February underscored a shift in global market dynamics – while US exceptionalism showed cracks under mounting fiscal pressures and policy uncertainty, Asia, led by China, emerged as a bright spot. As markets price in these structural recalibrations, we believe that true insight comes from recognizing these shifts early, not just following the latest trends. This perspective enabled us to effectively capture the China rally, which we detail in our commentary this month. These are indeed interesting times to navigate, but with each passing week, our conviction in the rotation of capital into Asian markets strengthens. Enjoy!

The MSCI All Country Asia Ex-Japan Index was up 1.05% (in USD terms1) over the month of February, as weaker US performance led to a drag on developed market equities in favor of emerging markets and Asia, though performance was largely focused on China. Relative to the rest of the region, China and Hong Kong were the top performers, while Indonesia and Thailand were the laggards. Sector-wise, Communication Services and Consumer Discretionary led performance, while Energy and IT were the main underperformers.

MSCI China returned 11.67% in February as economic data and policy signals turned decidedly positive. Sentiment was also boosted by an apparent easing of regulatory pressures for tech corporates, while excitement around Chinese firms’ advancements in AI and high-tech industries sparked a re-rating in internet and growth stocks. China’s Manufacturing Purchasing Managers’ Index (PMI) turned expansionary in February to 50.2 (vs 49.1 in January) as production resumed following the Spring Festival holidays.2 Meanwhile, inflation remains benign despite January’s consumer price index (CPI) rising 0.5% y/y, the fastest in five months.

Indian equities continued to pull back this month, declining 7.99% as some flows shifted to China and Hong Kong. Foreign institutional investors (FIIs) recorded outflows for the second consecutive month, with net outflows of USD 5.4 billion (vs outflow of USD 8.4 billion in January). Conversely, domestic inflows remained strong at USD 7.4 billion in February (vs inflows of USD 10 billion in January).3 On the macro front, GDP growth stayed robust, with India’s economy expanding 6.2% y/y in Q3FY25 (vs 5.6% y/y in the prior quarter), keeping India on track as one of the fastest-growing major markets. Consumer price inflation eased to 4.3% in January, a five-month low and back within range of the Reserve Bank of India’s (RBI) medium-term target. Easing price pressures allowed the RBI to cut its policy repo rate by 25 bps to 6.25% – the first rate cut in nearly 5 years.

MSCI Korea declined 0.21% in February as the KOSPI traded in a tight range. Tech sector sentiment was mixed: while Samsung suggested memory chip demand could recover from Q2 2025, US restrictions on AI chip exports to China created headwinds. Exports fell 13.5% y/y in January following December’s surge and recovered just 1.0% y/y in February.4 Although the Bank of Korea (BoK) unexpectedly held its policy rate at 3.00% in January to stem the Won’s slide, the central bank maintained an easing bias this month but signaled it would wait for political stability before further rate cuts. Despite these challenges, Korean equities found support from resilient domestic investors and earnings beats in select sectors.

Taiwanese equities saw a moderate pullback of 4.38% in February as investors locked in gains following solid gains in the prior months. The decline came as inflows into MediaTek were dwarfed by the aggressive selling in TSMC on tariff risks and headlines on a potential Intel partnership. Market sentiment was further dampened as Taiwan marginally lowered its 2025 GDP growth outlook to 3.14% (vs its November forecast of 3.29%) due to fears of new US tariffs under the Trump administration, which could disrupt Taiwan’s export-driven economy.5 On the positive side, manufacturing PMI improved by 0.4pts in February to 51.5 as productivity gains and stronger sales were cited as key factors leading to higher output volumes.

Within ASEAN, the Philippines and Singapore were the top performers, with equities returning 3.73% and 3.29%, respectively, in February. For the Philippines, the inflation outlook continues to improve, with headline inflation easing to 2.1% y/y in February (vs 2.9% in January). In Singapore, equities rallied after the Monetary Authority of Singapore (MAS) announced a slew of measures to reform and strengthen the local stock market. The announcements are part of a broader initiative to boost market liquidity and potentially reduce the market’s valuation discount versus regional peers like Australia and Japan. On the downside, Indonesia and Thailand were the worst performers this month, with equities down 15.85% and 8.59%, respectively. Heavy net outflows from both markets were likely driven by a combination of weak macro and earnings, while tariff uncertainty loomed alongside the shift in interest back to China. For Indonesia, investors are keenly watching the newly launched Danantara, a sovereign wealth fund receiving USD 20 billion in cash injections, as it aims to improve the management of state-owned enterprises (SOE).

