In the bustling port of Busan in South Korea, giant cranes unload transformers destined for the US. Thousands of miles away, in India, engineers are working to modernize power grids and integrate renewable energy into a growing industrial network. Meanwhile, in Germany, battery cells from a Chinese factory power the latest generation of electric vehicles (EVs) for European roads.

These activities are not isolated, but part of a larger narrative of a global industrial revival, driven by the need for security and sustainable growth. In this paper, we explore the key drivers behind this industrial resurgence, Asia’s critical role in the evolving global supply chain, and the exciting investment opportunities emerging in this transformative era.

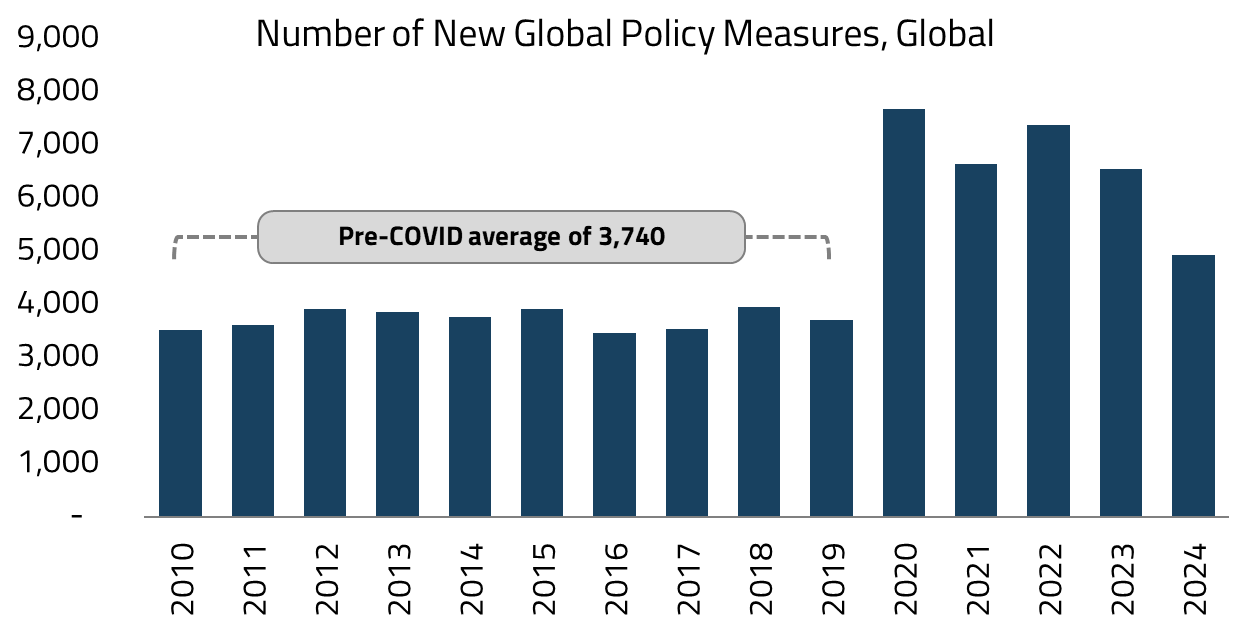

Governments around the world are increasingly using industrial policies in their administrative agendas. Industrial policy involves government initiatives to shape the economy by targeting specific industries, corporations, or economic activities. Key measures include subsidies, trade barriers, exclusive lists, foreign direct investments, and localization and procurement policies.

Policymakers are increasingly relying on direct intervention to address broader market failures. For instance, in the US, the Biden administration introduced unprecedented subsidy-based programs, including the CHIPS Act, the Inflation Reduction Act, and the Infrastructure Investment and Jobs Act. The current Trump administration, on the other hand, uses sectoral tariffs on key industries to address the cost and technology gap with other countries.

Beyond the US, in India, the government introduced the Production Linked Incentive (PLI) scheme, which is a form of performance-linked incentive designed to provide companies with financial benefits based on incremental sales from products manufactured in domestic units. The European Union has its own Green Deal Industrial Plan and Critical Raw Materials Act, while China has continued its Made in China 2025 initiative over the past decade, focusing on high-tech industries. More recently, Germany’s landmark EUR 631 billion “Made For Germany” initiative, aimed at boosting domestic industrial capacity and reducing reliance on foreign supply chains, marks one of the most ambitious examples of contemporary industrial policy in Europe.

