggards. Sector-wise, IT and Industrials led the performance over Q1, while Communication Services and Consumer Discretionary were the worst-performing sectors.

MSCI China declined 8.89% over Q1 2026, though Hong Kong bucked the trend with a 5.46% gain. The quarter was defined by a pivot from policy optimism to geopolitical anxiety. Early-quarter sentiment was supported by the release of full-year 2025 GDP at 5.0% (meeting Beijing’s target), the formal end of the “three red lines” policy, and the National People’s Congress setting a 2026 GDP growth target of 4.5% to 5%, alongside the launch of the 15th Five-Year Plan. Manufacturing activity proved resilient, with the official manufacturing purchaser’s index (PMI) rebounding to a 12-month high of 50.4 in March after two months of contraction, driven by post-Lunar New Year production resumption.2 However, the onset of the US-Iran conflict in early March drove a 7.72% decline for the month as energy input costs surged and risk sentiment deteriorated across the region.

Indian equities underperformed the region, with MSCI India declining 18.09% over Q1 2026. The drawdown was overwhelmingly concentrated in March, with equities falling14.93% as the US-Iran conflict triggered a broad-based risk-off. Foreign portfolio investors (FPI) pulled out a record ~USD 12.7 billion from Indian equities in March alone, the heaviest monthly outflow on record, with FPIs net sellers on every trading day of the month.3 The surge in crude oil prices above USD 100 per barrel was particularly damaging given India’s reliance on Middle Eastern crude, weighing on the rupee and reigniting inflation concerns. Manufacturing PMI fell to a 45-month low of 53.9 in March from 56.9 in February, as input cost inflation hit its sharpest level since August 2022.4 The March weakness overshadowed earlier constructive developments, including the announced US-India trade framework and the landmark India-EU trade agreement.

Korean equities were the region’s standout, delivering a Q1 return of 16.70%. The first two months of the year saw a parabolic rally as KOSPI broke through the 5,000 and then 5,500 levels to fresh record highs, powered by the AI-driven memory semiconductor supercycle. Samsung Electronics surpassed 1,000 trillion won in market capitalization for the first time, while SK Hynix continued to rally on insatiable demand for HBM chips. However, March delivered a sharp 25.39% correction as the Middle East conflict triggered profit-taking after the extraordinary run-up, with foreign investors unwinding positions aggressively. Underlying economic data remained softer than equity performance suggested, with full-year 2025 GDP growing just 1.0% and Q4 contracting 0.2% quarter-on-quarter, though the Bank of Korea projects a recovery to 2.0% growth in 2026.

Taiwanese equities gained 9.15% over Q1, led by TSMC and the broader AI supply chain. January and February saw the TAIEX surge past 35,000 to fresh all-time highs, with foreign institutional investors buying aggressively on the back of continued AI-related capex from US hyperscalers. March, however, saw equities pull back 12.92% as the Middle East conflict amplified pre-existing geopolitical concerns, and with energy disruptions raising questions about semiconductor supply chain resilience. Broader tech names, including Delta Electronics and Hon Hai, gave back earlier gains, though the fundamental chip demand picture remained intact heading into Q2.

Within ASEAN, performance diverged sharply. Thailand was the region’s top performer for Q1 (+15.68%), driven by a decisive early-February election that saw the Bhumjaithai Party secure a strong mandate, and amplified by a surprise 25bp rate cut from the Bank of Thailand to 1.00%. Malaysia (+2.47%) held up relatively well, supported by its position as a net hydrocarbon exporter, while Singapore (-1.14%) was broadly flat, maintaining its role as a relative safe haven. Indonesia was the region’s worst performer, declining 20.45% over Q1 2026, hit by a confluence of negative catalysts, including the MSCI’s warning in late January of a potential downgrade from “emerging” to “frontier” market status.