Chinese equities have staged an impressive rally this year, surging nearly 13% year-to-date (YTD).6 The momentum has been particularly strong in large-cap tech names, with stocks like Tencent, Alibaba, and Xiaomi benefiting from heightened interest in China’s AI capabilities. Adding to the positive sentiment, President Xi’s private sector symposium with industry leaders in February (the first such meeting since 2018) signaled Beijing’s renewed commitment to supporting the private sector and advancing technological development. Notably, this positive momentum persisted even as geopolitical concerns over potential US tariffs loomed in the background. So how did we get the China rally right?

Since late 2024, we maintained that market fears over US-China trade tensions were overblown, anticipating a more moderate policy approach to tariffs than consensus expected. This view, combined with our recognition of extreme market pessimism and compelling valuations, led us to increase our China and Hong Kong allocation to over 40% by early 2025. Our focus on resilient businesses with proven execution capabilities (particularly companies expanding globally like PDD and Trip.com), alongside domestic leaders capturing market share from foreign competitors, has been well-rewarded as markets recalibrated to a more benign outlook. This positioning, coupled with our understanding that Chinese companies’ technological advancements and competitiveness were being undervalued, has played out well in the portfolio.

We believe there is still meaningful upside potential in Chinese equities. Firstly, valuations remain attractive, with major tech companies like BABA trading around 15x 1-year forward P/E even after the initial rally but still significantly below the multiples commanded by US tech leaders.7 This suggests room for further multiple expansion as confidence returns.

Secondly, consumption revival has yet to materialize but will serve as a critical leg of growth. Since the start of the pandemic in 2020, Chinese household bank deposits have surged by 86%, representing an extraordinary USD 9.8 trillion increase.8 To put this into perspective, these savings amount to more than double Japan’s GDP in 2023; money that is locked away in bank accounts as consumers lack the confidence to spend.9 However, what we’re hearing on the ground is that the property market in major cities is stabilizing, with the rate of decline in property prices levelling off. This stabilization, combined with the massive savings buffer, sets the stage for a potential consumption revival once confidence returns.

On the corporate side, we observed this positive shift in February when the Chinese government signaled strong support for the private sector to stimulate the economy. President Xi’s symposium reaffirmed the commitment to the private sector and marked a clear move away from the regulatory tightening cycle, thereby rebuilding investor confidence.

