February delivered strong returns across much of Asia, but volatility, as ever, was waiting around the corner. The US-Israel and Iran conflict has injected fresh uncertainty, while the indiscriminate sell-off in software and consumer internet names has tested investor conviction. In this month’s commentary, we share our assessment of the Middle East conflict, explain why we believe the AI disruption narrative is overdone, and make the case for the old economy’s quiet resurgence. In times like these, the ability to separate signal from noise is what defines long-term performance.

The MSCI All Country Asia Ex-Japan Index rose 8.21% (in USD terms1) over the month of January. Relative to the rest of the region, South Korea and Thailand were the top performers, while China and Indonesia were the laggards. Sector-wise, IT and Industrials continued to lead performance, while Communication Services and Consumer Discretionary were the worst performers.

MSCI China declined 5.68% in February, pulling back amid subdued economic data and cautious sentiment ahead of the National People’s Congress (NPC). The official manufacturing Purchasing Managers’ Index (PMI) slipped to 49.0 (vs 49.3 in January), partly weighed by disruptions from the nine-day Lunar New Year holiday2. However, the private Caixin/S&P Global PMI told a different story, surging to 52.1 (the highest since December 2020), suggesting stronger conditions among smaller, export-oriented manufacturers. Lunar New Year consumption showed mixed signals: tourism trips hit a record 596 million and spending reached RMB 803.5 billion (~USD 116 billion), both up 19% y/y.3 However, average spending per trip fell 0.2%, reflecting ongoing price sensitivity.

Indian equities returned 1.45% in February, modestly underperforming the broader region but maintaining a positive trajectory. The highlight of the month was the announced US-India trade agreement framework reducing US tariffs on Indian goods from 25% to 18%, while India committed to lower tariffs on US industrial and agricultural products. The deal also included a USD 500 billion purchase commitment over five years, improving trade visibility and reducing uncertainty. Domestically, the FY27 Union Budget maintained fiscal discipline with a 4.3% deficit target while increasing spending 7.7%. The RBI held rates at 5.25% with a neutral stance and raised its FY26 GDP growth estimate to 7.4%. Manufacturing PMI hit a four-month high of 56.9, signaling continued expansion from robust domestic demand.4

Korean equities surged 22.08% in February, extending their position as the region’s standout performer. The KOSPI broke above 5,500 to hit fresh record highs, powered by the AI-driven memory semiconductor supercycle. Samsung Electronics surpassed 1,000 trillion won in market capitalization for the first time, while SK Hynix continued to rally on the back of insatiable demand for high-bandwidth memory (HBM) chips from hyperscale AI data centers. Foreign buying was a significant tailwind, with overseas investors adding meaningfully to their positions, though late-month profit-taking saw a record single-session foreign sell-off. Retail investors, who had largely sat out the earlier stages of the rally, also began participating more actively, adding further momentum this month.

Taiwanese equities rallied 12.75% in February, with the TAIEX surging past 35,000 to a new all-time high, led by TSMC. Foreign institutional investors bought Taiwanese equities aggressively, recording their largest single-day purchases in over two decades. TSMC alone accounted for a significant portion of index gains, as continued demand for advanced logic chips and AI-related capital expenditure from US hyperscalers underpinned the rally. Broader tech names, including Delta Electronics and Hon Hai, also advanced on robust AI server demand.

Within ASEAN, Thailand was the month’s standout, with equities surging 20.57%, driven by a decisive election result on February 8 that saw Prime Minister Anutin Charnvirakul’s Bhumjaithai Party secure a strong mandate, boosting political stability. The rally was amplified by a surprise 25bp rate cut by the Bank of Thailand to 1.00%, which buoyed sentiment in rate-sensitive sectors including banks and property. The Philippines also delivered solid returns of 7.27%, supported by continued monetary easing and improved macro sentiment. Meanwhile, Indonesia was the region’s laggard at -1.14%, weighed down by persistent foreign outflows and subdued commodity sentiment.

Note: This outlook was prepared as of March 8, 2026. Given the rapidly evolving nature of events, we will continue to update our views as the situation develops.

The US-Israel military operation against Iran has been the dominant risk event shaping global markets since early March. The conflict has since widened beyond its initial scope, with disruptions to air travel, energy logistics, and shipping in the Strait of Hormuz.

