In our December 2024 healthcare article, we outlined the structural case for Asian healthcare as a compelling long-term investment opportunity. We highlighted how Asia, home to approximately 59% of the global population, continues to spend significantly less on healthcare as a percentage of GDP relative to developed markets, and argued that this gap would narrow as the region’s economies advance.1 Given this backdrop, we outlined five key investment themes in Asian healthcare: China’s manufacturing prowess in medical devices, India’s dominance in the US pharmaceuticals market, the scaling of Indian hospital networks, the rise of India and ASEAN as medical tourism hubs, and the emerging potential of GLP-1 obesity drugs across the region.

In this follow-up piece, we revisit and expand upon several of these themes with updated data and new developments. Three areas in particular have seen meaningful progression: 1) China’s pharmaceutical sector has accelerated its transition from generics to genuine innovation, with a surge in global out-licensing deals validating the quality of its drug pipeline; 2) India’s Contract Research, Development, and Manufacturing Organization (CRDMO) industry has reached an inflection point, benefiting from the “China+1” diversification trend and the global demand for GLP-1 drug manufacturing; and 3) India’s leading private hospital chains are embarking on their most aggressive capacity expansion in years, supported by robust cash flows and a persistent shortage of quality hospital beds across the country.

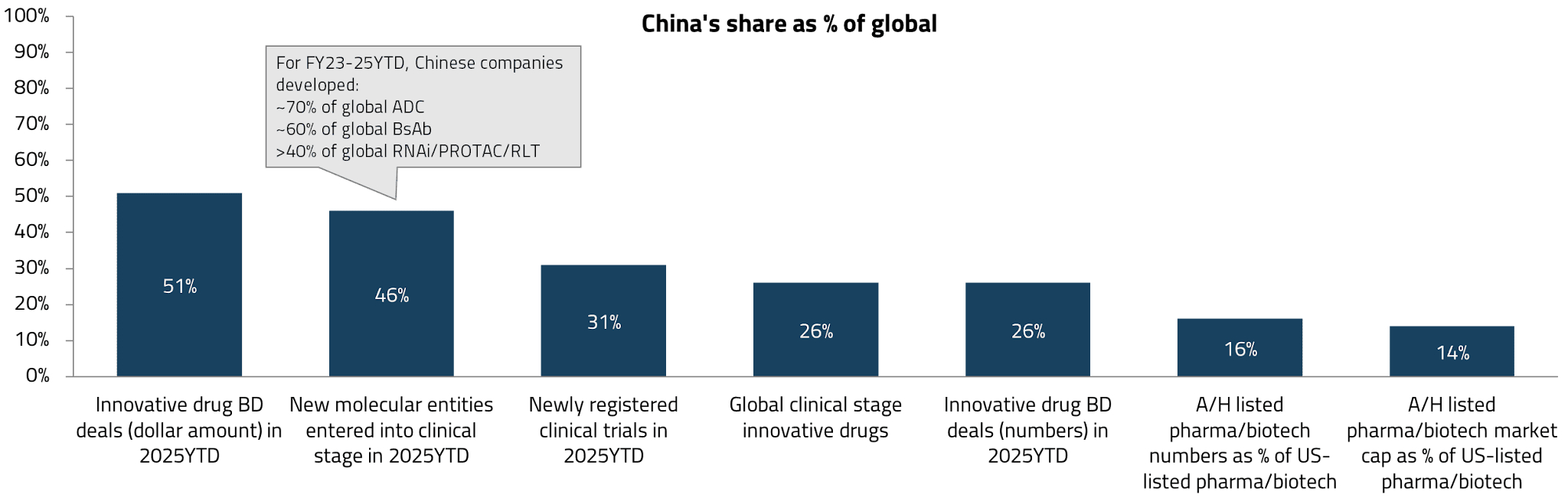

Global pharmaceutical companies are increasingly looking to China as a source of innovation. Over the past few years, China has materially increased its contribution to global drug development. Today, Chinese companies account for approximately one-quarter of all innovative drug candidates under active development (excluding those without clinical updates for three years).2 More strikingly, 46% of new molecular entities (NMEs) entering human trials in the first half of 2025 originated from China, up from just 17% a decade ago.3

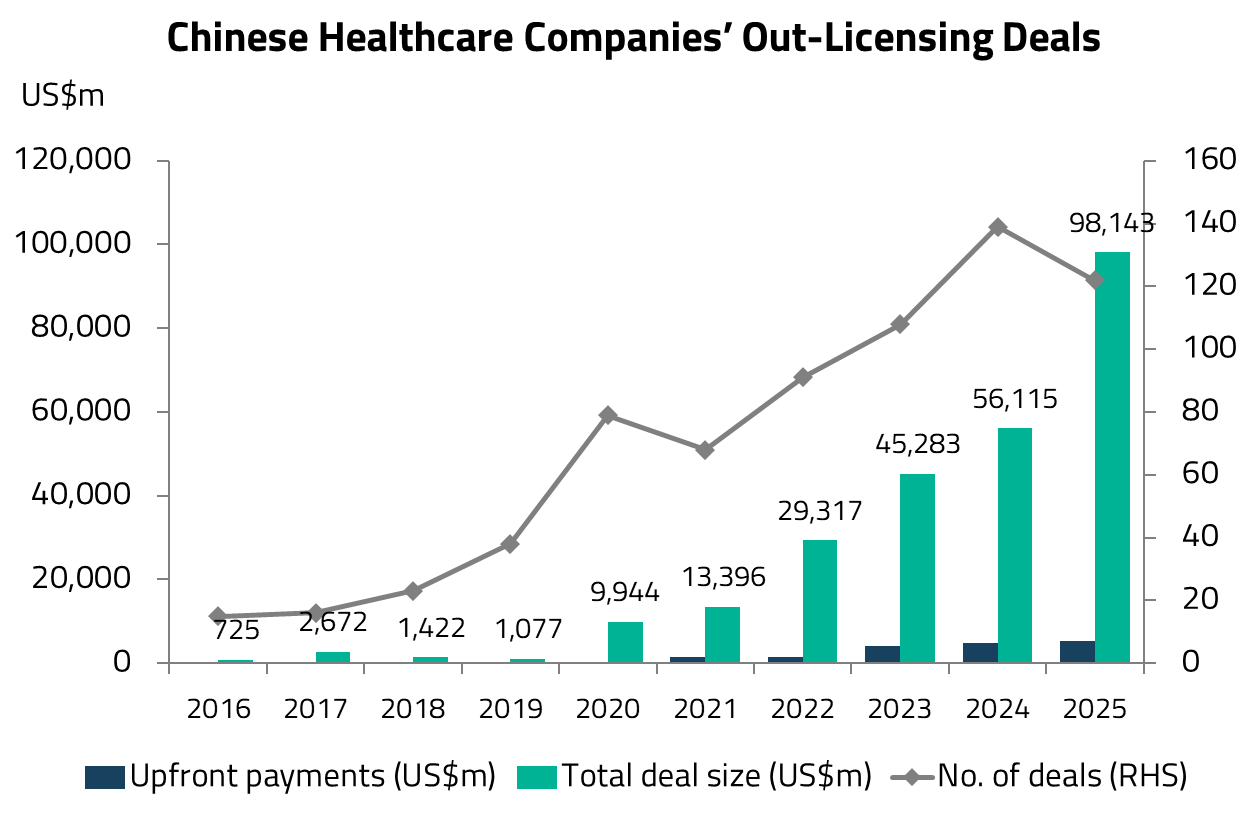

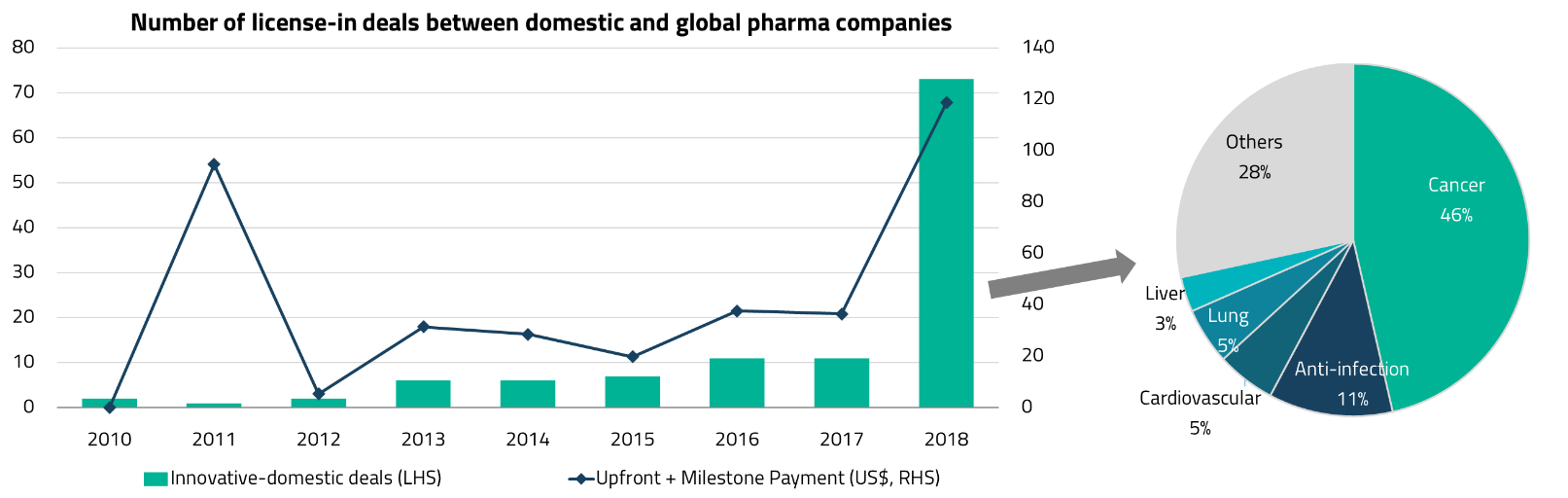

This growing recognition of China’s innovative capabilities has fueled a surge in out-licensing deals. Chinese companies now account for approximately 50% of global licensing deals by dollar value and 26% by volume.4 This is a striking shift from even five years ago, when China was primarily associated with low-cost generic drug manufacturing.

The transformation has been a decade in the making. Over the past ten years, China’s biopharmaceutical industry has fundamentally pivoted its strategic focus from generics to innovative drugs, driven by sweeping regulatory reforms, increased R&D investment, and the development of a deep talent pool in the life sciences.