The emergence of a multipolar world is driving the increasing prominence of industrial policies. Each nation is striving to secure resources and economic advantages for itself. In this context, there are four drivers behind the rising importance of industrial policy:

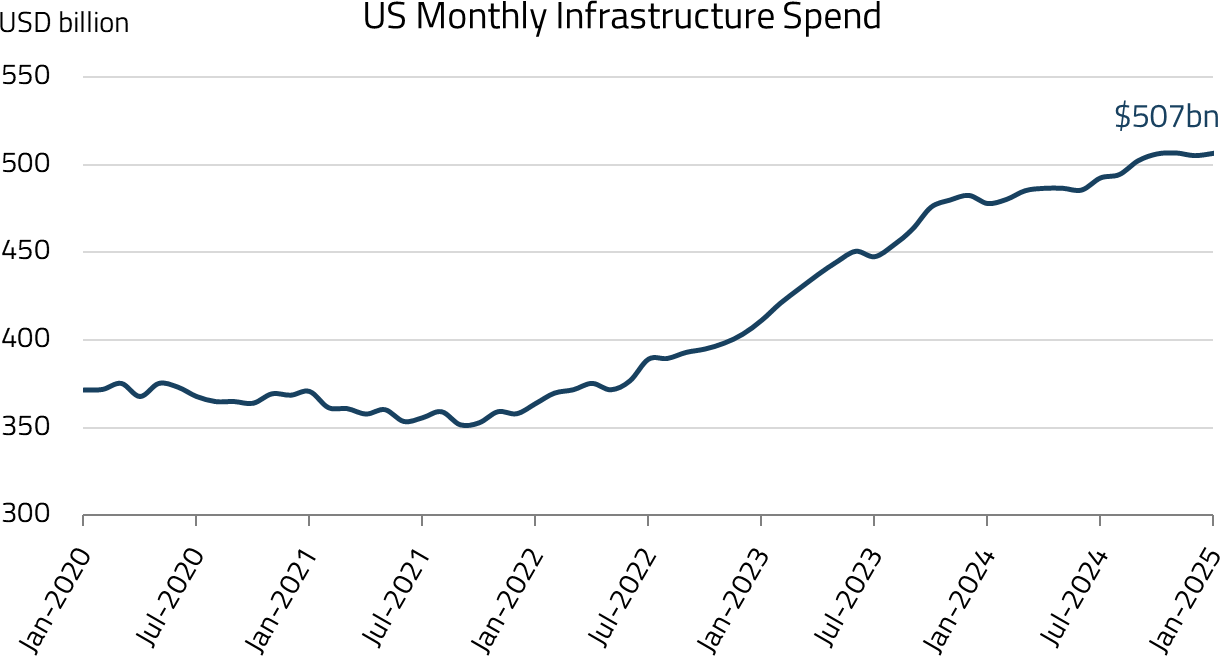

1. Underdevelopment of Infrastructure in the US and Europe

Post-financial crisis, much of the developed world (and India as well) went through a necessary deleveraging following the excesses of the early 2000s to 2007. This was followed by the rise of capital-light tech platforms – high ROE businesses that captured market attention but required minimal physical investment. Then came COVID-19. The cumulative effect was 17 years of limited capital investment. And the result is stark: aging infrastructure ill-equipped for today’s demands and utterly unprepared for a world where corporates increasingly look to form 20-30% local capacity to reduce dependence on geopolitically unaligned countries.