Our base case remains that the conflict is more likely to move toward a negotiated resolution in the near term rather than a prolonged military engagement. Multiple parties have strong incentives to de-escalate:

We continue to monitor several signals that suggest further escalation may be contained:

The key escalation risks we are watching include any retaliatory action by GCC nations beyond self-defense, which would represent a meaningful widening of the conflict. We are also monitoring for any indication that China or Russia may move beyond rhetoric to direct involvement – this remains a tail risk, though current signals suggest it is unlikely.

From a portfolio perspective, we have made no changes to our portfolio as a result of the conflict. The primary transmission mechanism to Asian markets is through oil prices, but this remains manageable given that oil reserves across the region are abundant, providing a buffer against near-term supply disruption. Any portfolio adjustments made in recent weeks, such as trimming Korean semiconductor positions, were driven by valuation discipline, not geopolitical considerations. However, the sharp correction across Asian equity markets in early March has created value in sectors such as industrials, financials, consumer discretionary, and technology, which we may look to take advantage of as clarity emerges.

Markets have taken a “shoot first, ask questions later” approach to AI disruption. Following the widely circulated Citrini Research report warning of a dystopian wave of AI-led disruption, a massive sell-off swept through software-as-a-service (SaaS) stocks and broader consumer internet names globally. The fear is twofold: 1) that agentic AI will render traditional aggregator apps obsolete (e.g. booking travel, hailing rides, ordering food) without needing a human to navigate an interface; and 2) that “vibe coding” and off-the-shelf large language models (LLMs) will make it trivially easy for enterprises to build in-house tools, eliminating the need for expensive third-party software.

We choose to ask questions first.

Can everything be disrupted? Perhaps not. We believe the current correction is a sort, not a crash. Markets are in the process of separating value-adding platforms with genuine moats from “thin” apps that merely provide an interface for data. That sorting will ultimately be healthy, but in the meantime, the indiscriminate sell-off has created significant dislocations. Here is why we think the market has overreacted.

Enterprise adoption takes time. Ask your own IT team how many systems they plan to replace with AI in the next 12-18 months. The answer is likely very few. There is a process that can’t be shortcut, including evaluation, vendor selection, testing, compliance review, and integration. If enterprises replaced their entire software stack overnight, businesses and economies would falter. As history consistently shows, the impact of technological disruption is overestimated in the near term and underestimated in the long term. Adoption will happen, but on the enterprise’s timeline, not the market’s.

B2B disruption will come faster than B2C. This distinction matters. In our own business, we are already going to our vendors, asking how they are leveraging AI, and requesting that they share some of their productivity gains. That dynamic, where procurement teams demand AI-driven efficiencies from their suppliers, will accelerate disruption in B2B software. B2C, however, is a different story. Consumer-facing businesses that have spent years fine-tuning their operations, managing queries, returns, last-mile logistics, dispute resolution, etc., have built deeply embedded processes that are far harder to replicate. When there is a physical back end involved, operational sophistication is the moat.

Physical assets are being completely discounted. The sell-off has ignored the real-world infrastructure that underpins many consumer internet companies, including their fulfilment centers, warehouses, delivery fleets, and logistics networks. Regardless of how AI might reshape the front-end of consumer discovery, goods still need to move from point A to point B, returns still need to be processed, and service issues still need to be resolved. Companies with these tangible assets will endure.

Differentiation will come from taste and real-world presence, not just technology. The “shoot first” approach assumes that everything will be commoditized. But in a world where software interfaces may converge, differentiation will increasingly come from taste – consumers’ preferences for quality, brand, experience, and trust. AI may help consumers find the best options that match their preferences, but companies still need to deliver goods and services that stand apart. Moreover, it is naïve to assume that consumers will do everything online. The brands that truly understand their customers know this. Shopping malls, for example, have reinvented themselves for Gen Z, blending experiential retail with social and lifestyle elements that can’t be replicated online. The companies best positioned to thrive have an omnichannel presence – tech savvy companies with local interfaces, local presence, and local servicing capabilities to meet customers both offline and online. Another example is ride-hailing, where the online experience needs to match the offline execution. Established players like Grab have over a decade of driver and rider data, trust ratings, and operational refinement that are extremely difficult to replicate, regardless of how sophisticated a new AI-powered entrant may be.