While multinational pharmaceutical companies (MNCs) may have initially turned to China for cost-effective assets of comparable quality, we are now seeing a significant increase in China’s contribution to novel modalities. These include antibody-drug conjugates (ADCs), bispecific antibodies (BsAbs), RNA interference (RNAi) therapies, and proteolysis-targeting chimera (PROTAC) molecules – next-generation drug platforms that represent the frontier of pharmaceutical innovation.

Chinese companies now account for approximately 60% of global development activity in these novel modalities, compared to 35-40% in more established categories such as small molecules or monoclonal antibodies (mAbs).5 This suggests that China is carving out a particularly strong position in areas where engineering expertise (i.e., the ability to design, optimize, and manufacture complex biological constructs) matters more than entirely new biological target discovery.

We believe this engineering advantage will continue to compound. China benefits from cost-effective early-stage R&D infrastructure, and its companies are aggressively exploring novel drug component combinations, including bispecific ADCs (BsADCs), dual-payload ADCs, and multi-specific antibodies. As these modalities gain clinical validation, engagement with Chinese biotech assets is likely to become an essential component of global MNCs’ external sourcing and partnership strategies.

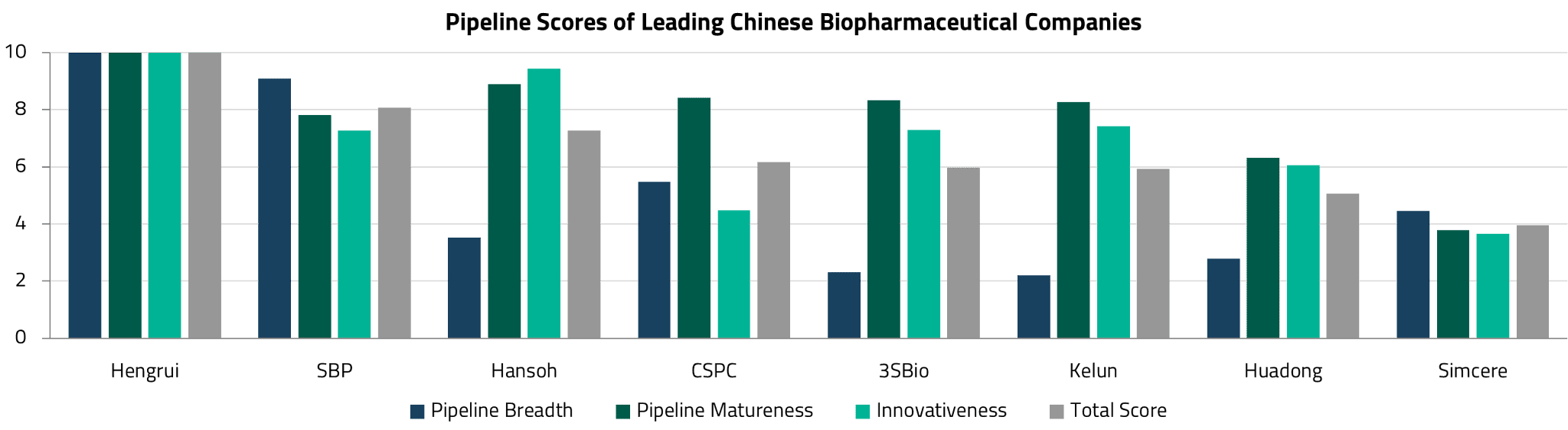

To assess which Chinese biopharma companies are best positioned, it is helpful to consider pipeline quality across multiple dimensions. UBS has developed a three-dimensional scorecard that evaluates leading companies on: (i) pipeline breadth, which measures the number of pipeline assets relative to the sector’s maximum; (ii) pipeline maturity, which assesses the proportion of assets in clinical or NDA-stage relative to the sector’s maximum; and (iii) innovativeness, which captures the share of the most advanced pipeline assets in four essential and promising technology platforms.

According to this framework, Jiangsu Hengrui Pharmaceuticals Co., Ltd. (Hengrui Medicine) ranks highest across all three dimensions, followed by Sino Biopharmaceutical (SBP) (ranked second in pipeline breadth), and Hansoh Pharmaceutical (ranked second in innovativeness). Below, we examine how two of these companies (Hansoh Pharma and Hengrui Medicine) have demonstrated both strong R&D capabilities and effective business development execution.

Hansoh Pharma exemplifies China’s pharmaceutical transformation. The company has successfully transitioned from a generics-focused business to an innovation-led platform. This is clearly visible in its revenue composition: innovative products are expected to contribute over 80% of total sales in 2025e, up from just 18% in 2020.6

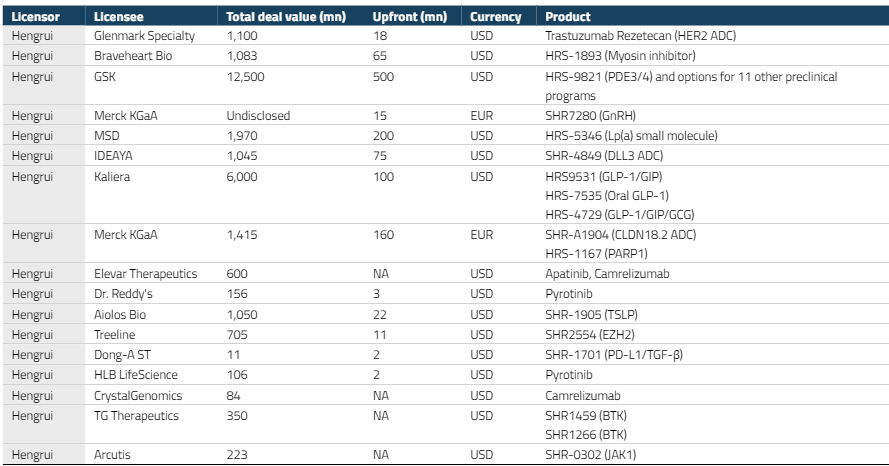

Hansoh has also successfully out-licensed its proprietary molecules to major global pharmaceutical companies. The company has completed five out-licensing deals over the past three years, spanning assets from preclinical through to late-stage development. Its most recent transaction was with Roche in October 2025, involving its CDH17 ADC molecule (currently in Phase 1 trials). The deal included a US$80 million upfront payment, with potential milestone payments of up to US$1.45 billion and tiered royalties on global net sales outside China.7

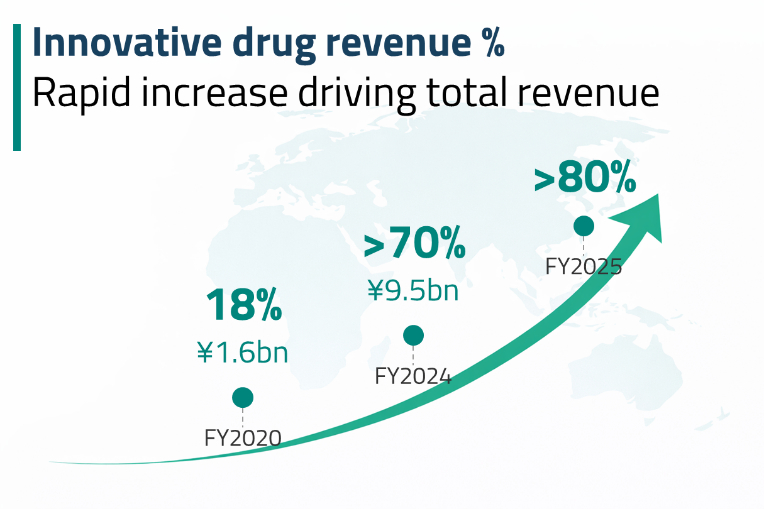

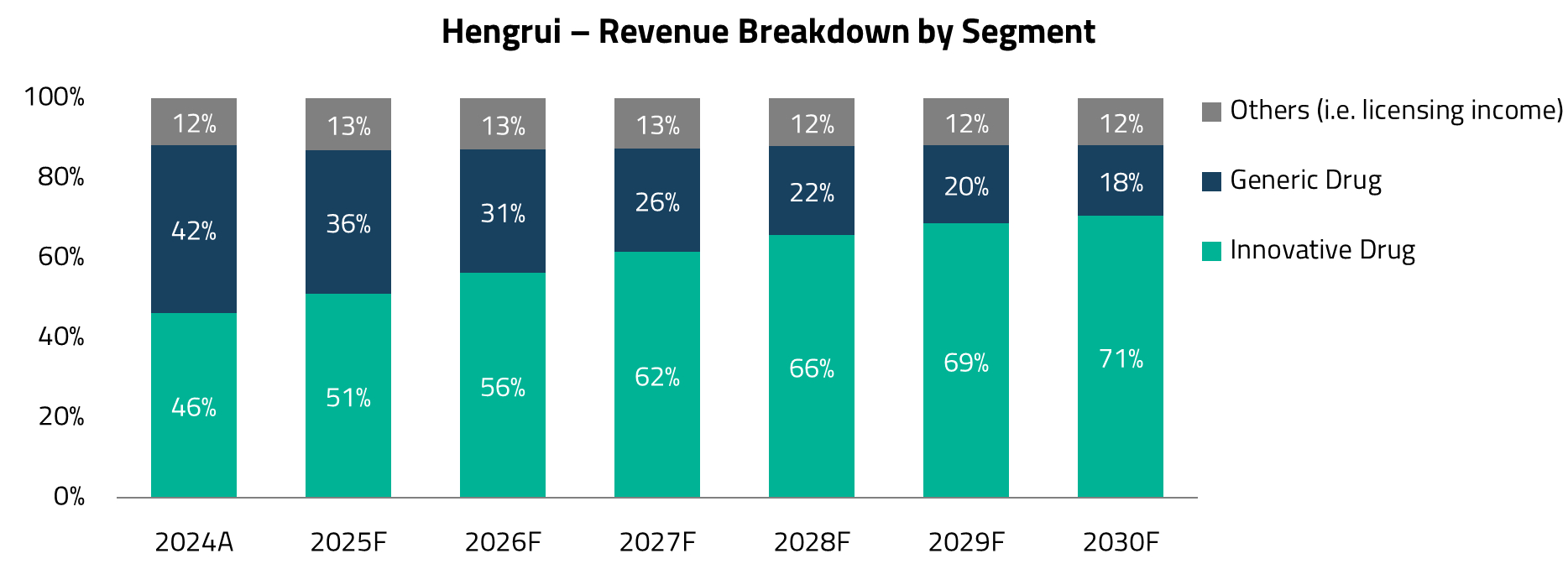

Jiangsu Hengrui Pharmaceuticals is one of the largest China-based companies engaged in drug research, development, production, and sales. The company focuses on oncology, metabolic and cardiovascular diseases, autoimmune and respiratory disorders, and other therapeutic areas. In 2024, innovative drugs accounted for 46% of its revenues, while generic drugs contributed 42%. According to Macquarie Research, by 2030, over 70% of Hengrui’s revenues are expected to come from innovative drugs, with the generics segment likely to shrink to approximately 18% of total revenues.8

Hengrui’s key differentiator is the breadth and depth of its pipeline. The company boasts one of the most comprehensive drug development pipelines among Chinese pharmaceutical companies, spanning multiple therapeutic areas including oncology, metabolic disorders, respiratory diseases, ophthalmology, nephrology, and cardiovascular diseases. This diversification reduces the risk inherent in drug development and positions Hengrui to capture opportunities across multiple disease categories.