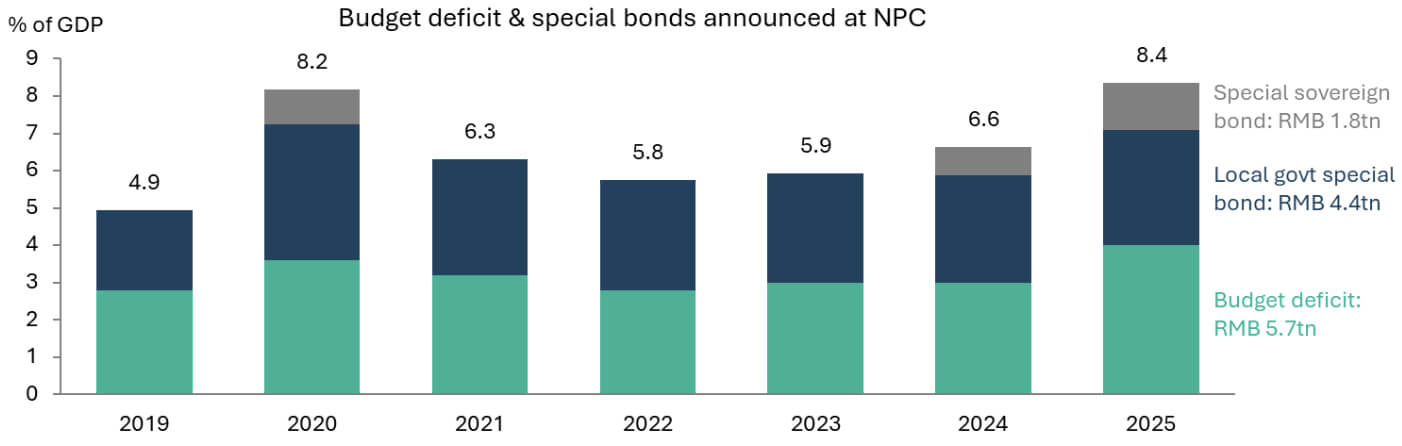

The recent National People’s Congress (NPC) meeting further reinforced Beijing’s commitment to growth. The government maintained its ambitious “around 5%” GDP target for 2025 while unveiling substantial stimulus measures, including an unprecedented 4% budget deficit (~RMB 5.7 trillion) and expanded special bond quotas totaling RMB 6.2 trillion. Key initiatives include doubling consumer subsidies to RMB 300 billion and a RMB 500 billion bank capital injection. Notably, these measures were planned before recent trade tensions escalated, suggesting Beijing has additional policy tools if needed. Thus, the shift to a “moderately loose” monetary stance since last December (the first since 2010), combined with the substantial fiscal firepower, should position China well to counter potential headwinds from higher US tariffs.

While we remain constructive on Chinese markets, we recognize the recovery will take time to broaden out. The initial rally has concentrated on AI and tech names, but we expect a wider market recovery as policy measures flow through the economy and private sector hiring picks up. With the market re-rating phase largely complete, we will be watching for an earnings revival phase in the coming quarters. As this transition unfolds, we may tactically take some profits and gradually rotate part of our exposure toward India around Q2.

The US faces mounting fiscal pressures. With a 6.4% deficit and interest payments of almost USD 900 billion in the fiscal year 2024, 18% of government revenues went into servicing debt.10 As US Treasury bond yields have climbed to ~4.3%, interest payments could consume well over 20% of annual tax receipts in the coming years.11 This unsustainable trajectory could lead to a debt trap. So it makes sense why the Department of Government Efficiency (DOGE) is now stepping in to cut excess spending. However, this process will lead to a drag on growth and consumer sentiment as adjustments are made.

These structural changes, while challenging, are necessary. We observed similar transformations in China over the past few years with the tightening of the tech and real estate sectors. In India, significant shifts occurred in 2016-2017 with demonetization and the implementation of the Goods and Services Tax (GST). Both countries experienced periods of uncertainty as their economies and markets adapted to these changes, but the benefits manifested in the subsequent years. A similar cycle is now unfolding in the US. If these issues are not addressed promptly, it could lead to more severe global repercussions, as bond yields are likely to spike further.

Our base case remains that the US is likely to achieve a soft landing, avoiding a recession. While consumer spending may moderate and corporate earnings growth slows, robust domestic capital expenditure should sustain some economic momentum. Despite elevated interest rates, we expect strong capital investments to continue, particularly in infrastructure, energy production, and innovative technologies like AI. However, the next 12-24 months represent an uncertainty corridor for the US economy. This raises the question: Where will investors focus their attention?

Market dynamics increasingly favor Asian markets as the narrative of US exceptionalism faces growing scrutiny. This shift illustrates a classic market principle – that prices respond not just to current conditions but to the rate of change in those conditions. During the Asian sell-off in November/December last year, investors remained fixated on US exceptionalism while overlooking attractive valuations and improving fundamentals in Asian. What many missed was that the US would need to address the structural challenges mentioned above before sustainable growth could resume.

The contrast with Asia is becoming more apparent. While the US grapples with fiscal tightening, governments across Asia are moving toward stimulus measures. This marks a significant turn from the past 3-4 years, when Asian consumers faced high inflation and a lack of meaningful government handouts. Many also worked in informal sectors that bore the brunt of COVID-19 disruptions. That challenging period is now behind us. Asian consumer balance sheets have strengthened, and inflation has come down to target range levels, setting the stage for a broad-based economic recovery.