Incumbents are rarely truly disrupted. There is an implicit assumption in the sell-off that established companies are too slow to adapt. But if we look into history, in the consumer internet space, it is remarkably rare for an incumbent with a deep moat to be truly displaced. The only clear example we can point to is ByteDance’s Douyin, where a genuinely superior algorithm disrupted incumbents. Beyond that, incumbents typically adapt, acquire, or simply out-execute. Moreover, many Chinese consumer internet companies have survived periods of far more intense competitive pressure, including regulatory crackdowns and subsidy wars, and have emerged stronger. To assume they will be asleep at the helm while AI disruption unfolds is to dismiss their track record. Smart incumbents will use LLMs to innovate, and those with strong balance sheets can acquire disruptive AI startups or build solutions in-house, much as Microsoft did by rapidly incorporating features and acquiring strategic assets.

AI will expand and retreat, like Uber did. A useful analogy is Uber’s global expansion: the company expanded aggressively into numerous markets where it faced entrenched local competitors with superior regulatory relationships, cultural understanding, and willingness to compete on local terms. Many of these markets generated minimal revenue while consuming disproportionate management resources and creating regulatory liabilities, leading the company to ultimately retreat. We think AI disruption will follow a similar pattern. It will expand into every category and across every market, but not every segment will support rapid AI adoption. We will see it retreat from areas where the unit economics, regulatory environment, or consumer behavior do not align. Companies with deep domain expertise, that can identify and address clear pain points, will continue to provide value.

What about jobs?

The more significant issue, as alluded to in the Citrini report, is AI’s potential impact on employment. As we first wrote about in our September commentary, we believe AI-driven job displacement – particularly in white-collar, entry-level, and middle-management roles – is a real and valid concern. But we do not expect large-scale job losses to materialize within the next one to two years. The more likely timeline is four to five years or beyond, as enterprise adoption cycles and organizational change management takes time.

What we also haven’t fully baked in is the likelihood of government intervention. If job displacement begins to materialize at scale, policymakers will almost certainly respond – whether through regulation, retraining programs, or fiscal measures – to minimize the pain of disruption.

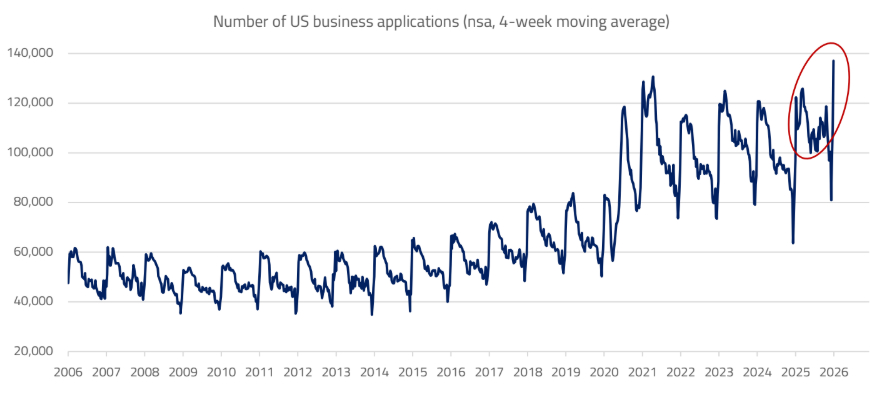

In the near term, we see offsetting forces. New business formation in the US is surging, fueled by AI and LLMs that are dramatically reducing the cost and complexity of launching a company. As these firms scale, they will hire for sales, operations, customer success, and roles we have not yet imagined – underscoring that AI is more likely to strengthen than disrupt the labor market over the next couple of years. The gold rush in AI applications is real: capital that was previously in crypto is now being redirected into AI app development, adding further momentum to the startup ecosystem.

Staying focused on the rotation

As we outlined in last month’s commentary, we maintain that the defining story of this year is the rotation from AI enablers to AI adopters. The early signs are already visible. Nvidia, despite delivering another blockbuster quarter, is seeing its share price plateau. It becomes increasingly difficult for companies at such extraordinary market capitalizations to compound at past levels. Meanwhile, questions remain about whether hyperscaler capex will actually be executed at the levels estimated for the coming years. A significant portion of planned AI infrastructure investment is expected to be funded through private markets, but with private assets now marked down due to software exposure, the ability of private credit to support the required capex is uncertain. The “AI enabler” trade is becoming stretched, and when the market recognizes that it has been too dismissive of the adopter side of the equation, a correction will follow.