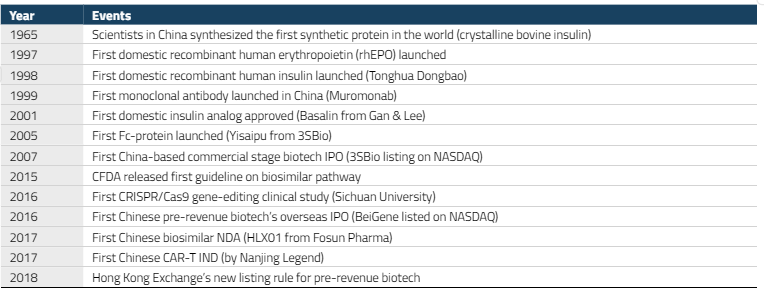

While we are witnessing the success of China’s biotech sector today, this has been the result of steady and deliberate policy developments, coupled with substantial private investment over the last 10 years.

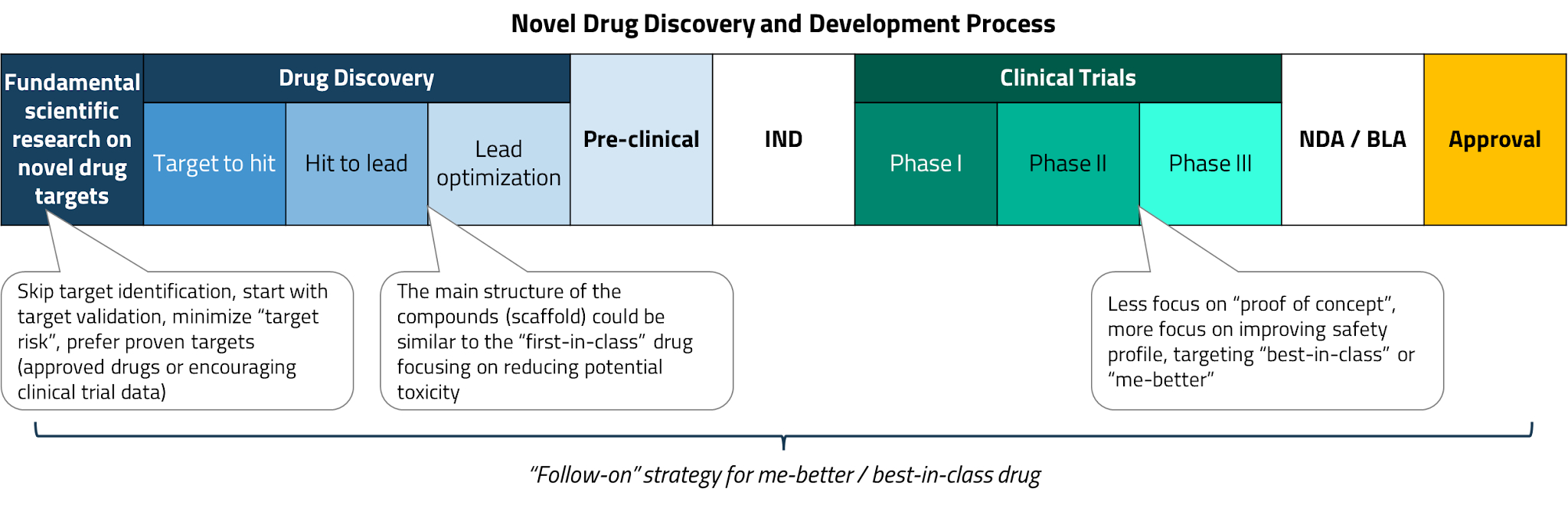

In the early stages, Chinese pharmaceutical and biotech companies primarily pursued a “fast follow-on” strategy. Rather than investing heavily in new target identification or proof-of-concept research, these companies focused on improving the safety and efficacy profiles of existing leading drugs – an approach often referred to as developing “me-better” drugs. Early successes in this category included the launch of domestically developed PD-1 inhibitors (a class of cancer immunotherapy) and third-generation tyrosine kinase inhibitors (TKIs), among others.

A key regulatory milestone came in 2015, when China’s Food and Drug Administration (CFDA) issued its first guidelines for a biosimilar approval pathway. By 2017, the first domestically developed biosimilar had been approved. A biosimilar is a near-identical copy of a biological drug whose original patent has expired, analogous to generics in the small-molecule drug space.

The year 2018 proved to be a breakthrough for China’s biotech sector. The Hong Kong Stock Exchange introduced new listing rules (Chapter 18A) that allowed pre-revenue biotechnology companies to list for the first time, providing a critical funding channel for the sector. The same year also saw a significant jump in licensing deals between global and domestic pharmaceutical companies, as MNCs began to take notice of the quality of Chinese drug candidates.

The speed of this transformation is remarkable. In less than a decade, China’s pharmaceutical industry has evolved from a predominantly generics-focused market into a genuine innovation engine. This trajectory mirrors China’s track record in other industries (e.g., from electric vehicles to consumer electronics), where the country has rapidly moved from low-cost manufacturing to global technology leadership.

For investors, the implication is clear: China’s biotech and pharmaceutical sector is no longer just a source of cheap manufacturing capacity, but an increasingly important source of proprietary innovation that global pharmaceutical companies cannot afford to ignore.

India’s Contract Research, Development, and Manufacturing Organization (CRDMO) industry is at an inflection point. For those unfamiliar with this space, CRDMOs are specialized companies that provide outsourced R&D, clinical development, and manufacturing services to pharmaceutical companies. Rather than building their own manufacturing facilities, global drug makers increasingly rely on CRDMOs to handle complex chemistry, formulation, and large-scale production, allowing them to focus on drug discovery and commercialization.

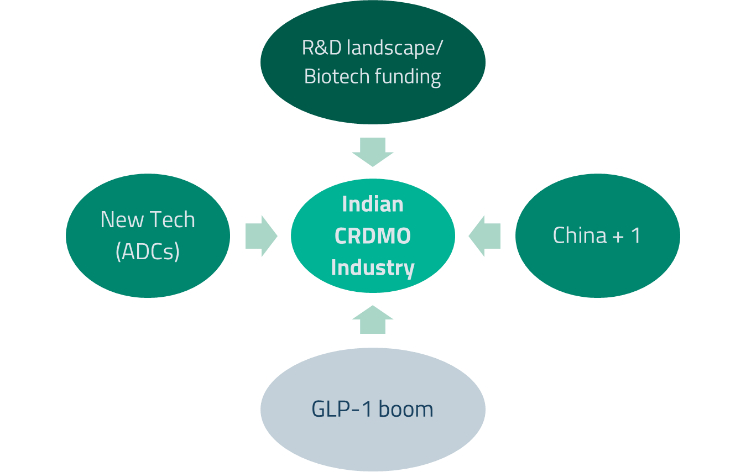

Four key structural drivers are converging to propel India’s CRDMO sector: 1) the “China+1” strategy, whereby US and European pharmaceutical companies are diversifying their supply chains away from over-reliance on China; 2) the explosive growth of GLP-1 weight-loss and Type 2 diabetes drugs, which require significant new manufacturing capacity; 3) the emergence of new drug modalities such as antibody-drug conjugates (ADCs), which demand specialized manufacturing capabilities; and 4) a favorable global R&D environment with improving biotech funding.

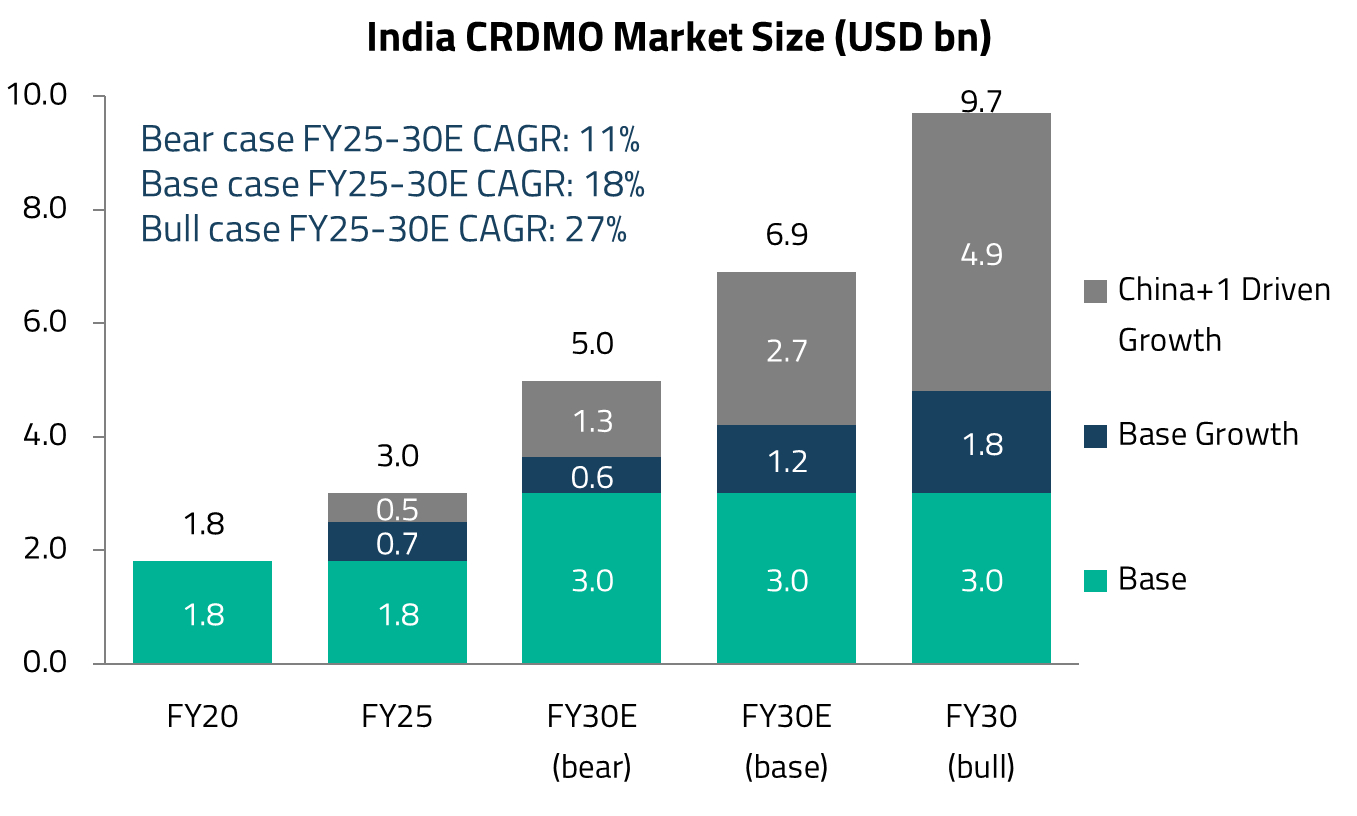

India’s CRDMO industry has undergone a remarkable transformation. Until a few years ago, Indian contract manufacturers were largely perceived as quasi-chemical firms offering basic synthesis services. Today, they have evolved into strategic partners for global pharmaceutical innovators, earning a place in the global spotlight. The industry’s combined market capitalization now stands at approximately US$40-50 billion, comparable to global CRDMO peers.9