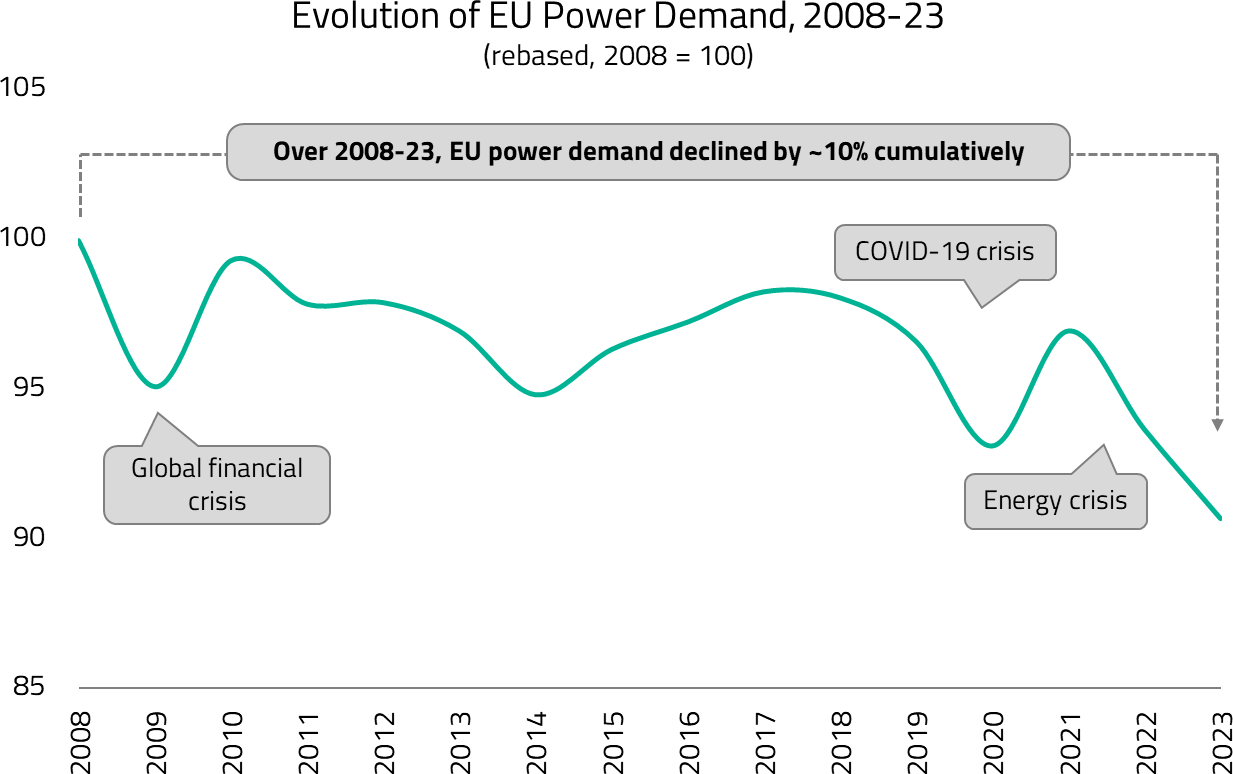

This is particularly obvious in the power infrastructure. We saw this recently with the Iberian Peninsula blackout, which left mainland Portugal and parts of Spain without electricity for almost a day. Power demand in Europe peaked in 2008 but then faced a prolonged period of weak consumption, driven by the GFC in 2009, the COVID-19 pandemic in 2020, and the Energy Crisis in 2022. Currently, electricity demand is ~10% below 2008 levels.1 However, the electrification trend and the build-out of AI data centers are raising the structural long-term power demand growth. This challenge is not limited to Europe but extends to other developed markets, including the US and Australia. As a result, governments are now forced to address these deficiencies through aggressive industrial policies.

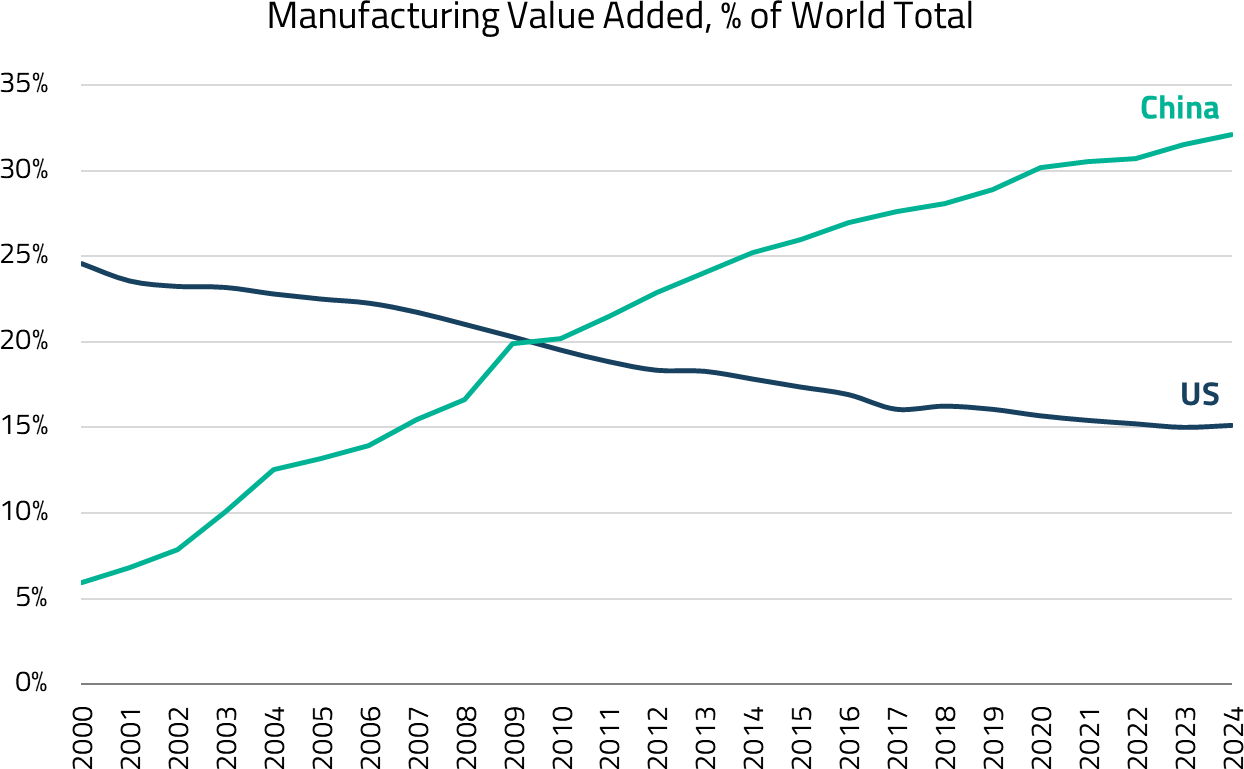

China was once primarily associated with low-value-added products that posed little threat to global brands in high-end markets such as tech/electronics in the US and auto/luxury goods in Europe. However, during its multi-year COVID-19 lockdown and amid rising US-China tensions, many foreign businesses were not able to visit China as regularly as they did in the 2010s. Simultaneously, Chinese companies scaled back foreign expansion as senior executives faced travel restrictions.