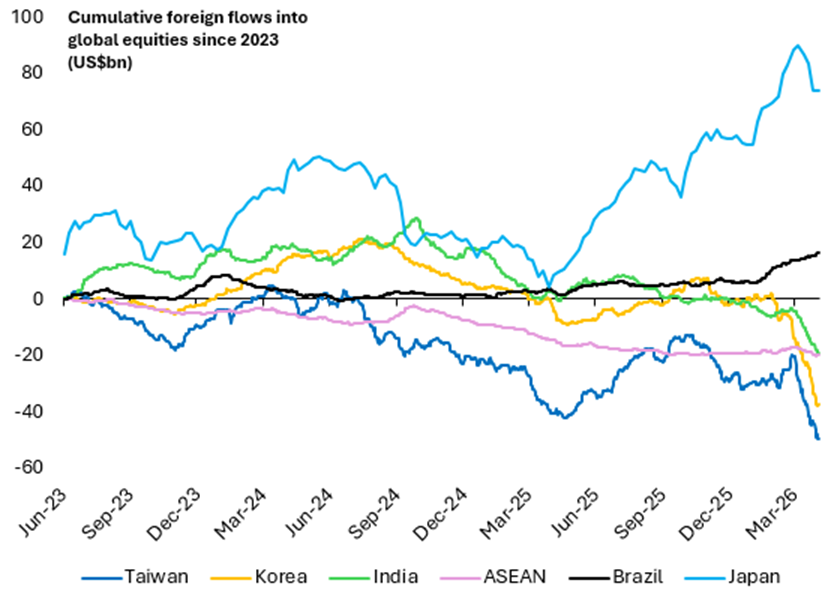

The ongoing conflict in the Middle East has triggered a sharp risk-off move across global markets. Asian equities have not been spared, dragged lower by the kind of “baby with the bathwater” correlations that have historically penalized emerging markets during global shocks. Foreign investors pulled an estimated ~USD 65 billion from Korea, Taiwan, and India in March alone, the largest monthly outflow since 2008-09.5

While the absence of a clear ceasefire remains a near-term dampener, negotiations are underway and making meaningful progress, validating our view that the March drawdown was a temporary dislocation. Markets appear to share this view – Asian equities rallied ~10% month-to-date as of April 13th, on the back of US-Iran negotiations, suggesting that the base case for a resolution is increasingly being priced in.

Our base case remains that the conflict will not escalate materially from here, and that it is in the interest of all parties to find an off-ramp. Negotiations have already made significant progress, and while the most difficult issues, particularly around Iran’s nuclear enrichment program, remain unresolved, neither side has shown an appetite for further escalation. We are optimistic that a middle ground will ultimately be found. China’s role will be critical in this regard; it is Beijing that has the leverage to bring Iran to the negotiating table, and we expect it to use that influence constructively. That said, we are not complacent. We are closely monitoring for signs of further escalation, and we acknowledge the tail risk that a prolonged US blockade of the Strait of Hormuz risks drawing China to the conflict in favor of Iran as they look to secure their energy supplies, which would meaningfully change the trajectory. For now, however, our central expectation is that all parties will seek a resolution in the near term, not least because the US has pressing reasons to move on.

For Asia, the market reaction overlooks a fundamental shift: Asian economies are more structurally resilient, less correlated to the conflict, and better positioned than in previous crises. Before we hone in on why we believe this dislocation presents a compelling buying opportunity for Asia, it is worth stepping back to frame the global backdrop, specifically, the US political cycle and the evolving AI investment narrative, both of which reinforce the case for Asia.

The US is about to get preoccupied with domestic issues, and we believe markets are underestimating what that means for capital allocation. Like any political term, the first half is always the best window to tackle tough external challenges, and this administration has done exactly that: Iran, Venezuela, tariffs, immigration, and sanctions lists. The second half of the term, particularly heading into the midterms, always pivots toward the issues that actually drive electoral outcomes at home. For this administration, those issues are clearly 1) affordability and 2) job disruption. Going forward, we expect the US political conversation to become increasingly inward-looking and, frankly, more populist in tone. By contrast, the rest of the world, and Asia in particular, is likely to look relatively more stable, more predictable, and more investor friendly.

The US is also where the biggest political backlash against AI will come from, and it will come sooner than most investors expect. The US has the highest corporate margins, the most acute affordability crisis among developed economies, and is the fastest adopter of AI. It is therefore also where AI-driven job displacement will hit hardest and fastest, precisely in the white-collar and middle-management segments of the workforce that the MAGA platform would want to defend. European businesses will be slower to adopt AI, and that adoption gap only widens the political asymmetry. So far, we have not yet seen an organized political backlash, but the administration is visibly restless. Once the Middle East situation stabilizes, its attention will rotate squarely to the domestic agenda, and we think AI’s impact on jobs will be next in line. It only takes a handful of politicians to pick up this narrative and run with it and, when they do, the implications for AI capex plans and US corporate margin expectations will be significant.

The knock-on effect is a structural reallocation of global capital. For years, we have highlighted the anomaly that the US represents approximately 30% of global GDP but nearly 60% of global market capitalization. That gap has been sustained by the perception of US exceptionalism and the dominance of US tech platforms. As US policymaking becomes more populist and unpredictable, and as Asian and other EM policy frameworks continue to demonstrate stability, consistency, and industrial focus, we expect that gap to narrow. This is not a short-term trade; it is a multi-year rebalancing that, in our view, has only just begun.