An example is Sea Limited, which exemplifies this regional recovery story. Despite currency headwinds, the company delivered robust earnings in Q4 2024. Having successfully defended its market position through a period of strategic low-margin operations to ward off competitors like PDD and Douyin, Sea is now well positioned to expand its margins and accelerate growth initiatives to improve profitability.

Elsewhere, China, as we’ve already touched on, has clearly moved beyond the bottom. We don’t expect growth rates of 6-7% going forward, but 3-4% is still significant for the second-largest economy. In this more subdued growth environment, we are focusing on leading companies that are gaining domestic market share, as well as global champions in certain sectors like AI and autos. This also includes B2C platforms where there is further optionality to expand into overseas markets. For example, Trip.com is now one of the top online travel agency (OTA) players in the ASEAN region, gaining ground and even overtaking peers like Agoda and Booking.com in certain markets.

India appears to be approaching an inflection point, with sequential GDP improvements signaling the end of its recent mini downcycle. Manufacturing activity is notably accelerating, as evidenced by February 2025’s robust 6.6% surge in power demand – particularly impressive given it builds on a strong 7% growth base from the previous year.12 Power consumption, one of the more reliable indicators of industrial activity, suggests manufacturing facilities are meaningfully ramping up operations. From a portfolio perspective, our strategic focus on large caps has provided crucial downside protection during this transitional period. Looking ahead, we anticipate India’s recovery to gain momentum in the coming months, supported by accommodative monetary and fiscal policies bolstering domestic demand, and we will be positioning to increase our India exposure as these catalysts materialize.

In North Asia, we maintain strategic exposure to Korea through global tech leaders Samsung and SK Hynix, which also provides direct exposure to US and European tech spending cycles. While remaining underweight in Taiwan, we hold select positions in TSMC and AI beneficiaries, including MediaTek, focused on consumer AI applications, and Quanta, a growing player in AI server infrastructure manufacturing.

While still in its early stages, Asia’s recovery trajectory is becoming increasingly well-defined. Our conviction in the rotation of global capital toward Asian markets continues to build, particularly as other emerging markets, notably in Latin America, face growing headwinds. Asia’s distinct advantages in terms of policy flexibility, improving fundamentals, and attractive valuations position it as the standout destination within emerging markets.

In February, our Senior Investment Analyst, Marcus Chu, travelled across China to meet with corporates and industry experts and conduct comprehensive channel checks. Here are some of his observations from the ground:

Policy effectiveness and confidence showing early signs of improvement: Policy effectiveness has exceeded initial expectations, particularly in property and consumer sectors. The government’s targeted stimulus measures are yielding preliminary results, with property volumes and prices stabilizing in premium segments of tier-1 cities. The manufactured goods subsidy program has proven effective in supporting consumer sales. Multiple banks reported better-than-expected loan growth in early 2025, though retail loan quality deterioration remains a pressing concern. The modest improvement in confidence appears driven by multiple factors: the policy pivot from September 2024, DeepSeek AI developments, recent equity market rebounds, lower-than-anticipated tariff impacts, and cultural sector successes in movies and gaming. However, those we spoke with remained measured in their optimism, noting that similar sentiment upswings had previously led to false hopes.

Materials – Bearish demand outlook leads to focus on supply: Despite early-year performance exceeding forecasts, the consensus among industry experts points to a bearish demand outlook for the rest of the year. Meetings with management revealed concerns about sustained demand weakness, particularly in sectors like steel and solar materials.

In solar, the industry still faces significant headwinds, with experts anticipating that a turnaround is unlikely before 2025. This prolonged challenge underscores the need for companies to adapt strategically, focusing on cost management and exploring new markets to mitigate the impact of sluggish domestic demand.

However, in other sectors, like steel and cement, supply consolidation was a positive focal point. Marcus visited major steel producers like Baosteel, where discussions revealed ongoing industry consolidation efforts. While the government’s supply-side reform policies remain uncertain, the industry appears to be moving toward more disciplined production, potentially supporting better pricing power for leading players.