In revenue terms, India’s CRDMO sector is a US$3 billion industry, having grown at a 14% compound annual growth rate (CAGR) over the past five years.10 However, growth has not been uniform, reflecting the impact of COVID-related opportunities and the subsequent normalization. Looking ahead, Jefferies Research expects the sector to grow at an 18% CAGR during FY25-30E, supported by strong pipeline visibility, diversification by major pharmaceutical companies away from China, and demand related to GLP-1/GIP weight-loss and diabetes drugs.11

US pharmaceutical companies have historically relied heavily on Chinese CRDMOs such as Wuxi for outsourced R&D and manufacturing. However, rising geopolitical tensions between the US and China, including proposed legislation targeting certain Chinese biotechnology companies, have prompted a structural shift towards alternative suppliers. Indian CRDMOs, with their established small-molecule capabilities and proven track record, are well-positioned to capture this opportunity. Jefferies Research estimates the China+1 opportunity for Indian firms at approximately US$700 million per year in the base case.12

Indian CRDMO companies have also matured beyond their nascent stage. Many firms are now well-capitalized or have access to capital markets at will, enabling them to invest aggressively in moving up the capability curve. This includes entering new drug modalities and adding complex development and manufacturing capabilities that were previously the preserve of Chinese and Western CRDMOs.

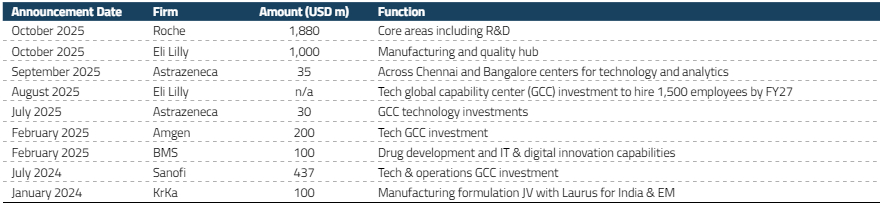

Major global pharmaceutical companies are backing India’s CRDMO potential with substantial investments. Eli Lilly has announced plans to invest more than US$1 billion to build contract manufacturing plants and a quality assurance center in Hyderabad.13 This initiative is reportedly part of a broader global expansion strategy aimed at enhancing manufacturing resilience and diversifying supply chains.

Additionally, Roche has committed US$1.9 billion to India over five years under the European Free Trade Association (EFTA) trade agreement.14 We expect these investments to further strengthen India’s growing CRDMO presence, driving incremental growth in the sector over the next seven years and signaling confidence from some of the world’s largest drug companies in India’s manufacturing capabilities.

The next major growth catalyst for Indian CRDMOs is the rapidly expanding market for GLP-1 receptor agonists – a class of drugs that has transformed the treatment of both Type 2 diabetes and obesity. GLP-1 drugs work by mimicking a natural hormone that regulates blood sugar and appetite and have demonstrated significant weight loss in clinical trials. Currently, there are over 170 such drugs in development globally, many in advanced trial stages, dominated by GLP-1 and emerging amylin-based therapies.15

As the market evolves from current leading products (semaglutide-based drugs such as Ozempic and Wegovy) to next-generation treatments like tirzepatide and orforglipron, Indian CRDMOs stand to benefit significantly. These companies are particularly well-positioned to manufacture the chemical intermediates and active pharmaceutical ingredients (APIs) required for this drug class, leveraging their existing strengths in peptide chemistry.

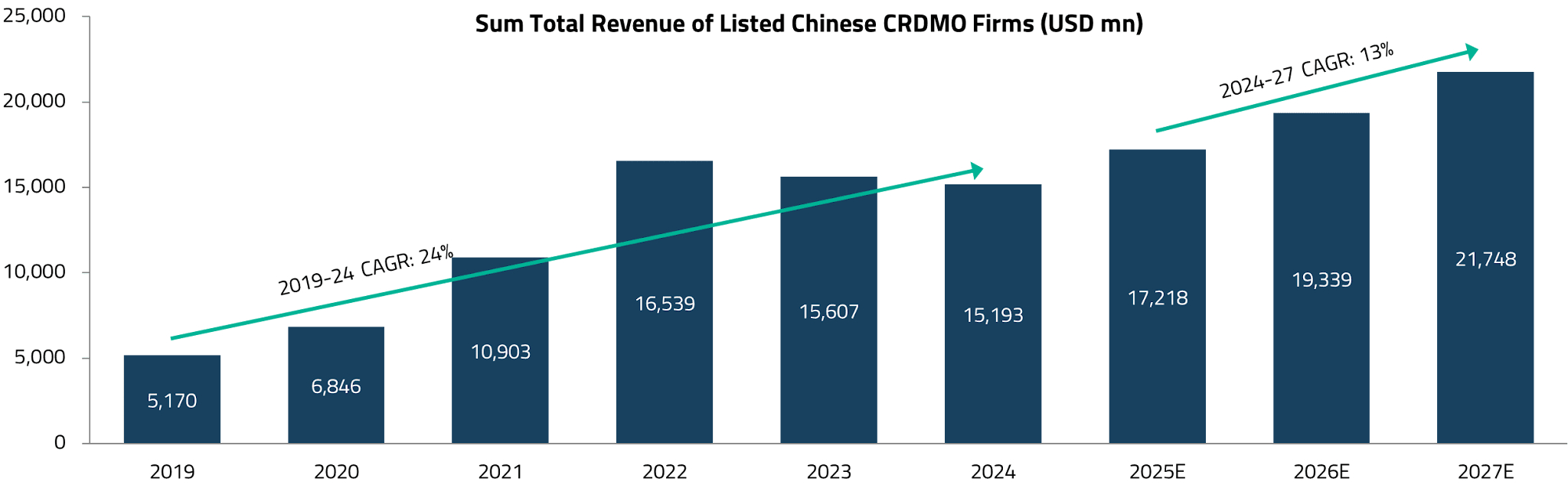

China’s CRDMO market, valued at approximately US$18.7 billion, offers a useful benchmark for understanding India’s growth trajectory.16Approximately 78% of China’s CRDMO revenue is derived from CRO/CDMO services related to small molecules, which is the most relevant segment for Indian players looking to benefit from the China+1 shift.17

The US is the dominant revenue source for nearly all major Chinese CRDMO companies, with average exposure of approximately 50%, rising to 60% on a weighted-average basis by sales.18 Following the US, the next two critical regions are China’s domestic market (driven by growing pharma R&D and innovation) and Europe. Given the heightened geopolitical tensions and the substantial reliance of Chinese CRDMOs on US revenue, geographic diversification by US pharmaceutical companies is poised to become a key structural catalyst benefiting Indian CRDMOs.