This is exactly the environment in which our investment approach comes into its own. We are investing in “last man standing” companies – businesses with deep moats, proprietary data, fulfilment and logistics infrastructure, and demonstrated value-add that cannot be easily replicated by an AI agent or a new entrant. These are the companies that will not only survive the market’s sorting but will emerge stronger from it.

This is a theme we have been building conviction on for over a year. In May 2025, we identified what we called “The Coming Investment Cycle” – the consequence of 17 years of limited capital investment since the Global Financial Crisis, during which the rise of capital-light tech platforms captured the lion’s share of market attention and capital allocation. US companies had been spending overwhelmingly on software rather than physical equipment, while the age of US capital stock reached its oldest level in post-war history. In our June half-yearly report, we formalized this as one of three core investment themes about the multi-year infrastructure and manufacturing capex.

That thesis is now playing out in real time, and the AI revolution is accelerating it. AI is not just a software story – it is profoundly infrastructure-heavy. The buildout demands physical construction: concrete, steel, cabling, transformers, and the skilled workers to install them. Every new gigawatt of AI compute capacity necessitates an ecosystem of railroads, power grids, and logistics networks to support it. In any technological revolution, there are picks-and-shovels beneficiaries, and this cycle is no different.

Meanwhile, the narrative around AI and jobs has been almost exclusively focused on white-collar displacement. But a closer look at labor markets in the US and Europe reveals a very different story for blue-collar workers. The construction industry in the US faces a monthly shortfall of approximately 350,000 workers, with 94% of firms reporting difficulty filling positions.5 The EU also reports labor shortages in 98% of occupation categories.6 Critically, this is not cyclical – it is structural, driven by the convergence of an aging workforce (over 21% of US construction workers are now 55 or older), a depleted vocational training pipeline, immigration constraints, and a cultural bias toward university education that has diverted generations away from skilled trades.7 The combined US-EU blue-collar workforce deficit could widen to 4-6 million unfilled positions by 2030.8

This has several important implications. First, it provides a powerful counterpoint to the AI job displacement narrative. While AI may displace certain white-collar roles over the medium term, blue-collar labor is becoming scarcer, and automation in physically complex sectors like construction and skilled trades remains years away from making a meaningful impact. Second, wage growth in blue-collar occupations is already outpacing white-collar, a trend that is likely to persist and benefit categories catering to this workforce. Third, companies that own physical infrastructure (e.g. the fulfilment centers, logistics networks, and industrial assets that underpin the real economy) are being undervalued by a market fixated on software disruption.

Given this, we maintain a significant exposure to Asian industrial champions in our portfolio, including in shipbuilding, power equipment, defense, and manufacturing – companies that are natural partners in the global rebuild. Our investment approach is deliberately unconstrained, spanning the growth-value spectrum to capture the best opportunities across Asian markets. While we focus on innovative, high-growth companies, we equally pursue value where competitive dynamics are shifting in ways the market has yet to price in. As of today, despite strong performance over the past year, the portfolio trades at just 13.4x two-year forward P/E, while estimated 3-5 year earnings growth sits at 21.3%. Importantly, not every position is firing at once. Our one-year attribution analysis shows that roughly half of securities in the portfolio returned less than 25% last year. We view these not as underperformers, but as dry powder – competitively robust businesses with identifiable catalysts for growth acceleration or value unlocking in the quarters ahead. This balance between contributors and coiled springs is by design, and it is how we build a portfolio that compound through cycles, and not just in them.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return, and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Private Placement Memorandum for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The MSCI AC Asia ex Japan Index captures large and mid-cap representation across Developed Markets (DM) countries (excluding Japan) and Emerging Markets (EM) countries in Asia. The index covers approximately 85% of the free float-adjusted market capitalization in each country. The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips, and foreign listings (e.g. ADRs). The index covers about 85% of the Chinese equity universe.

The contents of this material are prepared and maintained by Shikhara and have not been reviewed by the Securities and Exchange Commission of the United States.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.