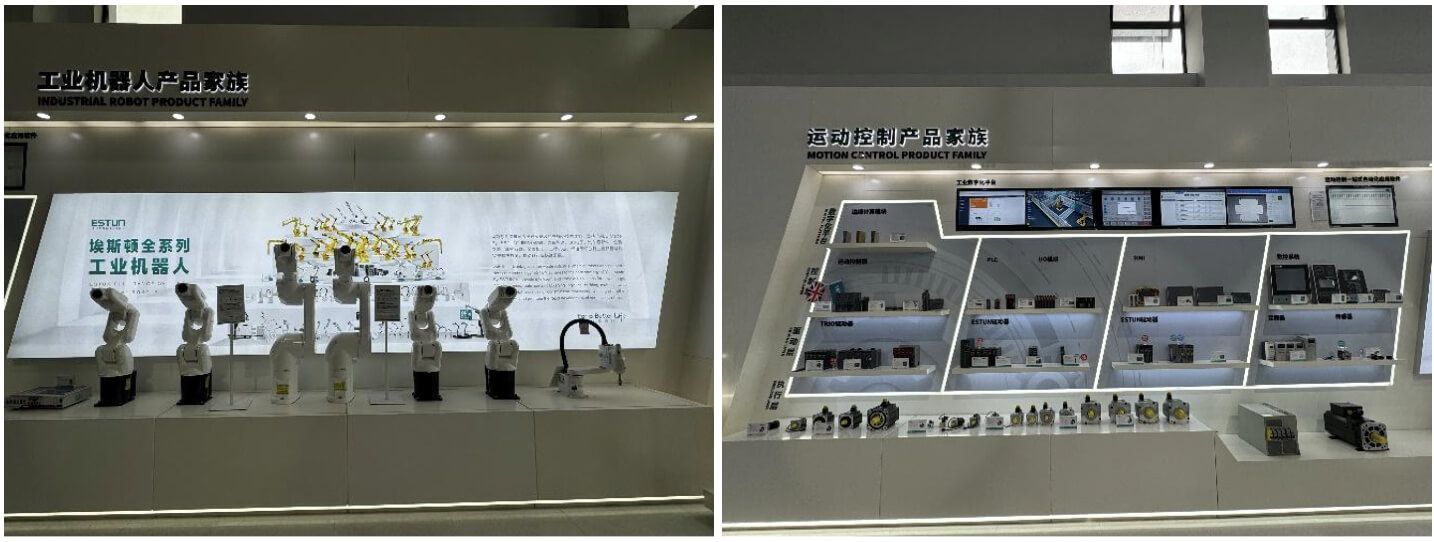

Industrial automation – Navigating competitive pressures: In a visit to Estun’s facilities, we gained valuable insights into China’s industrial automation sector. Estun, a leading Chinese industrial robotics manufacturer, has developed strong robotics capabilities, especially in automotive applications, where they serve industry giants like BYD and CATL. While touring their production lines, we observed their strategic pivot toward higher-value segments like spot welding, though our discussions with management revealed the challenges they face in matching the consistency and quality standards of international competitors.

The broader Chinese industrial automation landscape is at an interesting inflection point. While domestic competition remains intense and margin pressures persist, we believe a new phase of industry consolidation is emerging. Recent moves like Haier’s acquisition of Xinshida suggest larger industrial groups are positioning themselves in the automation space, potentially leading to a more competitive environment in the medium term. The winners will be those who can successfully navigate this consolidation while building sustainable competitive advantages, particularly in specialized applications like automotive and electronics manufacturing. For now, we will continue to watch this space.

For sophisticated investors only. For informational purposes only. The information presented in the material is not, and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

This material is prepared by Shikhara Investment Management LP (“Shikhara”). This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. Whereas Shikhara has, to the best of its endeavor, ensured that such, information is accurate, complete and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this material are prepared and maintained by Shikhara and has not been reviewed by the Securities and Exchange Commission of the United States.

The Fund managed by Shikhara may or may not hold all of, or some of the securities mentioned in the article.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom and the European Union and pending registration in the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom and the European Union and pending registration in the United States.