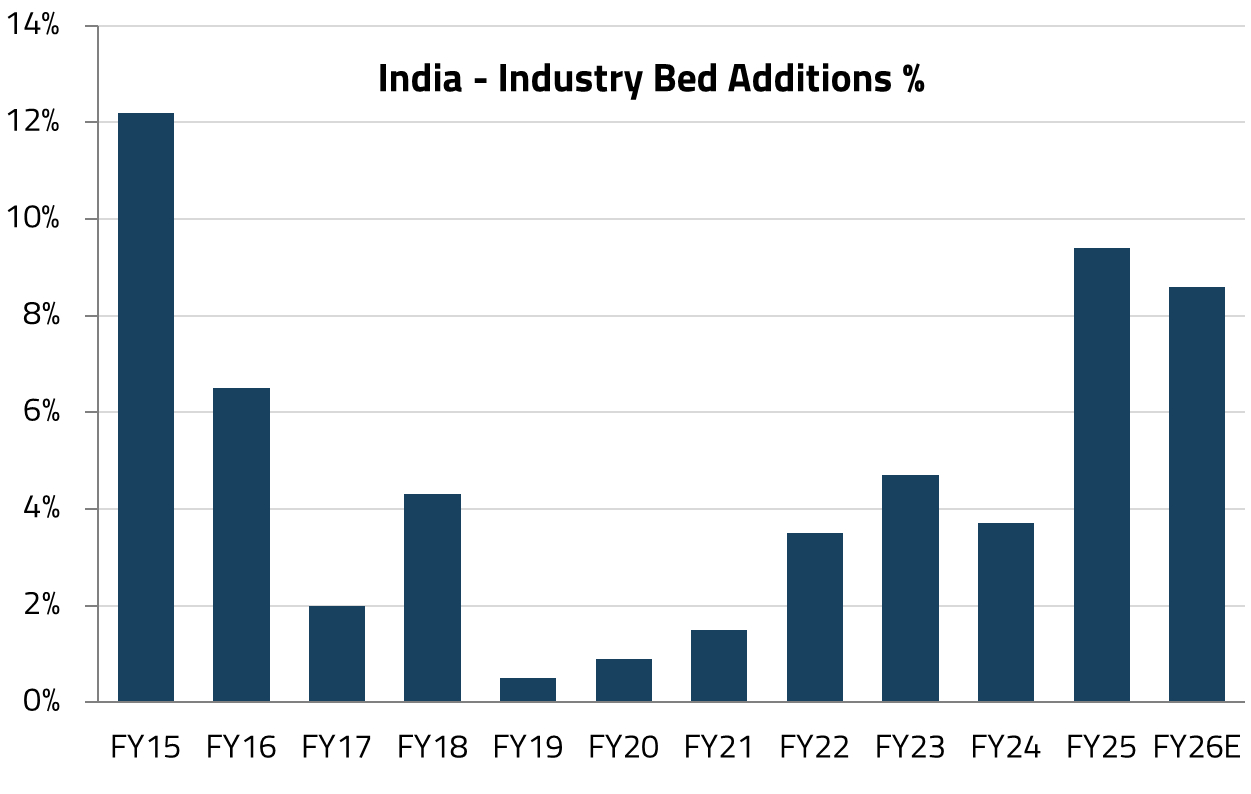

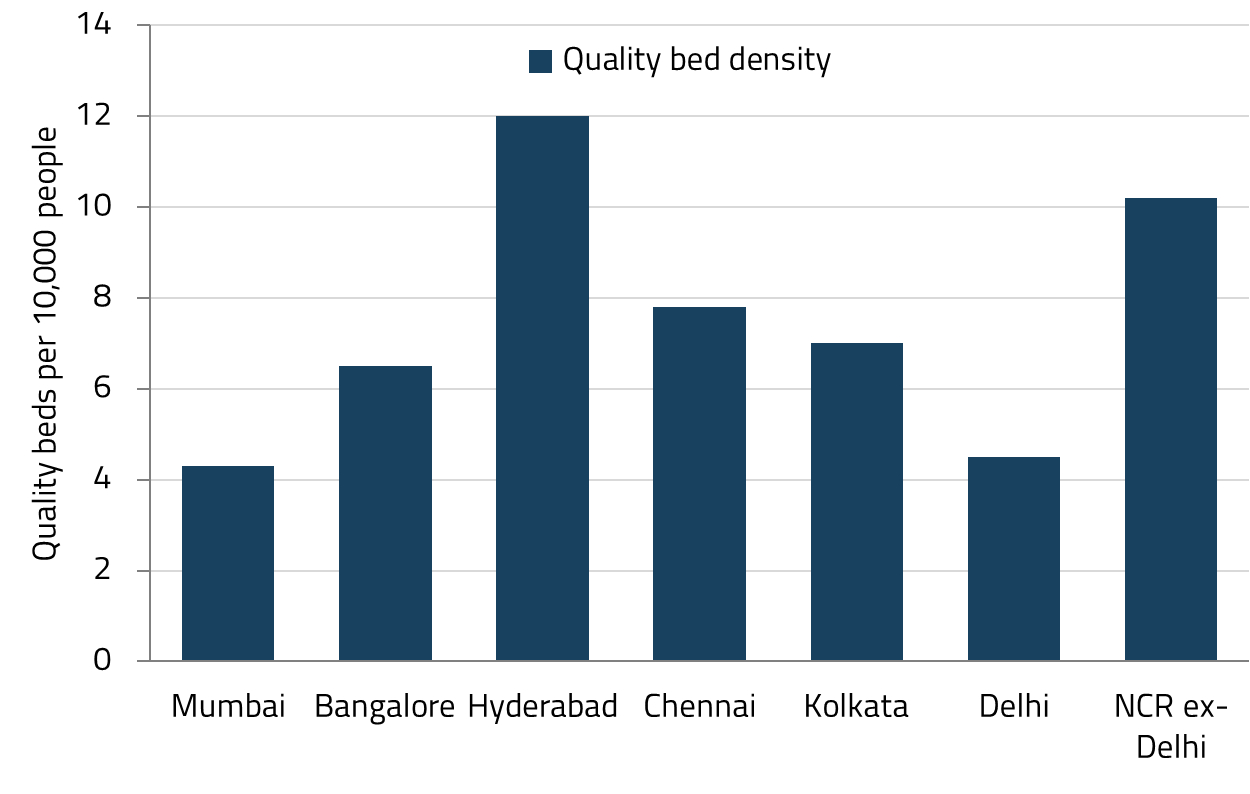

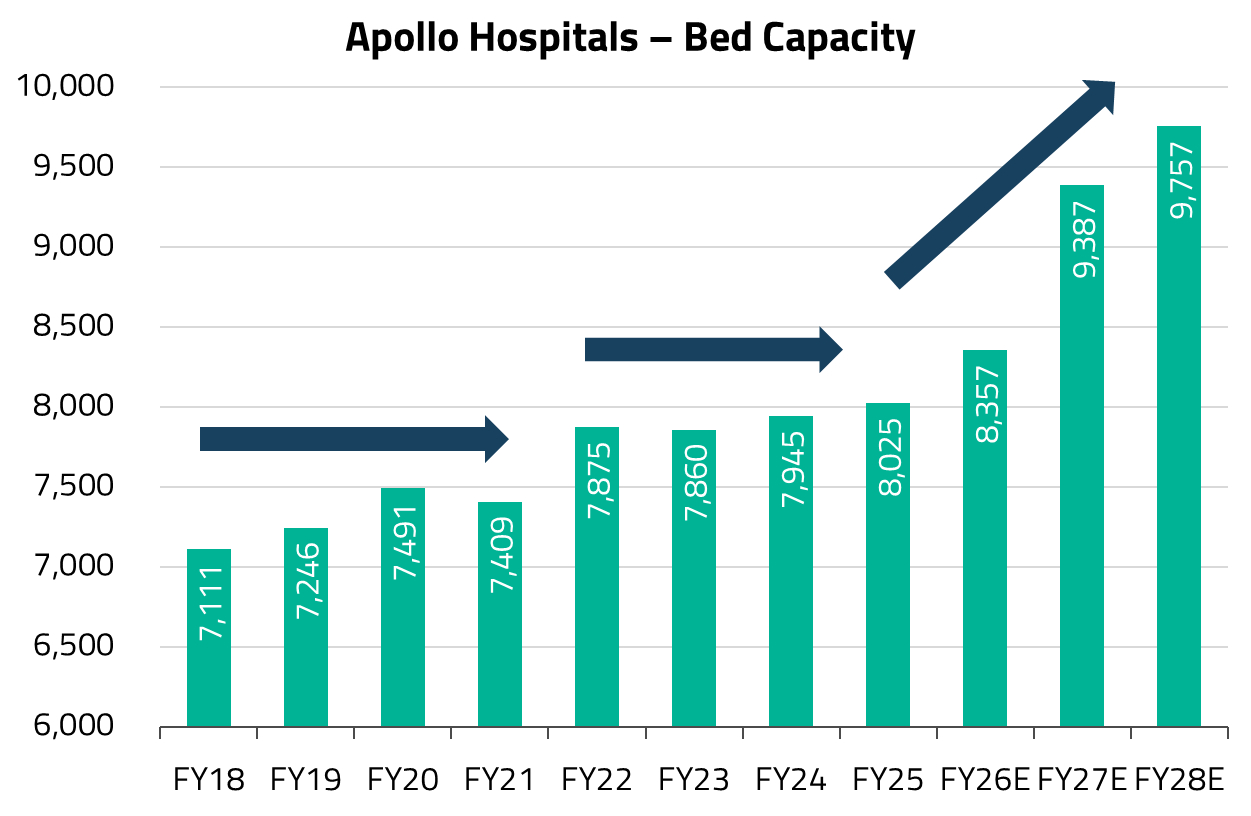

India’s leading listed private hospital chains are embarking on their most significant capacity expansion in years. The top listed players are set to add more than 17,000 beds (equivalent to over 40% of existing quality bed capacity) across India’s top six metro regions by FY30.19

For 3-4 years following the onset of COVID, India’s hospital industry was in a phase of consolidation. Hospital management teams focused on streamlining operations, improving efficiency, and navigating the challenges presented by the pandemic. This period of operational discipline led to significant improvements in key financial metrics, including operating margins, return on capital employed (RoCE), and leverage profiles, resulting in a substantial re-rating of hospital stocks over the past 2-3 years.

The key investor debate today centers on the risk of oversupply. Specifically, whether the aggressive bed additions could lead to cannibalization of existing hospital networks and slower ramp-up at newer facilities, creating near-term earnings headwinds.

We believe this expansion cycle is different from previous ones. Hospitals have found ways to add meaningful capacity without significantly eroding operating metrics. Several factors underpin our confidence. First, there is genuine demand: most micro-markets in India’s top six metro regions (excluding Hyderabad) face an acute shortage of quality hospital beds, meaning the demand-supply gap remains substantial. Second, talent availability in new micro-markets has improved, reducing one of the historical constraints on expansion. Third, recent upward revisions to the Central Government Health Scheme (CGHS) reimbursement rates, along with public sector unit (PSU) rate hikes approximately two years ago, have improved the economics of government-scheme patients (historically a lower-margin segment), while also signaling the government’s acknowledgement that medical inflation is a reality.

The on-the-ground reality reinforces the data. Our CIO, Rahul Chadha, recently opted to have dental work done in India rather than the US. In the latter, the estimated cost for a root canal, extraction, and new cap was substantial and not covered even under a premium “Gold” healthcare plan. In India, the same procedures were completed across three to four visits at a fraction of the US estimate, in an upmarket dental clinic housed in a private hospital in Gurgaon that delivered what he described as priority-level care. What struck him most, however, was not the cost savings but the demand. Despite the wave of new hospitals opening across Gurgaon, the facility was completely packed – weekdays, weekends, mornings, and evenings alike. As Rahul puts it, “This is what India’s shopping malls looked like 20 years ago when the malls were full of people.” Nowadays, everyone shops online, but demand for hospital and clinic services has risen, thanks to improved insurance coverage, greater affordability, and greater health awareness amid the rise of chronic diseases. This is quality, affordable healthcare meeting rapidly growing demand.