We have been making the case since September 2025 that the next leg of the AI story belongs to the adopters, not the enablers. In that quarter’s commentary, we first laid out why companies that leverage AI to expand margins, improve user engagement, and capture market share would ultimately capture the economic returns from this technology cycle. The fear in the market has been that OpenAI and similar large language model (LLM) platforms would directly disrupt existing consumer internet businesses, justifying their explosive capex and user growth. Our view has consistently been the opposite: incumbents with distribution, data, and brand equity would be the real winners. That view is now being validated.

OpenAI’s consumer ambitions have repeatedly stalled. The company has pulled back on Sora, its much-hyped video generation product. Its agentic tie-up with Walmart was quietly dismantled. Its attempt to build commerce and travel portals inside ChatGPT has failed to gain meaningful traction. These are not isolated misses; they are evidence that cracking the consumer code is far harder than building a great model. Coding is cheap. LLMs look increasingly commoditized, with limited product differentiation across suppliers. What actually wins in consumer markets is a deep understanding of user pain points, feature sets that delight, and the fulfillment and logistics infrastructure that turns intent into delivery. None of that can be replicated with just a clever prompt.

Meanwhile, smart incumbents are paddling hard. Leading consumer internet companies across Asia are integrating AI agents, investing in both front-end and back-end capabilities, and leveraging their proprietary data to improve targeting, engagement, and unit economics. An analogy we often return to is the old taxi industry in the ride-hailing era: rather than being wiped out, the smarter incumbents adopted the apps themselves and benefited from both the existing taxi system and the ride-hailing network. We are seeing the same dynamic now. Companies that recognize the challenge at the right moment will use LLMs to become more competitive, not be disrupted by them.

At the same time, the AI investment wave itself is approaching its natural ceiling. Hyperscaler capex has grown from approximately USD 250 billion in 2024 to roughly USD 650 billion in 2026, and the rate of growth is now decelerating off a high base.6 As the absolute numbers get larger, the pushback grows from multiple fronts. First, the power infrastructure is struggling to keep up: generation capacity is constrained, electricity costs are rising, and data center projects are facing community opposition over water usage and local grid strain. Second, the MAGA base is starting to turn cold on AI as the technology threatens the very career paths (study hard, get a good job) that underpin the social contract of the population. Third, a significant portion of planned AI infrastructure investment is expected to be funded through private credit markets, and those markets are flashing warning signs.

The private credit stress is worth dwelling on. As we flagged in our November 2025 commentary, recent high-profile defaults (First Brands, Tricolor Holdings) have raised concerns about underwriting standards, hidden leverage, and asset-liability mismatches in semi-liquid private credit vehicles. More recently, private credit paper for AI is being placed with high-net-worth individuals, including a member of our own investment team who was pitched to invest. That is a textbook late-cycle distribution signal, echoing the dotcom-era retail push and the pre-GFC securitization wave. The convergence here is what makes us cautious: the largest technology capex cycle in history is being increasingly financed by a credit market that is itself showing cracks. As capital becomes finite, LLM providers will be forced to narrow their focus to where they can earn real returns, and the “everything everywhere all at once” phase of AI spending will give way to a more disciplined cycle. For OpenAI who just saw its revenues surpassed by Anthropic, this is a particularly vulnerable moment.

None of this means we are bearish on AI; it means we are becoming more selective. The AI enabler trade has worked for an extended period, and parts of it still have room to run. But we recognize that the extreme black-and-white treatment of stocks in this cycle will give way to a much more nuanced set of winners and losers as execution risk comes to the forefront.

Against this backdrop of a US turning inward and an AI investment cycle beginning to mature, Asia is uniquely well-positioned. The March sell-off has been indiscriminate, but the underlying case for the region has arguably never been stronger. Below, we lay out four reasons why we believe the current dislocation is a compelling buying opportunity.

We have been active, not passive, through this pullback. Earlier this year, we took profits in several AI enabler positions, particularly in Korea, that had run ahead of fundamentals. The correction has allowed us to redeploy that capital into structural stories at attractive valuations, such as healthcare and internet names. We have added to positions in CATL, the global leader in battery technology, which sits at the cusp of an inflection in energy storage and benefits directly from elevated energy prices. We have also increased exposure to commodity names such as Zijin Mining and China Hongqiao Group, the world’s largest aluminum producer, both of which benefit from supply uncertainty emanating from the Middle East and the structural demand story around electrification, infrastructure buildout, and the global reindustrialization cycle. Importantly, these changes represent less than 5% of the portfolio weight, as we maintain long-term conviction in our portfolio.