When China’s borders reopened in 2023, many countries and corporations discovered that Chinese products had undergone significant advancements and were starting to pose a real threat to global supply chains. The combination of economies of scale, agility, technological advances, and competitive pricing has made Chinese products highly sought after in global markets. “Mind-blown” was the word used by many foreign visitors who attended the China auto shows in 2024 and 2025, commenting on the level of innovation on display.

The rapid export growth of advanced Chinese products is starting to threaten the crucial pie of developed markets and, in a way, affecting local employment and tax revenues. In response, many countries have introduced protectionist measures and industrial policies aimed at slowing China’s threat, leveling the cost and technology gap, and buying time to nurture their domestic ecosystems that have some catching up to do.

In a globalized market with free capital flow, companies have traditionally focused on maximizing profits through specialization. Production and operations were naturally outsourced to regions offering competitive advantages – from low-cost labor and efficient infrastructure to established ecosystems and sometimes looser regulatory standards. However, the pandemic and rising geopolitical tensions have forced corporates and governments to reassess this approach.

Diversifying supply chains at higher costs has become a priority to ensure resilience. Many companies suffered due to logistics issues during the pandemic, volatile energy and raw material prices during geopolitical disputes, or just a lack of access to key critical components when they were needed. As a result, supply chain security has become just as important as profit maximization.

This shift has created new investment opportunities globally. Many countries are now competing to attract multinational corporations (MNCs) by launching industrial policies that leverage their core strengths. For example, countries like the US leverages its strong local consumer market; Mexico and Brazil capitalize on their geographic advantages; Indonesia positions itself as a resource hub; Malaysia offers cheap power costs; and India promotes friendly fiscal policies. The competition among nations to attract MNCs has intensified, reshaping the global industrial landscape.

The US has clearly shown an interest in industrializing the country with a tilt towards higher-valued production and security-sensitive industries, such as telecommunications, autos, shipbuilding, semiconductors, and pharmaceuticals. To achieve this, the US has to provide sufficient protectionist policies, including but not limited to tariffs, subsidies, policy changes, and country exclusions. These measures aim to bridge the cost and technology gaps not only with China but also with other importing nations.