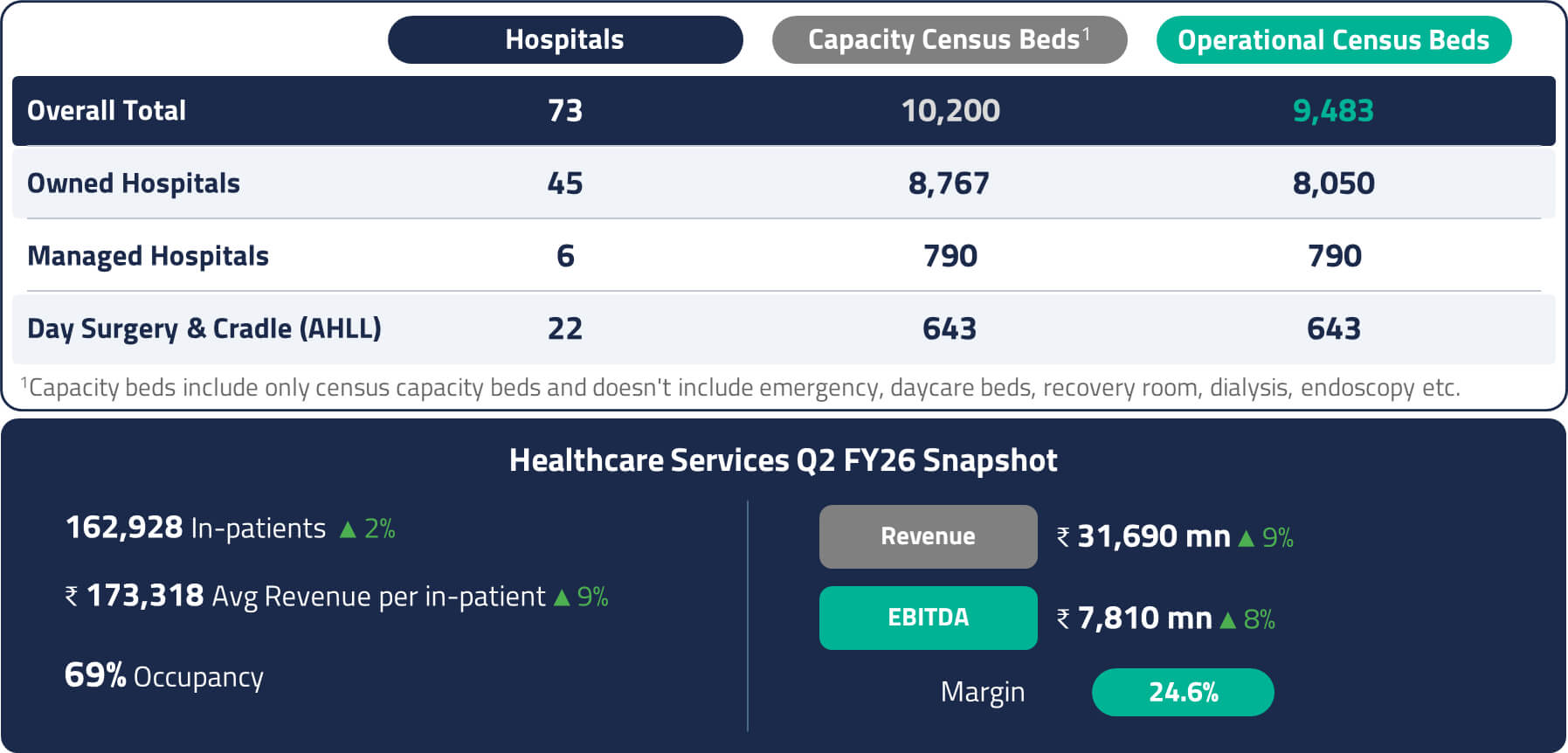

Apollo Hospitals is an integrated healthcare services provider with offerings spanning hospitals, retail pharmacies, health insurance, clinics, and digital health. It is one of the largest private hospital networks in India, with a pan-India presence.20

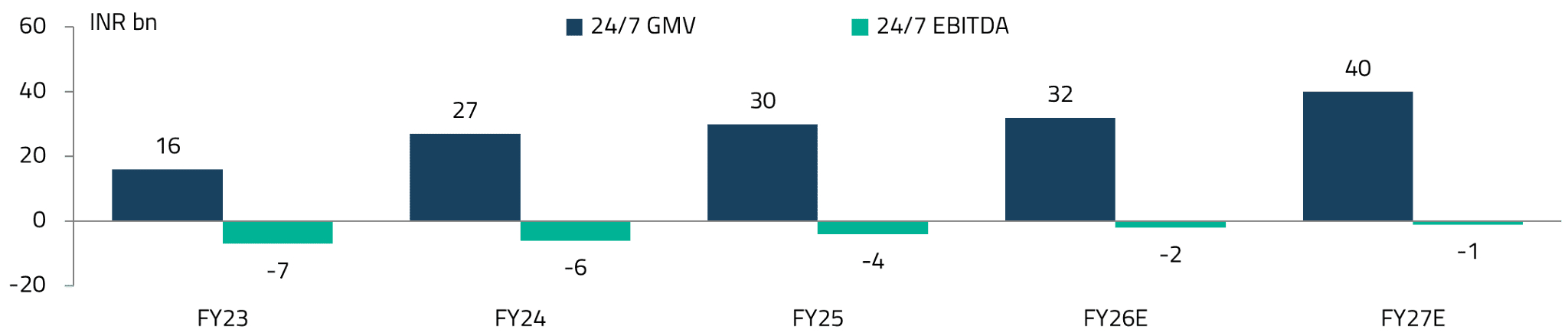

Over the past few years, Apollo has successfully built India’s largest omni-channel healthcare platform. On the offline side, the company operates over 6,900 pharmacy stores across the country.21 On the digital side, its Apollo 24/7 platform has amassed 44 million registered users and approximately 950,000 daily active users (DAUs), creating a significant digital health ecosystem.22

The gross merchandise value (GMV) for Apollo 24/7 has grown sharply over the past few years. The platform is also expected to reach EBITDA breakeven by FY27, a significant milestone in demonstrating the viability of digital health platforms in India.23

A key debate for Apollo 24/7 is whether it can continue to scale and succeed in shifting pharmacy sales from offline to online channels. We believe the answer is yes and point to China’s experience as an encouraging precedent.

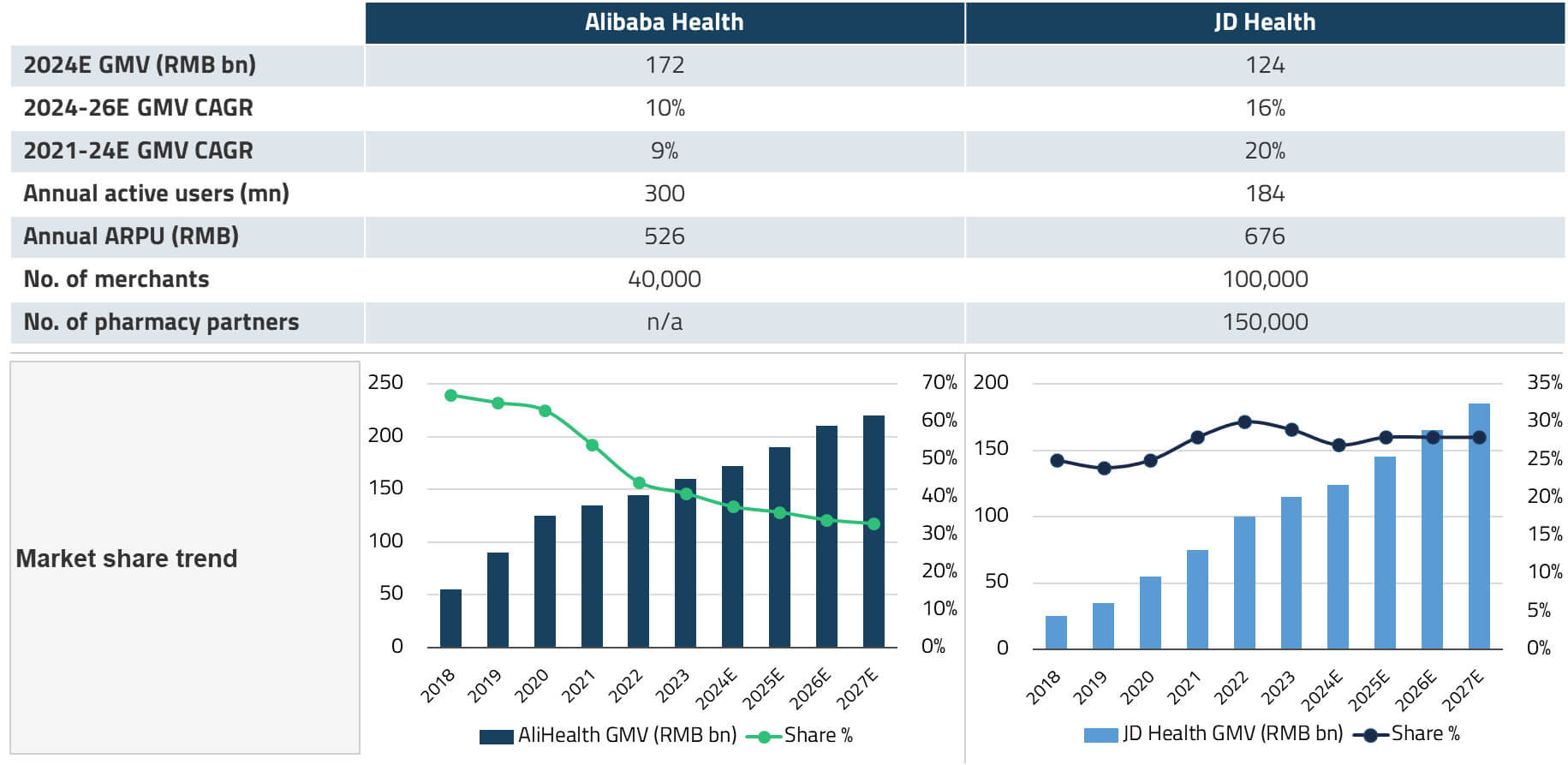

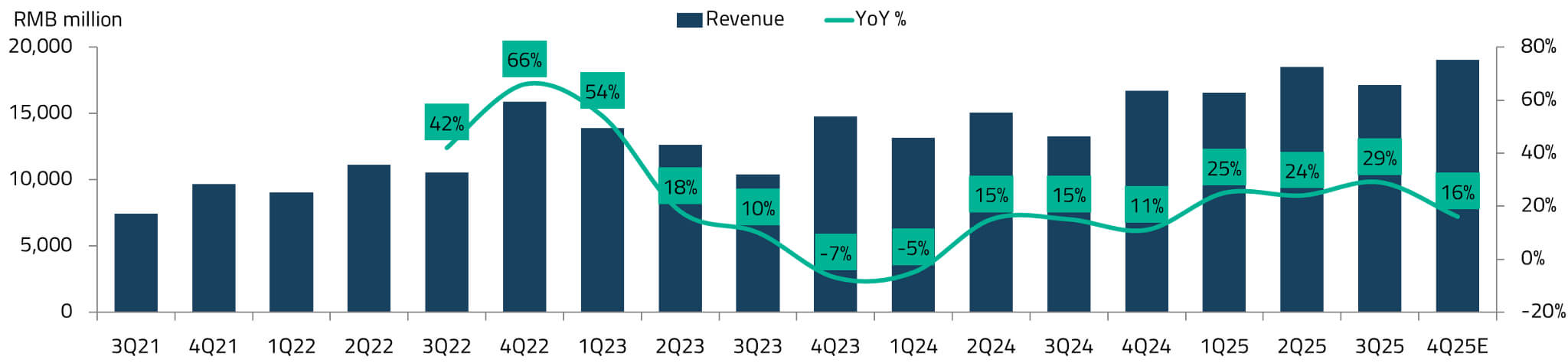

China’s online pharmacy platform industry is relatively concentrated, with Alibaba Health and JD Health together commanding an estimated 65-70% market share.24 JD Health’s revenue has grown at approximately 27% per quarter from Q3 2021 to Q3 2025, even though online penetration of drug sales in China stands at only 8%.25 This penetration rate is expected to increase over the coming years, driven by the outflow of prescriptions from hospital pharmacies and the extension of reimbursement coverage to prescription drugs sold online.