The portfolio is built for resilience. Approximately 10% of the Fund is allocated to healthcare names, including Hansoh Pharma and leading hospital operators, that are largely insulated from geopolitical volatility. These businesses are not only defensive in nature but are actively deploying AI to improve productivity and cost competitiveness, making them beneficiaries of the technology cycle rather than victims of it.

Our base case remains that the conflict will move toward resolution in the near term, driven by the strong economic incentives of multiple parties to de-escalate. Historical precedent shows that geopolitical oil shocks tend to create short-lived volatility, and markets typically look through the disruption once supply risks are quantified. When that inflection comes, we expect a sharp recovery in Asian equities, and investors who are positioned ahead of it will benefit disproportionately.

Each quarter, we highlight a select number of companies that showcase exceptional growth potential. These stocks on our conviction list represent opportunities we believe will deliver substantial value over the coming years. Here are the standout stocks we’re featuring this quarter.

| Stock | Investment Rationale |

|---|---|

| Contemporary Amperex Technology Co., Limited | CATL is the global leader in lithium-ion batteries, commanding approximately 39% of the global EV battery market in 2025, the only supplier worldwide with over 30% market share, and an even higher share in energy storage systems (ESS).9 Our conviction rests on three drivers. First, CATL sits at the intersection of two structural demand cycles: EV adoption and grid-scale energy storage, the latter of which is accelerating as utilities worldwide grapple with renewable integration and AI-driven power demand. Second, the company’s technology moat continues to widen, with its LFP and sodium-ion chemistries, fast-charging platforms, and Shenxing and Qilin battery architectures setting industry benchmarks. Third, elevated energy prices from the Middle East conflict reinforce the economic case for electrification and storage globally, accelerating customer adoption. With a fortress balance sheet, dominant market share, and exposure to multiple long-duration growth vectors, CATL offers a compelling combination of scale, innovation, and structural tailwinds. |

| Hansoh Pharmaceutical | Hansoh exemplifies China’s pharmaceutical transformation from generics to genuine innovation, a theme we explored in depth in our recent Asia Healthcare white paper. Innovative products are expected to contribute over 80% of total sales in 2025, up from just 18% in 2020, a remarkable pivot in five years.10 The company has completed five out-licensing deals with global pharmaceutical majors over the past three years, including its most recent transaction with Roche in October 2025 for its CDH17 ADC molecule, which included an US$80 million upfront payment and potential milestone payments of up to US$1.45 billion.11 As global MNCs increasingly turn to China as a source of novel drug modalities, Hansoh is well-positioned to capture a disproportionate share of the opportunity. |

| Narayana Hrudayalaya | Narayana Hrudayalaya is one of India’s leading private hospital chains, distinguished by its ability to deliver complex, high-quality clinical outcomes at a fraction of global costs through system design rather than wage arbitrage. As we detailed in our recent Asia Healthcare white paper, NARH’s Health City Cayman Islands operation has become a textbook case of operational transformation: EBITDA margins nearly doubled from approximately 22% in FY20 to 43% in FY25, while revenue per patient compounded at roughly 14% annually.12 The real prize, however, is the company’s recent acquisition of Practice Plus Group (PPG) in the UK, a major NHS partner currently running at approximately 10% EBITDA margins.13 Management expects margins to move into the mid-teens, with the acquisition turning EPS-accretive from FY27 and delivering 20-22% RoCE by the end of the decade.14 |

As we have shared with many of our investors, the world today is going to be noisy, uncertain, and at times exhausting to navigate. Environments like this demand exceptional leaders, the kind who can see through the short-term fog and build businesses that compound for the coming years. A few extraordinary companies, run by a few extraordinary leaders, will rise above the rest through this environment. These are the companies that we look for, and it is also the kind of company that we strive to be.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return, and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Private Placement Memorandum for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The MSCI AC Asia ex Japan Index captures large and mid-cap representation across Developed Markets (DM) countries (excluding Japan) and Emerging Markets (EM) countries in Asia. The index covers approximately 85% of the free float-adjusted market capitalization in each country. The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips, and foreign listings (e.g. ADRs). The index covers about 85% of the Chinese equity universe.

The contents of this material are prepared and maintained by Shikhara and have not been reviewed by the Securities and Exchange Commission of the United States.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.