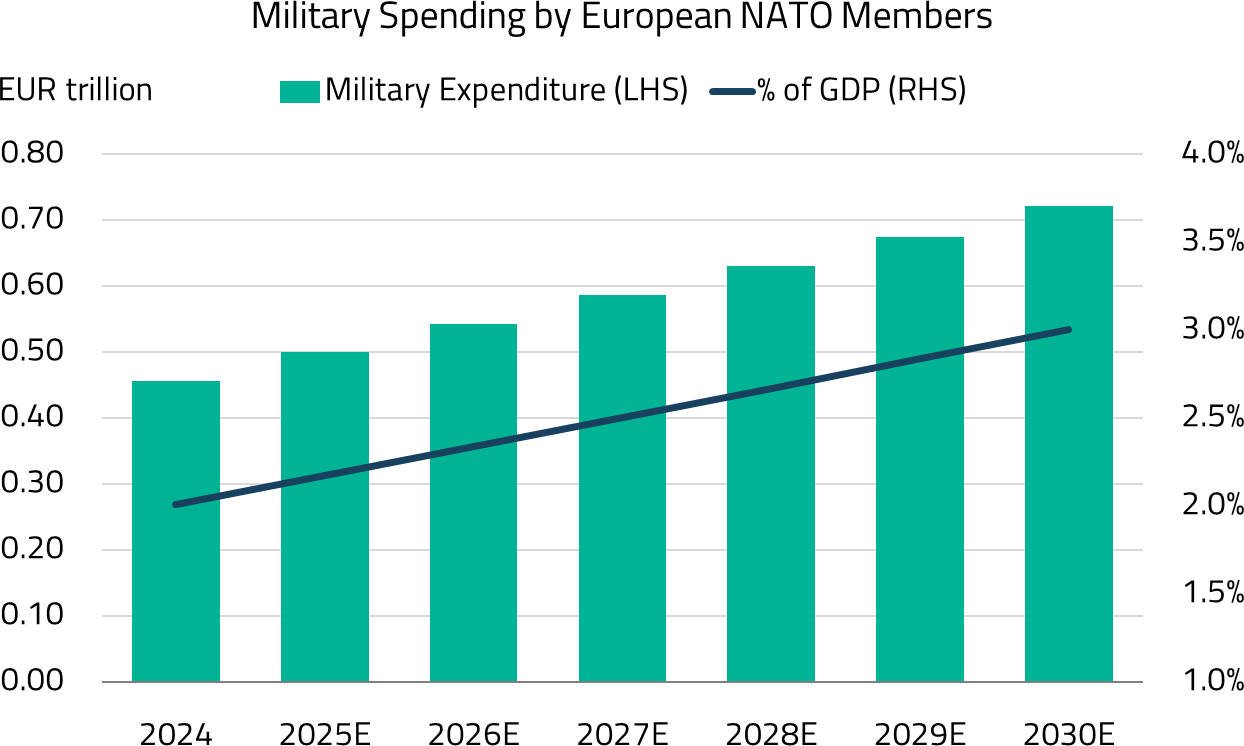

Meanwhile, the US is also pulling back from global participation in international organizations and is less actively supporting its allies. This shift has left allied nations needing to fend more for themselves and reduce dependence on US spending. Defense is a prime example of where industrial policies are being implemented to rebuild regional and local capabilities.

An example of this trend is the EUR 631 billion “Made For Germany” initiative mentioned earlier. This program joins a EUR 500 billion government infrastructure fund and EUR 400 billion in new government debt for defense, all coordinated with the country’s leading banks and savings institutions.

These investments are not just about stimulating domestic growth. They represent an explicit strategy to reduce Germany’s reliance on both Chinese manufacturing and US security guarantees. By channeling capital into expanding local capacity and technological independence, Germany is responding directly to geopolitical risks, such as the weaponization of supply chains and shifting global alliances. The country’s willingness to go at it alone, bypassing slow EU-level coordination, signals a new era in which major economies seek resilience and autonomy.

The Trump administration has announced a strong appetite to re-industrialize the US, focusing on key verticals such as automobiles, pharmaceuticals, defense, shipbuilding, and semiconductors. From the US perspective, rebuilding domestic manufacturing capacity is essential not only for economic resilience but also for strategic autonomy. Ensuring control over key assets means that if a geopolitical conflict were to eventuate in the next 10-15 years, the US will have the necessary infrastructure in place to maintain its strategic interests without being entirely dependent on China.

The direction toward re-industrialization is clear. But considerable ambiguity regarding policy details and implementation remains. For example, the varying levels of tariffs imposed by the US across different countries make it difficult for companies to effectively plan their production facilities and supply chains.

For industrial companies, as profit margins are not very high, a 5-10% difference in tariff rate matters a lot in the project return analysis. Moreover, many of the industrial policies are subject to change between different administrations. Corporations don’t want to be left behind with investments tied to stale policies. For instance, changes to the Inflation Reduction Act or CHIPS Act could lower the project returns significantly. In this environment, both companies and nations are actively adjusting their strategies to navigate the uncertainty.

In normal circumstances, such fluctuations in policy are manageable, as they occur in every country. However, the challenge in recent years is the frequency and scale of industrial policy changes, which have become more drastic and unpredictable. This volatility has made it harder for companies to commit to long-term investments with confidence.

To address these challenges, the US is exploring several measures, including:

While these steps signal a clear intent to strengthen the US industrial base, policy stability and clarity will be crucial for attracting corporate investment and achieving sustainable success in re-industrialization.