For India, which has an even lower base of online pharmacy penetration and a significantly larger unserved population, the long-term opportunity for platforms like Apollo 24/7 could be substantial. Apollo’s key advantage lies in its integrated model: the combination of physical hospitals, a nationwide pharmacy network, and a digital platform creates a flywheel effect where each channel reinforces the others.

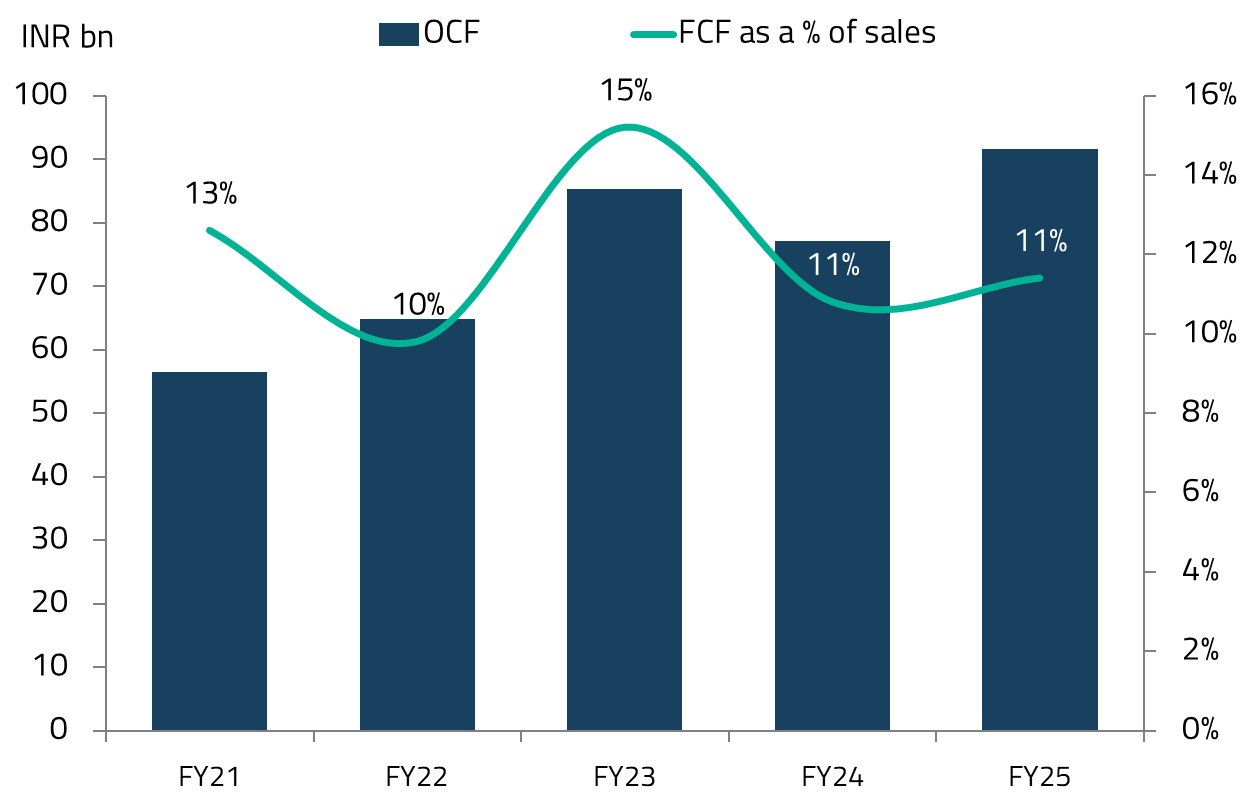

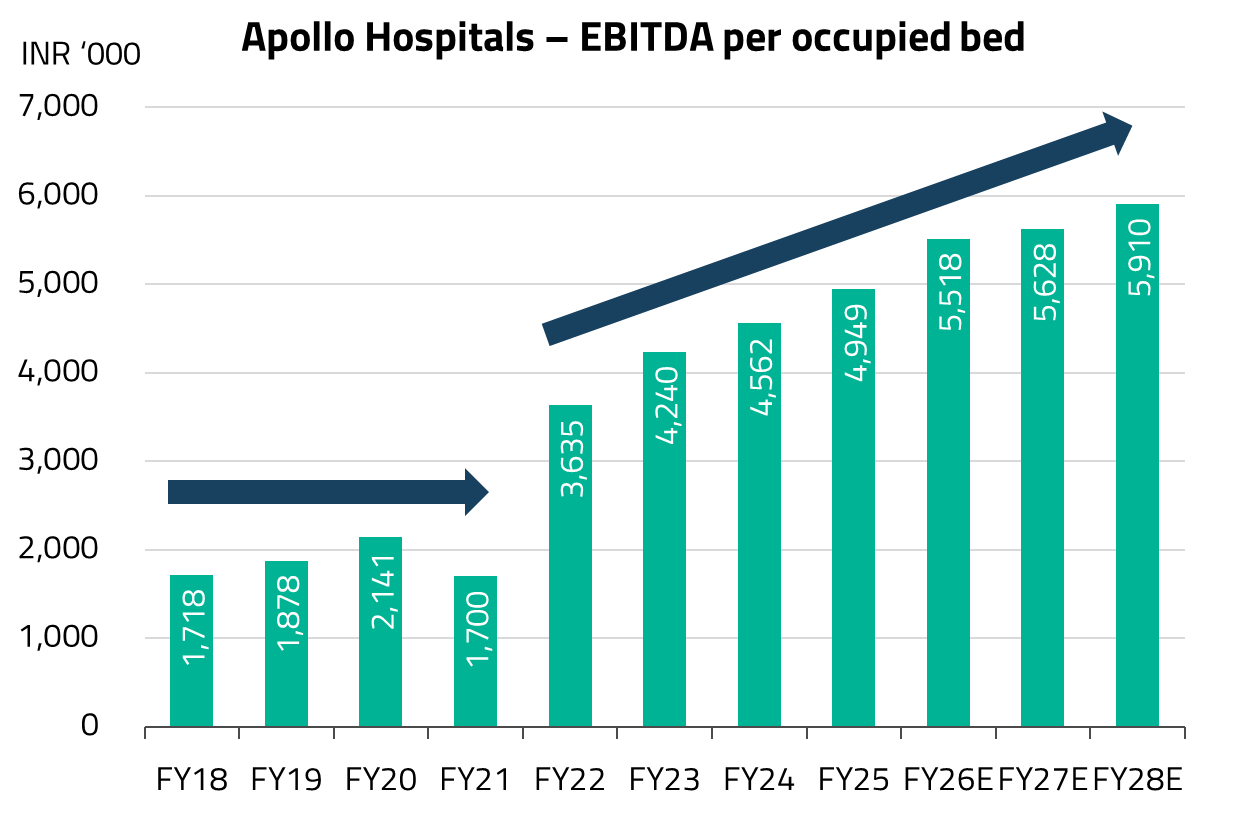

Apollo Hospitals has been a preferred hospital company since the pandemic, while it was at deeply discounted valuations. At the time, the market was understandably focused on the near-term issues, while elective surgeries fell sharply, dragging down revenue per patient, even as operating costs remained largely fixed. Apollo Hospitals was emerging from a period of stagnant bed capacity since approximately 2017. What the market underestimated, in our view, was that Apollo had used the downturn to run a leaner cost base, and that the pent-up demand for deferred elective surgeries was enormous. We recognized that the subsequent years would benefit from improvements in per-bed economics as well as a gradual increase in overall bed capacity.

As the pandemic receded, that is exactly what played out. Several factors drove Apollo’s strong performance during this period. The pandemic triggered a “flight to quality,” as patients increasingly preferred higher-quality hospitals with better infection control protocols, accelerating a shift from unorganized to organized hospital chains. Simultaneously, heightened health awareness drove a significant uptick in health insurance penetration, further supporting the move to branded hospitals as patients’ ability to pay for quality healthcare improved. An “up-trading” trend also emerged, whereby patients with improved affordability opted for better facilities and premium services, driving strong growth in average revenue per occupied bed (ARPOB). For Apollo specifically, a period of consolidation in bed capacity from 2022 onwards led to better asset utilization, improving margins and returns. Revenue intensity surged as patients returned for deferred procedures, but Apollo’s lean cost base barely moved. With the same number of beds running at progressively higher occupancy, margins expanded significantly and profit growth compounded over three to four years, without any aggressive capacity additions diluting the returns.

Today, that chapter is maturing – occupancy levels across Apollo’s network have largely normalized, and the company is entering its next phase of growth of adding more beds. The focus is on brownfield expansion, adding capacity adjacent to or within existing hospital campuses, which benefits from established brand presence and patient referral networks, allowing new beds to ramp up faster than greenfield sites. We continue to favor the company as this next leg of growth unfolds.

For decades, Narayana Hrudayalaya (NARH) has stood apart in Indian healthcare by challenging a deeply held assumption: that high-quality medical care must be expensive. Built on scale, specialization, and process discipline, NARH’s hospitals consistently deliver complex procedures at costs far below global benchmarks, without compromising clinical outcomes. While this model is well understood in India, its true validation came thousands of miles away, in the Caribbean.

Health City Cayman Islands: From experiment to proof of concept

Health City Cayman Islands was NARH’s boldest experiment. When operations began in 2014, expectations were high: medical tourism from the US and Latin America would power volumes, and Cayman would become a regional healthcare hub. Reality proved harsher. For the first five years, volumes disappointed, fixed costs were heavy, and returns lagged. The turnaround only came when NARH adapted its model to local realities rather than imported assumptions.