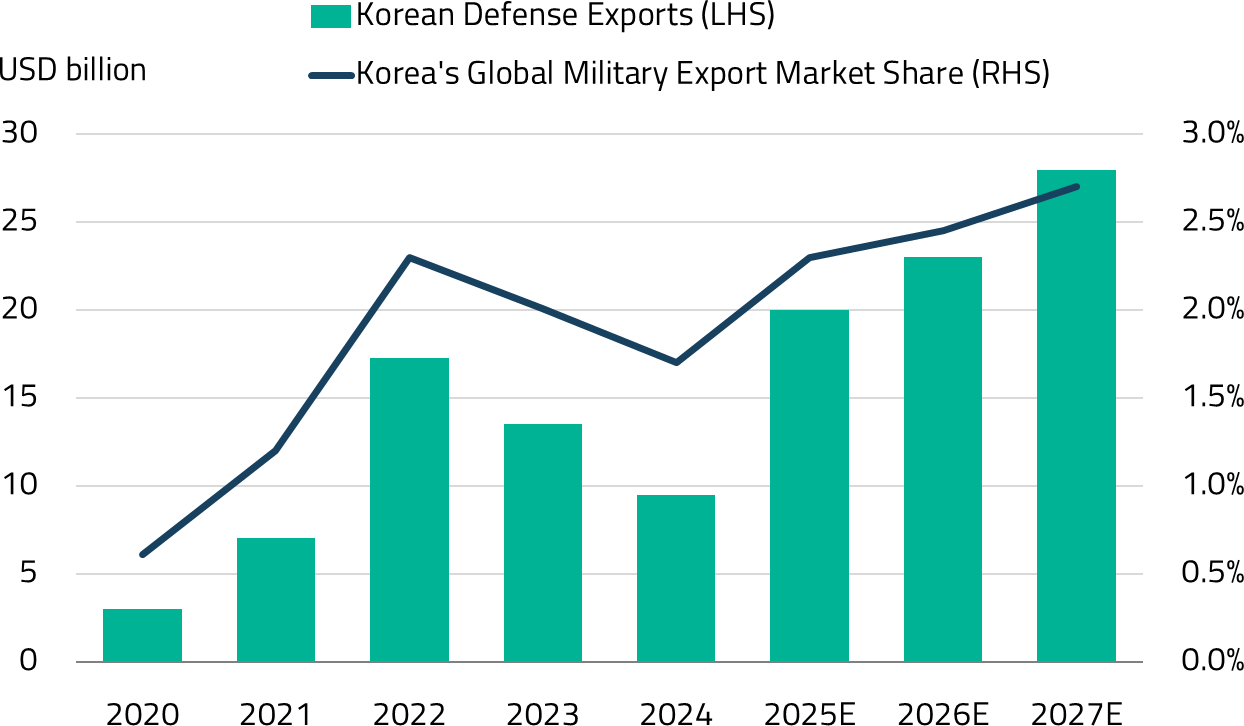

The reindustrialization efforts in the US and Europe cannot succeed in isolation. These developed markets require strong partnerships to rebuild their industrial ecosystems and meet strategic goals. In this context, we think Asian countries, particularly South Korea and Japan, are positioned to play a crucial role in the global supply chain.

South Korean and Japanese industrial companies stand out as ideal partners due to several competitive advantages:

Beyond individual partnerships, Asia’s broader role in the global supply chain reflects its position as a critical region for reindustrialization. With a mix of developed economies like South Korea and Japan, emerging manufacturing hubs such as India and ASEAN, and the manufacturing giant China, Asia will remain a backbone of global production networks.

Korean and Japanese companies: Rightful partners in US and European reindustrialization

We believe South Korean and Japanese companies will be essential partners in the reindustrialization efforts of the US and Europe. These firms bring a combination of engineering excellence, global competitiveness, and specialized capabilities that align well with the needs of advanced industrial economies.

In grid infrastructure, South Korean firm HD Hyundai Electric has significantly expanded its transformer exports to the US, with a strong backlog to show for it. The company established a transformer factory in the US back in 2011, giving it over a decade of operational track record. Its product knowledge, quality, and reliability are important to US utility companies choosing suppliers, making HD Hyundai Electric a preferred supplier for grid infrastructure projects. Beyond the US, the company has also secured a solid footprint in the Middle East and Europe, supported by new order wins in these regions.

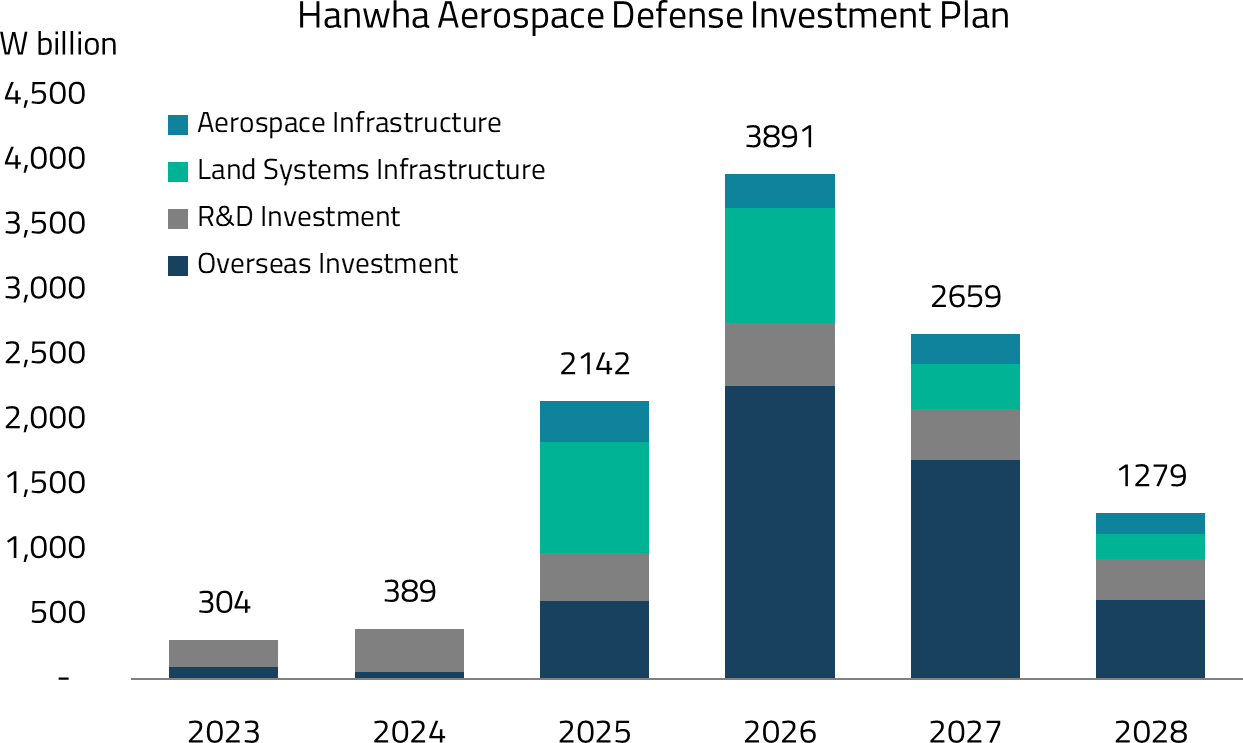

In defense, Hanwha Aerospace in South Korea is gaining momentum globally, driven by heightened geopolitical tensions. The company recently hosted an ‘Industry Day’ event in Berlin, signaling plans to partner with Germany to address the land system arms supply shortage in Europe. In the Middle East, Hanwha Aerospace has prioritized local partnerships in Saudi Arabia for land systems, which has been set as the top KPI for the management. The company is also well-positioned for potential order wins in the US and Canada, leveraging its growing global reputation. Additionally, Hanwha Aerospace owns Hanwha Ocean, which is strategically placed to secure shipbuilding or navy-related new build and maintenance, repair, and overhaul (MRO) projects.

In Japan, heavy industrial companies are well positioned to benefit from the global tightness in shipbuilding, defense, and gas turbine manufacturing capabilities. We highlight Mitsubishi Heavy Industries (MHI), which is a global leader in gas turbine combined-cycle systems – a critical technology for gas-fired power plants. The company is benefiting from the global upcycle in gas-fired power plant construction, driven by surging electricity demand due to expanding AI and data center investments. Beyond energy infrastructure, MHI has significant exposure to defense and nuclear energy sectors, making it a key partner for countries prioritizing strategic industrial and energy projects.

India’s energy transition and power infrastructure upcycle

India is rapidly advancing its energy transition, with ambitious renewable energy targets of 500 GW of non-fossil fuel capacity by 2030.2 The country is also overhauling its power infrastructure to support industrial growth and supply chain localization. As India positions itself as a “China+1” destination in the multipolar industrial order, the power sector is emerging as a critical enabler. Years of underinvestment are now being reversed through a surge in capex across generation, transmission, and distribution (T&D).

The T&D segment, which has long been a bottleneck, is finally seeing renewed momentum. The focus is driven by the need to integrate intermittent renewable energy and support rising base-load demand from data centers, manufacturing hubs, and urban electrification. High Voltage Direct Current (HVDC) technologies are gaining prominence, enabling efficient long-distance power transmission and reducing grid losses. This is a necessary step as generation assets diversify geographically.

With only a handful of global players qualified for HVDC projects, companies like Hitachi Energy are poised to benefit meaningfully. Wind energy players like Suzlon are also seeing a renaissance, benefiting from a policy and market pivot toward renewables with round-the-clock power capability.

Meanwhile, engineering and infrastructure firms such as CG Power, L&T, and Kalpataru Projects are well-positioned to capitalize on accelerating investments in T&D and grid modernization. Power generation companies, too, stand to gain from increased capacity additions and policy incentives that prioritize green energy and grid stability.

Chinese companies: Striking a balance between collaboration and competition

There is no doubt that Chinese companies are advancing rapidly in manufacturing innovation, establishing a growing presence in high-value-added verticals, including automobiles, batteries, and power infrastructure. Firms that combine globally leading technology with sustained investment in R&D will remain highly competitive on the global stage. To address customer demands for supply chain diversification, many Chinese firms have begun localizing their supply chains outside of China. This enables them to operate with less geopolitical exposure while maintaining strong international partnerships.

One standout example is Contemporary Amperex Technology Co., Limited (CATL), a global leader in battery manufacturing. The company has strategically invested in two major battery production facilities in Hungary and Germany, placing it close to its European automotive original equipment manufacturer (OEM) customers. Not only does this localization strategy strengthen its customer relationship, but CATL also distinguishes itself through unparalleled R&D spending, which exceeds that of all other major global battery players combined. CATL spent USD 9 billion on R&D over 2020-24, which is greater than the next 5 Chinese battery makers combined.3 This relentless focus on innovation makes CATL a critical enabler of the global energy transition.

Another notable example is Zhejiang Shuanghuan Driveline, a leading producer of high-precision gears that are widely used in all types of vehicles. As electric vehicle (EV) adoption accelerates, the company has seen its market share and content per vehicle increases substantially. In 2023, Shuanghuan Driveline announced plans to establish a new manufacturing plant in Hungary to serve Europe’s growing new energy vehicle market. This move underscores the company’s commitment to aligning with global trends, leveraging its technological know-how to tap into new opportunities in international markets. The company is also positioning itself as a key supplier of humanoid robotic gears.

There’s a lot more noise and complexity in understanding the global industrialization theme, making it difficult to navigate. Geopolitical uncertainty is rising, project profitability remains volatile due to shifting policy assumptions, and the current high-interest rate environment is causing corporations to approach capital expenditures with increasing caution. Companies are also contending with lingering challenges, including the energy crisis, the aftermath of COVID-19 supply chain disruptions, and the broader geopolitical environment.