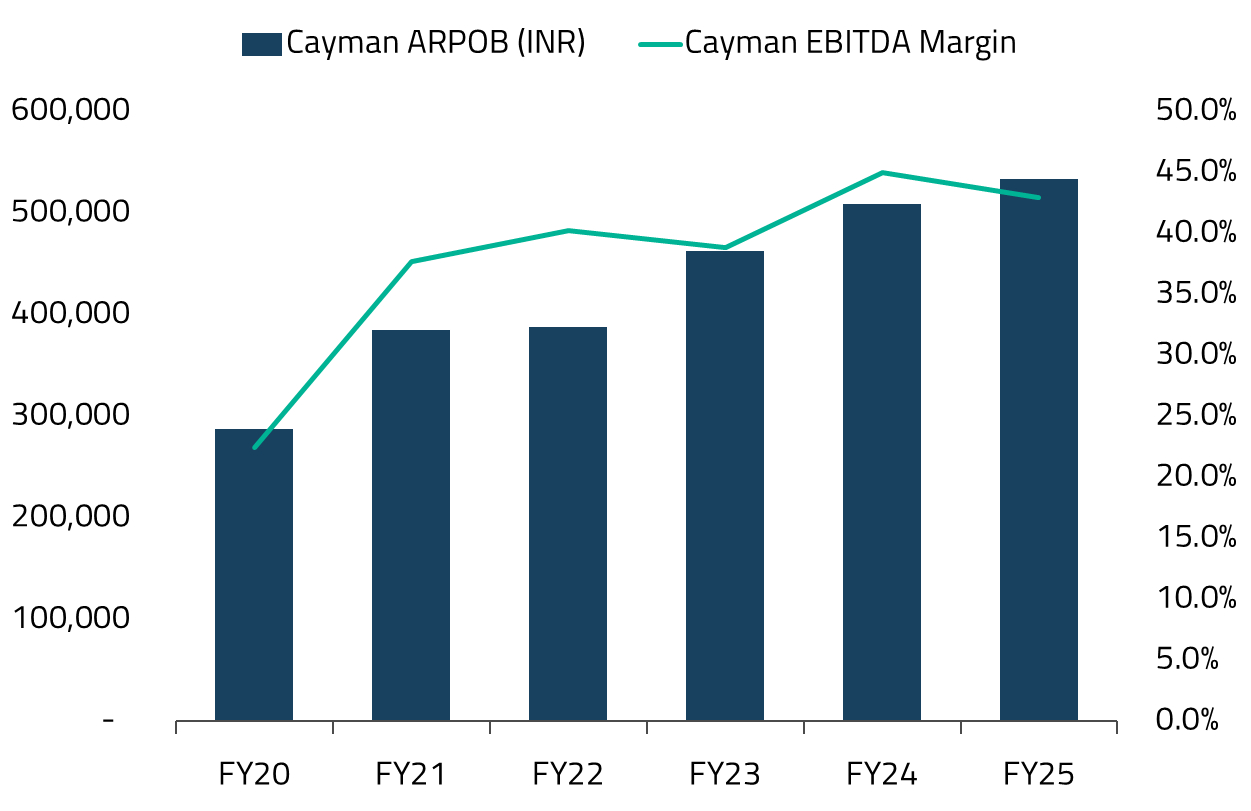

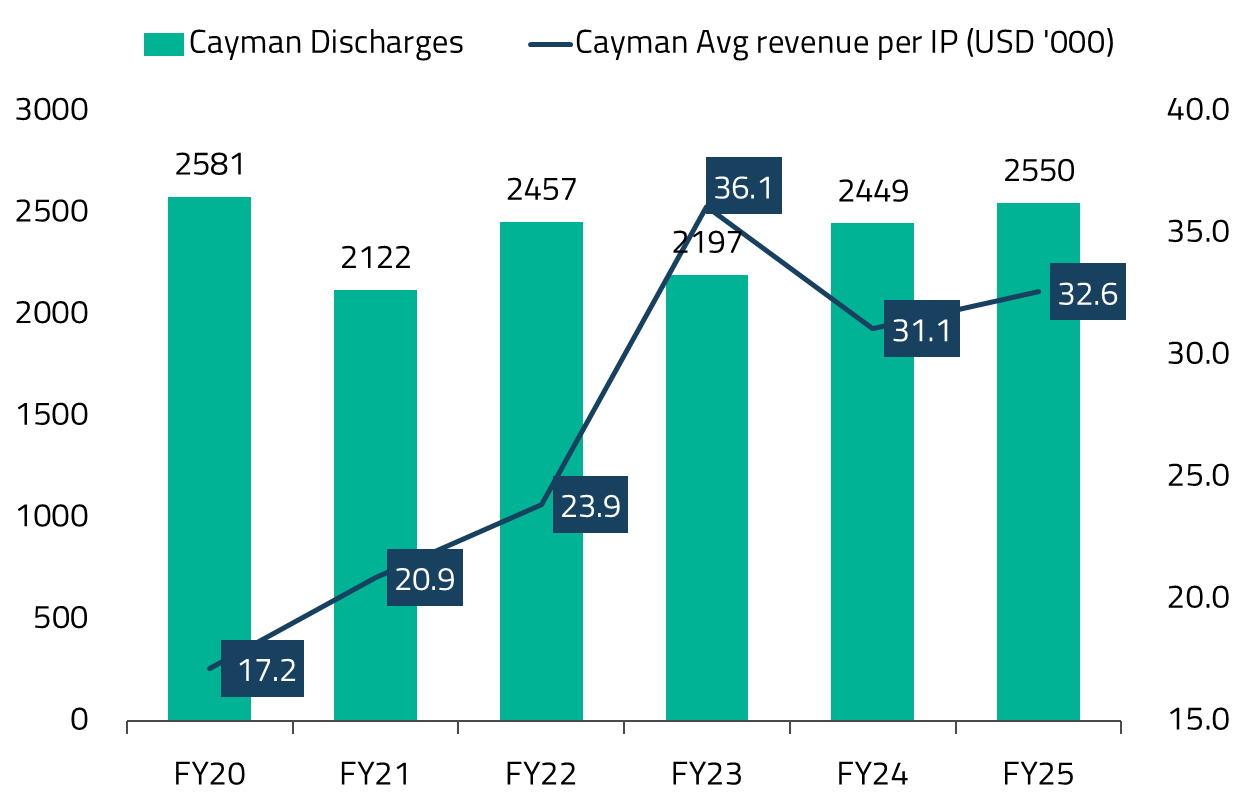

Post-COVID, Cayman emerged as a textbook case of operational transformation. NARH shifted focus decisively towards local demand, improved clinical mix, and technology-led efficiency. Instead of chasing volumes, the company concentrated on higher-acuity procedures (e.g., oncology, radiation therapy, and complex tertiary care) while simplifying every operational step, from admissions to billing. The results were striking: between FY20 and FY25, Cayman’s EBITDA margins nearly doubled from approximately 22% to 43%, and the unit’s contribution to consolidated EBITDA rose from 23% to 40%.26

Importantly, this was not a volume-driven recovery. Inpatient discharges remained broadly flat over this period, but revenue per patient compounded at roughly 14% annually since FY20, reflecting sharper case selection and better utilization of clinical assets.27

Cayman mattered for more than just profits. It demonstrated that NARH’s competitive advantage does not stem from low wages or regulatory arbitrage, but from system design – automation, standardized clinical pathways, high asset turnover, and minimal human friction in non-clinical processes. That insight now underpins NARH’s most ambitious overseas move yet: the acquisition of Practice Plus Group Hospitals (PPG) in the UK.

The UK opportunity: Practice Plus Group (PPG)

PPG gives NARH entry into one of the world’s largest and most structured healthcare markets. Operating seven hospitals and multiple surgical centers, PPG is a major partner to the UK’s National Health Service (NHS), with long-term contracts, predictable volumes, and an asset-light, day-care-heavy model. Today, the business runs at approximately 10% EBITDA margins, constrained by operational inefficiencies, limited private-pay mix, and legacy processes.28

For NARH, the opportunity is familiar. Management believes many of the same levers that worked in Cayman, such as technology-enabled workflows, faster patient throughput, tighter scheduling, and improved case mix, can be applied in the UK context. Unlike Cayman, however, the UK offers scale. Even modest improvements in private-pay share, procedure complexity, and operating efficiency could materially lift margins and returns. NARH expects PPG margins to move into the mid-teens over the next few years, with the acquisition turning EPS-accretive from FY27 and delivering 20–22% RoCE by the end of the decade.29

In that sense, Cayman was the laboratory and the UK is the real test. If NARH succeeds with PPG, it will have proven something rare in global healthcare: that a hospital model engineered in India, built on an obsession with cost, efficiency, and outcomes, can travel to developed markets and still win. That possibility, more than near-term financial accretion, defines the strategic importance of Narayana Hrudayalaya’s next chapter.

Healthcare is a sector characterized by idiosyncratic growth factors – structural demand drivers that are largely independent of broader economic cycles. In Asia, these factors are converging to create a multi-year investment opportunity that we believe is still in its early stages.

The first leg of growth stems from Asia’s manufacturing prowess in both drug and medical device production. As we discussed in our December 2024 piece, countries like India and China have built formidable manufacturing ecosystems that allow them to produce pharmaceuticals, APIs, and medical devices at globally competitive costs while meeting the stringent quality standards of regulators such as the US FDA.

The second leg of growth is the transition from manufacturing to innovation. This article has documented how China’s pharmaceutical sector has rapidly evolved from a generics-focused market to a genuine source of global drug innovation, as evidenced by the surge in out-licensing deals and the growing share of Chinese-origin molecules in global clinical trials. India’s CRDMO sector, meanwhile, is moving from basic chemistry services to sophisticated contract development and manufacturing capabilities. Both countries are now contributing to the global pharmaceutical innovation ecosystem rather than merely servicing it.

Notably, in a world of rising protectionism, healthcare stands out as one of the few sectors where cross-border access to innovation is likely to be preserved. The economic logic is simple: developed nations facing ageing populations and ballooning healthcare budgets cannot afford to shut out lower-cost innovative drugs from Asia. AstraZeneca’s recent US$15 billion China investment through 2030 underscores this point, as does the broader surge in China-to-West licensing deals.30

The third leg of growth is the potential for cost-effective Asian healthcare delivery models to be replicated globally. As the Narayana Hrudayalaya case study illustrates, India’s hospital operators have demonstrated that it is possible to deliver high-quality clinical outcomes at a fraction of the cost seen in developed markets and, critically, that this model can be exported. NARH’s experience in Cayman proved the concept; its acquisition of PPG in the UK now tests whether the model can scale in a major developed healthcare system. If successful, it would establish a powerful precedent for Indian healthcare delivery, expanding well beyond domestic borders.

Taken together, these three growth vectors (manufacturing scale, innovation capability, and cost-effective delivery models) position Asia’s healthcare sector as one of the most compelling structural investment opportunities in emerging markets. We expect this theme to continue to evolve and expand, and will continue to identify and invest in companies that are at the forefront of this transformation.

For sophisticated investors only. For informational purposes only. The information presented in the material is not and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP (“Shikhara”) is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission. This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such, information is accurate, complete and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this material are prepared and maintained by Shikhara and has not been reviewed by the Securities and Exchange Commission of the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.