However, it’s worth highlighting that these investments are not disappearing – they are just delayed. The demand for additional capacity remains strong, driven by the need to support a multipolar world, albeit at a higher cost to consumers.

Our investment philosophy remains pragmatic. While it’s easy to get caught up in doomsday scenarios, history suggests this rarely eventuates. Instead, we’re positioning for the more likely scenario: a multi-year investment cycle that addresses years of underinvestment in critical infrastructure. We anticipate a reprioritization of domestic infrastructure across many Western economies, particularly the US. This includes investments in national infrastructure like roads, bridges, power and grid facilities, and strategic factories such as those for semiconductor manufacturing.

Additionally, we believe the green and renewable transition remains a core theme and continues to be top of mind for policymakers worldwide. Despite US rhetoric and pushback against the climate agenda, governments globally continue to embed sustainability-focused initiatives, further driving the need for large-scale industrial and infrastructure investments.

Asia is at the heart of this global industrial upcycle, bridging the gap between the world’s reindustrialization agenda and the rising demand for advanced technologies and resilient supply chains. With South Korea and Japan excelling in defense, shipbuilding, and energy systems, and India positioning itself as the next manufacturing hub, the region is well-equipped to drive growth across critical sectors. Simultaneously, China’s sustained investment in R&D and strategic localization efforts highlight its ongoing importance in global supply chains.

As governments and corporations intensify their focus on rebuilding and modernizing their industrial bases, the need for partnerships, innovation, and strategic investments has never been greater. For investors, this presents a rare opportunity to capitalize on Asia’s growing prominence in a multipolar world, where industrial policies, energy transitions, and supply chain resilience are reshaping the global economic order.

For sophisticated investors only. For informational purposes only. The information presented in the material is not and may not be relied on in any manner as legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This material doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP (“Shikhara”) is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission. This material does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this material are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Certain information contained in this material is compiled from third-party sources. The information and any opinions contained in this document have been obtained from sources that Shikhara considers reliable, but Shikhara does not represent that such information and opinions are accurate or complete, and thus should not be relied upon as such. Furthermore, all opinions are current only as of the date of distribution and are subject to change without notice. Shikhara does not have any obligation to provide revised opinions in the event of changed circumstances. Whereas Shikhara has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this material. Neither Shikhara nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this material are prepared and maintained by Shikhara and has not been reviewed by the Securities and Exchange Commission of the United States.

This website is published exclusively for the purpose of providing general information about the management services carried out by Shikhara Investment Management LP, Shikhara Capital (Hong Kong) Private Limited and its affiliates (collectively “Shikhara Investment Management” or “Shikhara”). The information presented on the website is not, and may not be relied on in any manner as legal, tax, investment, accounting, or other advice or as an offer to sell or a solicitation of an offer to buy an interest in any investment product or any other entity sponsored or managed by Shikhara Investment Management. This website doesn’t constitute and should not be considered as any form of financial opinion or recommendation.

Shikhara Investment Management LP is currently an Exempt Reporting Adviser that is exempt from registration as an investment adviser with the U.S. Securities and Exchange Commission and Shikhara Capital (Hong Kong) Private Limited has been approved by the Hong Kong Securities and Futures Commission. This website does not constitute an offer to sell or the solicitation of an offer to buy in any state of the United States or other U.S. or non-U.S. jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such state or jurisdiction.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the investment product will generate a return and there may be circumstances where no return is generated. Investors could lose all or a substantial portion of any investment made. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the investment product and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Shikhara’s investment products are suitable only for sophisticated investors and require the financial ability and willingness to accept the high risks and lack of liquidity inherent in Shikhara’s investment products. Prospective investors must be prepared to bear such risks for an indefinite period of time. No assurance can be given that the investment objectives of any given investment product will be achieved or that investors will receive a return of their investment.

Certain of the information contained in this website are statements of future expectations and other forward-looking statements. Views, opinions, and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance, or events may differ materially from those in such statements.

Certain information contained in this website is compiled from third-party sources. Whereas Shikhara Investment Management has, to the best of its endeavor, ensured that such information is accurate, complete, and up-to-date, and has taken care in accurately reproducing the information, Shikhara Investment Management takes no responsibility for the accidental publication of incorrect information, nor for investment decisions taken based on this website. Neither Shikhara Investment Management nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein, and nothing contained herein should be relied upon as a promise or representation as to past or future performance of any investment product or any other entity.

The contents of this website are prepared and maintained by Shikhara Investment Management and has not been reviewed by the Securities and Exchange Commission of the United States or the Securities and Futures Commission of Hong Kong.

The Shikhara logo and name are trademarks of Shikhara Investment Management LP, registered in Hong Kong, the People’s Republic of China (PRC), Australia, the United Kingdom, the European Union, and the United States.